Introduction

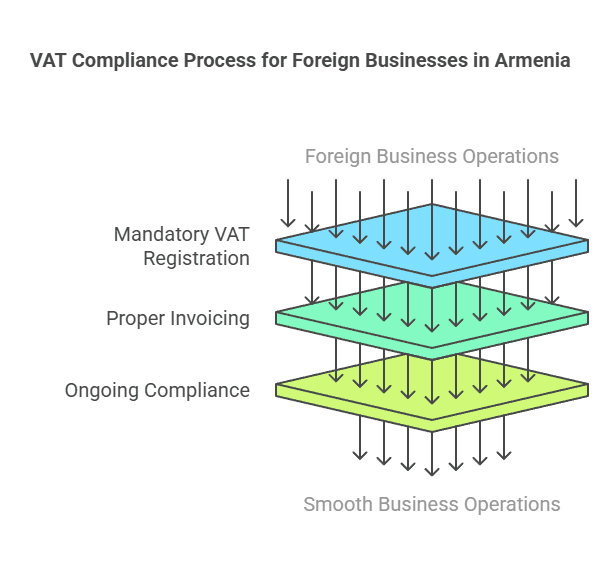

Expanding a business into Armenia requires a clear understanding of local tax obligations, especially VAT registration for foreign businesses. Armenia imposes a 20% Value Added Tax (VAT) on most goods and services, and foreign companies (non-residents) operating in Armenia may need to register for VAT under certain conditions. This comprehensive guide explains when VAT registration is required for foreign (non-resident) entities, who qualifies as a foreign taxable person, current VAT registration thresholds and exemptions, the step-by-step registration process, and ongoing Armenia VAT compliance duties. We cover all types of foreign enterprises – from digital service providers and e-commerce platforms to import/export traders, companies with a physical presence, and cross-border service firms.

Overview: VAT and Foreign Businesses in Armenia

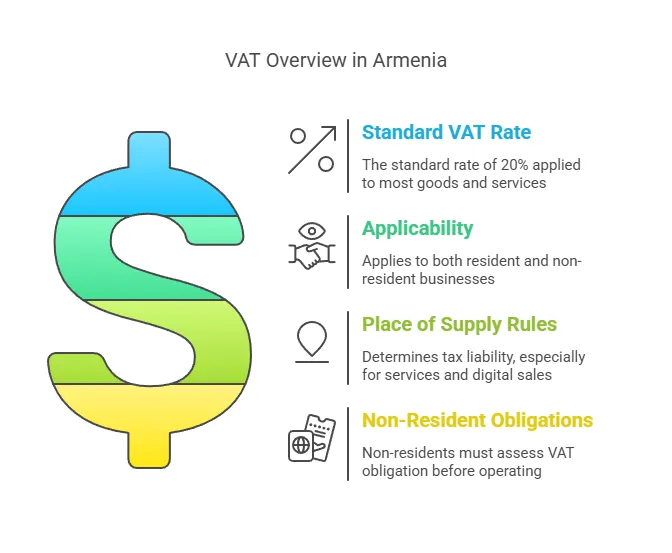

VAT in Armenia is a broad-based consumption tax at a standard rate of 20%, similar in principle to European VAT systems. It applies to the sale of goods and services in Armenia, and also to the importation of goods. Foreign companies (“non-resident” businesses) doing business in Armenia are generally subject to the same VAT rules as local companies, but with specific provisions for non-residents. Key points to understand include:

- Foreign taxable entities: In Armenia, any business entity (company or individual entrepreneur) making taxable supplies in the country is potentially required to register for VAT. A foreign company with no permanent establishment in Armenia (a “non-established” business) may still need to register for VAT if it conducts taxable transactions in Armenia that are not otherwise accounted for by a local VAT-registered customer. Foreign companies that set up a branch or other permanent establishment (PE) in Armenia are treated as local taxpayers for VAT purposes and must register accordingly.

- Place of supply rules: VAT is due in Armenia if the place of supply of goods or services is considered to be Armenia. For goods, this is generally when goods are in Armenia or imported into Armenia. For services, Armenia’s tax law deems certain services as supplied where the service is used or performed (with special rules for electronic services, discussed below). If a foreign business provides services within Armenia’s territory, or to customers located in Armenia, those services may be taxable in Armenia.

- Reverse charge mechanism: Armenia utilizes a reverse-charge system for certain cross-border B2B transactions. If a foreign supplier (without an Armenian VAT registration) provides a service or good to an Armenian business that is already VAT-registered in Armenia, the local business can self-account for the VAT (reverse charge). In such cases, the foreign supplier does not need to register for VAT because the Armenian buyer will calculate and pay the VAT. This mechanism ensures VAT is still collected, but shifts the compliance burden to the local VAT-registered customer. However, if the Armenian customer is not a VAT-registered taxpayer, the reverse charge does not apply – meaning the foreign supplier itself must register and charge Armenian VAT.

- Non-resident VAT portal: As part of modernizing tax administration, Armenia introduced an online e-VAT system that allows non-resident companies (particularly digital service providers) to register and file VAT returns easily without a local presence. This is especially relevant from 2022 onward as Armenia expanded VAT rules to cover foreign digital services.

In summary, foreign businesses selling to Armenian customers should assess whether they need an Armenian VAT number. The obligation depends on the nature of the supplies (goods or services), the type of customer (business or consumer, VAT-registered or not), and the scale of activities. Next, we define who is considered a foreign taxable person and when exactly VAT registration is mandatory for such entities.

Who Is Considered a Foreign Taxable Entity?

For VAT purposes, a foreign taxable entity in Armenia is generally a business that is not established in Armenia but is engaging in economic activities within Armenia’s jurisdiction. This includes:

- Non-resident companies with no fixed establishment in Armenia – for example, an overseas company selling digital services or goods to customers in Armenia without any branch, office, or other physical presence in Armenia. These are often called “non-established” or “non-resident” taxable persons.

- Foreign companies operating through a branch or representative office – if a foreign company registers a branch, representative office, or any fixed place of business in Armenia that carries out business activities, that branch is effectively a local establishment for tax purposes. It will be treated as a permanent establishment (PE). A PE in Armenia (such as a branch) must register as a taxpayer and comply with VAT rules like a resident business.

- Foreign individual entrepreneurs or professionals providing services or doing business in Armenia (without residing in Armenia). For instance, a consultant from abroad who comes to Armenia to perform a project might be considered a foreign taxable person if they conduct taxable transactions on Armenian soil.

It’s important to note that merely having a representative office that performs only auxiliary or preparatory activities (e.g. an office only doing market research and not actual sales) might not constitute a taxable presence. However, as soon as a foreign entity carries out commercial activities in Armenia (selling goods, rendering services, etc.), it potentially enters the Armenian VAT system.

Permanent establishment vs non-established: If your foreign business has a fixed place of business in Armenia (such as an office, workshop, store, factory, construction site over a certain duration, etc.), or people acting on your behalf in Armenia who can conclude sales contracts, you likely have a permanent establishment under Armenian tax law. That means the foreign business is effectively “established” in Armenia for tax purposes and must register as a local taxpayer (and thus for VAT). On the other hand, if you have no fixed base in Armenia – e.g., you sell remotely via internet or occasional visits – you are a non-established (non-resident) business. Non-established businesses can still have VAT obligations in Armenia, but they do not register as a local company; instead, they would register directly as a non-resident VAT payer if required.

Foreign versus local business status: One practical distinction is that foreign businesses cannot use Armenia’s small business regimes to avoid VAT. Armenia has a special “turnover tax” system for small enterprises under a revenue threshold (instead of VAT), but non-resident legal entities and their PEs are explicitly excluded from that regime. This means foreign businesses (and any branches they set up) are always subject to the normal VAT system from day one if they engage in taxable activities – they cannot claim the small business exemption that local entrepreneurs under the threshold might use. In other words, if a foreign entity does business in Armenia, it is considered a VAT payer by default when making taxable supplies (unless the reverse charge applies as mentioned). We will cover the registration thresholds next, but keep in mind foreign companies do not get the same threshold benefits as local firms in most cases.

Now that we have defined foreign taxable entities, let’s examine when a foreign business is required to register for VAT in Armenia.

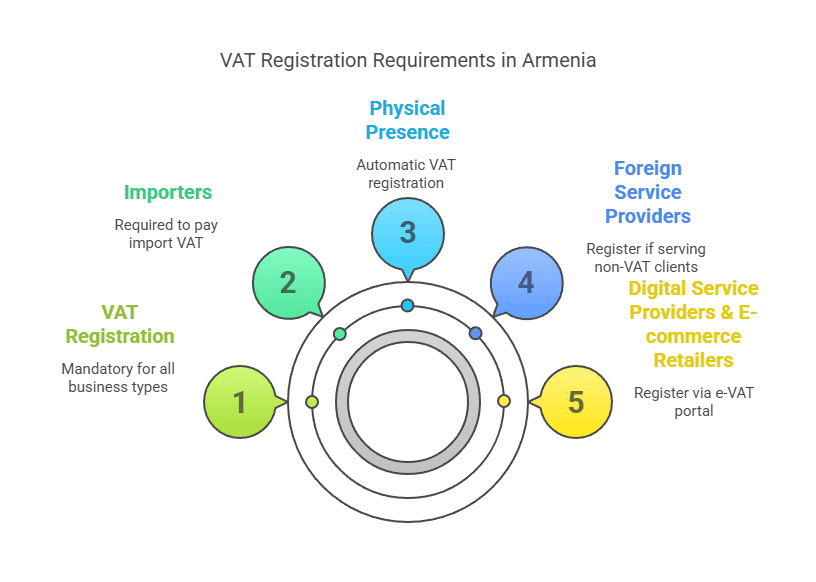

When Must a Foreign Business Register for VAT in Armenia?

Determining when VAT registration is required is crucial. Foreign businesses should register for Armenian VAT before making taxable supplies that obligate registration. The requirements depend on the nature of the transactions and the customers:

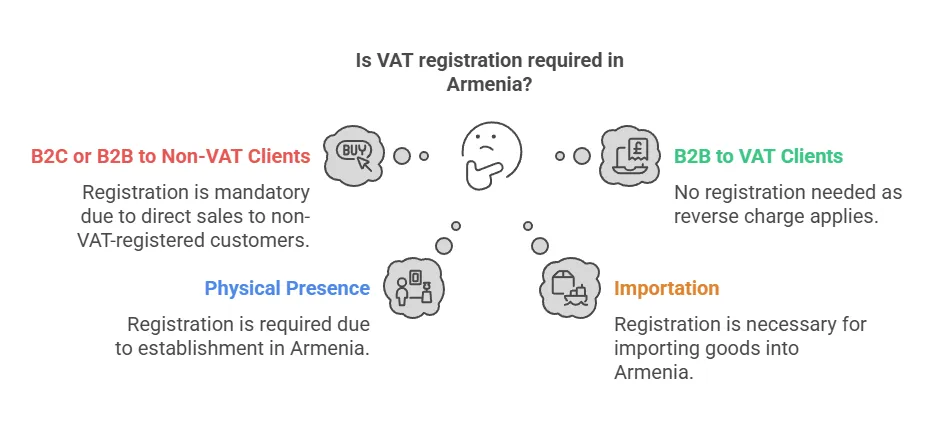

1. Selling to non-VAT-registered customers (B2C or small B2B): If a foreign business with no Armenian VAT registration makes taxable sales to Armenian customers who are not VAT payers, the foreign business must register and charge Armenian VAT on those sales. “Not VAT payers” includes private individuals (B2C sales) and any Armenian businesses or organizations that are not themselves registered for VAT (for example, small enterprises under the threshold or entities on the turnover tax system, as well as perhaps NGOs or government bodies that are outside the VAT system). In these cases, there is no minimum sales threshold – registration is required from the first taxable sale. Armenia’s tax law places the responsibility on the foreign supplier to account for VAT when the local customer cannot self-account.

- Digital services B2C: A prime example is foreign digital service providers (like providers of streaming services, software, online advertising, etc.) selling to Armenian consumers. As of 2025, Armenia’s law explicitly requires non-resident digital service suppliers to register and charge 20% VAT on B2C services delivered to Armenian individuals (with no threshold). We discuss digital services in detail below, but the rule is clear: non-resident B2C services trigger immediate VAT obligations.

- Goods sold to Armenian consumers: If a foreign e-commerce company sells goods directly to Armenian private customers and somehow arranges delivery inside Armenia, the foreign seller is responsible for Armenian VAT. In practice, VAT on goods is often collected at import (customs), but if the foreign seller acts as the importer-of-record or sells goods already in Armenia, a VAT registration would be needed to charge VAT on the sale. There isn’t a specific distance selling threshold in Armenia as in some jurisdictions; any regular supply of goods in Armenia by a foreign entity to a non-VAT customer could create an obligation to register.

- Services to non-registered businesses: Suppose a foreign consulting firm provides services to a small Armenian company that is not VAT-registered (e.g. a startup that hasn’t reached the threshold or opted for VAT). Because the Armenian client is not in the VAT system, the foreign firm cannot rely on reverse charge – the foreign firm must register and charge VAT on its fees for services performed in Armenia or deemed supplied in Armenia.

2. Selling exclusively to VAT-registered businesses (B2B): If a foreign company’s only activity in Armenia is selling to Armenian businesses that are VAT-registered taxpayers (under the standard VAT system), then the foreign company is not obliged to register for VAT. This is thanks to the reverse charge mechanism. In B2B transactions where the Armenian customer is a VAT payer, the law allows the local customer to self-assess VAT. The Armenian buyer will issue a self-invoice for the purchase, calculate the 20% VAT on the value, pay that VAT to the tax authority (and simultaneously deduct it as input VAT if it relates to their taxable business activities). In this scenario, the foreign supplier does not need to charge Armenian VAT or file returns – effectively, the compliance burden shifts to the local buyer.

- Example: A U.S. consulting company provides advice to a large Armenian corporation that is VAT-registered. The U.S. company can provide its service without registering for VAT in Armenia; the Armenian corporation will account for the VAT via reverse charge on its VAT return. This arrangement is common for cross-border B2B services and ensures VAT is paid by the local company.

- Caution – verify customer status: A foreign supplier must be certain that the Armenian business customer is indeed a VAT-registered taxpayer. If the customer is not VAT-registered (perhaps they are under the threshold or on a special regime), the reverse charge does not apply and the foreign supplier would have needed to register. It’s a best practice for foreign vendors to obtain the VAT registration number of their Armenian business clients or otherwise confirm their VAT status. If a foreign company mistakenly treats a sale as reverse-charged when the Armenian client was not a VAT payer, the foreign company could be held liable for the unpaid VAT.

3. Foreign businesses with a physical presence in Armenia: If a foreign company opens a branch, office, warehouse, or other fixed establishment in Armenia and conducts taxable operations through that presence, it must register for VAT as a matter of course (usually as part of registering the business locally). Importantly, as noted earlier, foreign PEs do not enjoy the standard VAT registration threshold. A local Armenian company does not have to register for VAT until it exceeds a certain revenue (AMD 115 million) or voluntarily opts in, but a foreign-established entity (branch) must register from the outset of activities. Essentially, the act of having a taxable presence means you are a VAT payer from your first dram of sales. So, if your foreign company sets up a subsidiary or branch in Yerevan and starts making sales, you should apply for VAT registration immediately – do not wait to hit any sales threshold.

4. Importers of goods: When a foreign company imports goods into Armenia, VAT is generally collected at the border as import VAT. Typically, the importer of record (the person or entity in whose name goods are cleared through customs) is responsible for paying VAT to Armenian customs authorities at the time of import. If a foreign business is acting as the importer of record for its goods (for example, bringing in inventory to store and sell in Armenia), it will need to have a tax registration in Armenia (or use a customs broker). Often, foreign companies import through a local partner or have a local entity handle imports. But if not, the foreign entity will need to register to deal with the import VAT and subsequent sales VAT. Once those imported goods are sold within Armenia, charging VAT on the sale is required (unless the sale is to a VAT-registered buyer who might then reverse charge? However, sales of goods are generally not reverse-charged, reverse charge mostly applies to services). In short, foreign import-export traders should register for VAT if they are bringing goods into Armenia for resale or using them in Armenia, so they can properly pay import VAT and charge VAT on domestic sales (and potentially reclaim the import VAT as input tax).

5. Providers of electronic services: This deserves special mention because Armenia implemented specific rules from 2022. Non-resident providers of electronic/digital services to Armenian customers must register for VAT in many cases:

- For B2C electronic services (services delivered online to individuals in Armenia), the foreign provider must register and charge VAT from the first sale in Armenia – no threshold applies. Armenia uses several criteria (such as the customer’s residency, billing address, IP address, etc.) to determine if an electronic service is consumed in Armenia. If so, 20% VAT is due on the sale to the consumer.

- For B2B electronic services provided to an Armenian legal entity, two situations occur:

- If the Armenian business is VAT-registered, the reverse charge applies (the Armenian business self-accounts for VAT, and the foreign e-service provider does not register).

- If the Armenian business customer is not VAT-registered (e.g., a small company or NGO), then the foreign provider must register and charge VAT, similar to a B2C scenario. In effect, this aligns with the general rule we stated for all services, but Armenia has a dedicated online system to facilitate compliance for electronic services. So, digital businesses selling into Armenia should assume mandatory VAT registration for any direct sales to end-users in Armenia.

- If the Armenian business is VAT-registered, the reverse charge applies (the Armenian business self-accounts for VAT, and the foreign e-service provider does not register).

- If the Armenian business customer is not VAT-registered (e.g., a small company or NGO), then the foreign provider must register and charge VAT, similar to a B2C scenario. In effect, this aligns with the general rule we stated for all services, but Armenia has a dedicated online system to facilitate compliance for electronic services. So, digital businesses selling into Armenia should assume mandatory VAT registration for any direct sales to end-users in Armenia.

6. Threshold considerations: For local Armenian businesses, there is an annual turnover threshold (currently AMD 115 million in a year, roughly around €200,000) under which they are not obliged to be VAT payers and can opt for a simplified tax. However, this threshold does not exempt a foreign business making taxable supplies. Non-resident companies do not get a free pass up to AMD 115 million. If you are a foreign entity with no Armenian establishment and you make even modest sales to Armenian consumers, you are expected to register as soon as you start those sales (again, because the threshold only applies to those who can use the “turnover tax” regime, which excludes foreigners). Therefore, foreign businesses have no VAT registration threshold in practice – it’s either you have to register immediately (for B2C or non-VAT B2B sales) or you might not need to register at all (if exclusively supplying VAT-registered buyers who reverse charge). This is a critical difference to note.

Summary of when to register: To distill the above, a foreign business must register for Armenian VAT if:

- It sells goods or services in Armenia to individuals or entities that are not VAT-registered (no matter the sales volume).

- It establishes a branch or a fixed business location in Armenia that will make taxable supplies.

- It imports goods into Armenia for use or sale (in order to handle import VAT and subsequent sales).

- It provides electronic services to Armenian consumers (regardless of amount).

Conversely, a foreign business does not need to register if all its Armenian sales are made to VAT-registered companies under standard VAT – those local companies will handle the VAT via reverse charge. Also, if a foreign business only performs activities that are entirely VAT-exempt (for example, certain financial services or educational services might be exempt by law), then no VAT registration is required because no VAT is due on those supplies. However, exempt categories are limited; most commercial activities will be taxable or zero-rated.

VAT Registration Thresholds and Exemptions in Armenia

Registration threshold: Armenia’s Tax Code sets a VAT registration threshold of AMD 115 million in turnover (approximately $280,000) within the preceding or current calendar year. This threshold is primarily relevant to domestic businesses. If an Armenian business’s sales for the year stay below AMD 115 million, it is not automatically required to register for VAT. Instead, it can choose to be taxed under a simplified turnover tax regime (a gross receipts tax) at a lower rate instead of VAT. Once a local business’s revenue exceeds AMD 115 million in a year, it becomes mandatory to register for VAT and start charging VAT on its sales from that point forward.

- For local companies and individual entrepreneurs: The threshold works as an on/off switch between the turnover tax system and the VAT system. Many small businesses in Armenia operate under the turnover tax until they grow beyond the threshold.

- No threshold for foreign businesses: As emphasized earlier, foreign businesses cannot take advantage of this threshold in order to avoid VAT. The law does not provide any registration threshold or de minimis rule for non-resident suppliers. If the conditions for taxation in Armenia are met (e.g., you’re selling to a non-registered customer), VAT applies from the first sale, even if it’s a very small amount. This means a foreign digital service provider making one sale of $50 to an Armenian consumer is technically required to register and remit Armenian VAT on that sale.

- Voluntary registration: Both local and foreign businesses can voluntarily register for VAT even if not strictly required (though in practice foreign businesses required to register will have to anyway). A local small business under the threshold might opt into VAT to reclaim input VAT on expenses or to appear as a VAT-registered supplier to clients. A foreign company that engages only in B2B with VAT-registered customers typically doesn’t need to register, but could voluntarily register if it wanted to (though there’s usually no benefit in doing so, since those sales are handled by reverse charge; plus, the tax authorities might not allow a non-resident to register without a taxable reason).

Exemptions from registration: Armenia’s tax code does not provide specific exemptions from the obligation to register for those who are making taxable supplies. If you engage in taxable transactions that aren’t covered by reverse charge, you must register – there’s no additional carve-out. The only “exemption” is if your activities are entirely outside the scope of VAT or zero-rated:

- If a foreign business’s only activity in Armenia is selling goods that are exported (zero-rated supplies), or providing services that are zero-rated (e.g., certain services provided to clients abroad are zero VAT), it might not need to register because it isn’t making any taxed sales in Armenia. But this scenario is rare for a non-resident; typically a non-resident would only be involved in Armenian transactions if they are selling into Armenia (which is a taxable domestic supply).

- If the business only makes VAT-exempt supplies (for instance, financial services, education or healthcare services as defined by law, which are VAT exempt), then it is not required to register for VAT since no VAT is charged on those activities. However, purely foreign businesses rarely come to provide only exempt services; and importantly, digital services like streaming, SaaS, etc. are not exempt (they are taxable at 20%). So this exemption scenario mostly concerns certain sectors.

In summary, for foreign companies, the AMD 115 million threshold is not a safety net – it’s relevant for understanding the landscape (especially if you set up a local subsidiary, that local company would use the threshold rule). But as a non-resident vendor, assume no threshold and no automatic exemption: if you have to charge Armenian VAT, you must register regardless of sales volume.

One relieving point: Armenia currently does not require non-resident businesses to appoint a local fiscal representative to register. Unlike some countries that mandate a local agent or tax representative for foreign VAT registrations, in Armenia you can register directly with the tax authorities (State Revenue Committee) on your own. This simplifies the process and reduces costs of compliance for foreign firms.

Next, we’ll outline the step-by-step process to register for VAT in Armenia as a foreign business, and highlight any differences in procedure for various business types.

Step-by-Step VAT Registration Process for Foreign Businesses

Registering for VAT in Armenia as a foreign business involves several steps. The process will differ slightly depending on whether you are registering with a physical presence (like a branch) or as a non-resident digital/service provider using the online system. Below, we break down the general procedure and specific pathways:

1. Determine Your Eligibility and Timing

- Assess obligation: First, confirm that your business activities trigger the need for VAT registration. As discussed, if you will be making taxable sales to non-registered customers in Armenia, plan to register before commencing those sales or as soon as possible after you realize the obligation. If you are establishing a branch or office in Armenia that will trade, you should prepare to register that entity for VAT as part of the setup.

- Choose registration route: Armenia offers an electronic registration portal for non-residents (intended mainly for those providing electronic services to consumers). If that fits your case, you can use the online e-VAT system. Otherwise, you may need to register through the tax authorities by submitting forms (possibly electronically via email/website or in paper). If you are creating a local branch or subsidiary, registration typically occurs through the local tax office in parallel with business registration.

2. Prepare Required Information and Documents

To register, you will generally need to provide:

- Business details: Legal name of your business, address (for a foreign company, your head office address abroad), and possibly the address of any local activity if applicable.

- Identification numbers: Your home country registration number or tax ID, and any Armenian tax ID if one has been issued before. If you have a branch being registered, that branch will be recorded in the Armenian State Register and given a taxpayer identification number (TIN).

- Authorized person: Contact details of a representative who will handle the registration (this could be an employee or officer of the company). Even though a fiscal representative isn’t required, you’ll still need a local contact point or at least someone responsible for correspondence with the Armenian tax authority. Often this can be done by the company’s personnel remotely if using the e-system.

- Supporting documents: For a non-resident registering directly, Armenia may request documents such as a certificate of incorporation or extract from a commercial register proving your business exists, a copy of the company’s charter, and an ID for the signatory of the application. If registering a branch, you would supply the branch registration certificate from the Armenian authorities and the parent company’s documents. Any documents not in Armenian may need translation into Armenian (or possibly English documents are accepted for the e-VAT portal). It’s wise to have notarized/apostilled copies of key documents ready if doing a full registration via the tax office.

3. Submit the VAT Registration Application

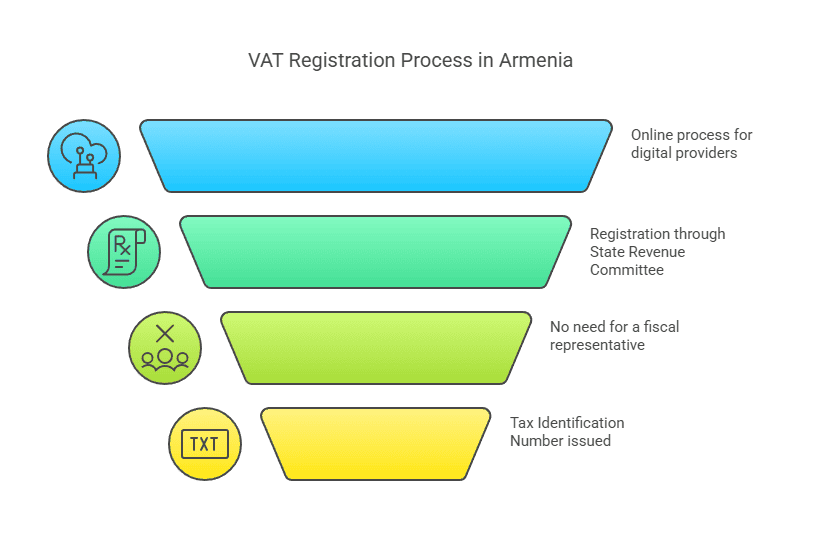

Non-resident digital service providers (using e-VAT portal): Armenia has a dedicated online portal for e-services VAT registration. This portal (often referred to as the eVAT system) is accessible via the official website of the Armenian tax authorities. The interface is available in English and Russian, making it user-friendly for foreign companies. Through this portal:

- You create an account as a foreign supplier of electronic services.

- The system will guide you to input your company details and upload any required documents electronically.

- A simplified electronic signature process is built-in, allowing you to sign the application digitally without needing a physical presence.

- Once completed, registration can be approved within minutes (according to the tax authorities). You will receive an Armenian taxpayer identification number (TIN) or VAT number and login credentials to use for ongoing filing.

This streamlined approach was introduced in 2022 to cope with the new wave of foreign digital businesses needing to register. If your business model is solely digital services to Armenian customers, this is the recommended route.

Other foreign businesses (goods, services, or with physical presence): If you are not just providing digital services, or you are an import/export business, or any scenario where the eVAT portal does not clearly apply, you may register by contacting the State Revenue Committee (SRC) of Armenia:

- The SRC handles tax registrations for all taxpayers. On their website, they provide forms and guidelines for taxpayer registration.

- You may be able to submit the application online via the SRC’s system as well. The SRC has an online taxpayer registration service for obtaining a TIN. This likely requires filling out an electronic form and attaching scanned documents.

- Alternatively, registration can be done through a local tax office or by mailing the application if electronic means are not available. Many foreign companies engage a local accounting/tax firm to assist with the process to ensure all formalities (like translations and correct form filling) are handled.

- For a foreign company establishing a branch, when you register the branch with the Armenian state register, the branch will be issued a TIN (tax ID) and that branch must then separately or simultaneously register for VAT since it will be a VAT-payer by default. In practice, the branch’s tax registration is often handled as part of the overall business registration process.

Note: When registering directly as a non-resident (especially outside the specialized e-service portal), ensure you clarify that it’s a VAT registration for a foreign entity. The tax authority will classify you appropriately. Since Armenia does not require a fiscal representative, you will be registering in your company’s own name.

4. Receive Tax Identification Number (TIN) / VAT Number

After successful application, the tax authority will issue a Tax Identification Number (TIN) for your business. In Armenia, the TIN serves as the VAT registration number as well. For companies, a TIN is typically a sequence of digits assigned to identify the taxpayer. Foreign businesses will get a number in the same format as local taxpayers. This VAT number is what you will use on invoices and in correspondence with the tax authorities.

If you used the e-VAT portal, you should get a confirmation of registration, and you’ll use your login credentials for future filings. If you applied via the general route, you may receive an official certificate or letter confirming your VAT registration and TIN. Keep this information safe, as you will need it for filing returns, making VAT payments, and proving your VAT status to any business partners.

5. Register for Online Tax Accounts (if not already)

Armenia’s SRC operates online systems for filing and paying taxes. Foreign taxpayers, once registered, should ensure they have access to these systems:

- If you went through the e-VAT system for digital services, then you already have access via that portal to file returns.

- If you registered through the general system, you should set up an account on the SRC’s online platform (often called “taxpayer personal account” or similar). This will allow electronic filing of VAT returns (in English or Russian if provided, or otherwise in Armenian – sometimes tax systems allow English forms for non-residents). The SRC online portal is important for ongoing compliance.

You may need to use the provided TIN and some initial password or procedure to activate your online account. The process is usually detailed by the SRC during registration.

6. Understand Specifics of Your Registration

Depending on your business type, note the specifics:

- Registration date effect: Your VAT registration becomes effective either from the date you requested or from the date you cross the threshold/started taxable supply. All taxable transactions from that point must include VAT. Ensure you do not charge VAT before you’re officially registered (since you wouldn’t have a number to report it with), but also don’t delay registration too long after you are required, or you could be liable for uncollected VAT.

- Local branch: If you registered a branch, that branch is now an Armenian taxpayer. It must keep separate accounts for its Armenian operations and comply just like a local company.

- Non-resident (no PE): If you registered just as a non-resident for certain transactions, remember that this registration only covers your obligation to collect Armenian VAT. It does not mean you’re subject to Armenian corporate income tax or other obligations unless you have a PE. In other words, registering for VAT doesn’t by itself create a taxable presence for income tax – it’s a compliance step for VAT only. (Of course, if you actually have a PE, you likely have other taxes too.)

7. Confirmation and Next Steps

Once registered, you are ready to start issuing invoices with Armenian VAT (where applicable) and collecting tax. The tax authority might provide guidance or a packet of information on filing and payment. At this stage, it’s prudent to consult a local tax advisor or thoroughly review the SRC’s guidelines to ensure you understand how to file your first VAT return and how to pay the VAT due from abroad. We will cover those compliance steps in the next section.

Processing time: The registration process for non-residents using the special portal is very fast (minutes to a day). For other methods, expect a processing time that could range from a couple of days up to a few weeks, depending on how quickly you provide any additional info requested. Generally, Armenia has been improving its administrative efficiency, and the fact that no fiscal representative is needed removes a potential delay.

Now that you have registered, let’s move on to your ongoing VAT compliance and reporting obligations as a foreign business in Armenia.

Ongoing VAT Compliance and Reporting Obligations

After registering for VAT in Armenia, foreign businesses must meet the same ongoing compliance requirements as any VAT-registered taxpayer. Below are the key obligations:

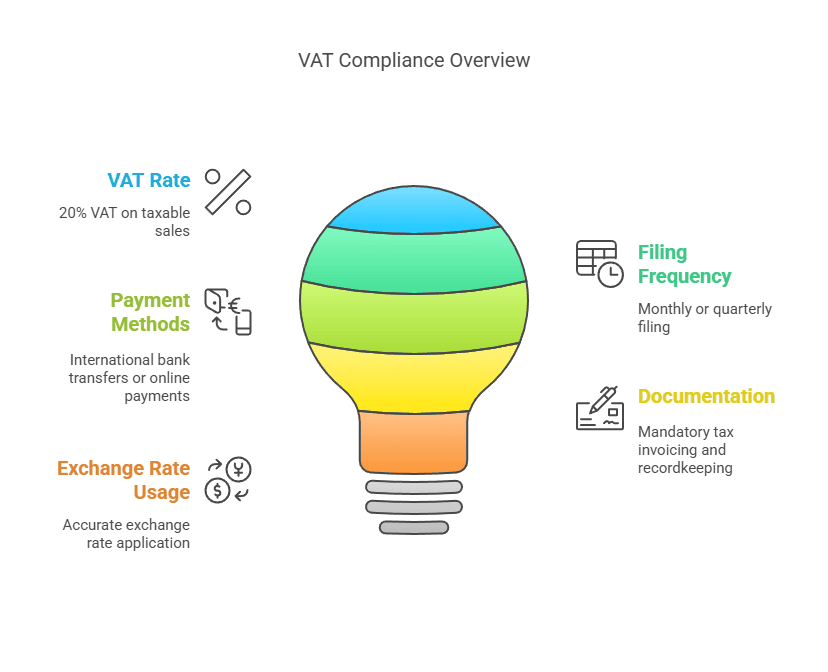

1. Charging and Collecting VAT: Once registered, you must charge Armenian VAT (20%) on all taxable supplies you make to Armenian customers (except those that are zero-rated or exempt by law). This means:

- Invoices: Issue proper invoices or receipts that include your Armenian VAT number and show the VAT amount charged. For B2B transactions, Armenian businesses will expect a “tax invoice” that meets Armenian requirements so they can potentially claim input VAT. For B2C transactions (e.g., digital services sold online), a simplified receipt showing VAT may suffice, but it’s good practice to maintain clear records of what you charged.

- Pricing: Ensure your pricing reflects VAT where applicable. If you advertised prices to Armenian consumers, clarify whether VAT is included or will be added at checkout. Many foreign digital services simply have VAT-inclusive pricing for simplicity.

- Currency: VAT in Armenia is computed in Armenian Drams (AMD). If you transact in another currency (e.g., USD or EUR), you will need to convert the sales amount to AMD for VAT reporting, using the exchange rate (official rate of Central Bank of Armenia) applicable on the date of supply or period end as per tax rules. Keep records of exchange rates used.

2. VAT Returns Filing Frequency: Armenian VAT returns are generally filed on a monthly basis. The standard rule for local VAT payers is that a VAT return must be submitted by the 20th day of the month following the reporting month. For example, January’s VAT return is due by February 20. This monthly filing applies to most cases, including foreign companies with a permanent establishment or those doing regular trade in goods/services.

However, there is a special concession for non-resident digital service providers using the e-VAT system: they are allowed to file quarterly VAT returns. In fact, Armenia aligned the reporting for these non-residents with common international practice (like the EU’s quarterly OSS/VAT returns). Thus:

- If you’re a non-resident only providing e-services to private individuals in Armenia through the special portal, you will file returns quarterly (four times a year). The quarters are Jan–Mar, Apr–Jun, Jul–Sep, Oct–Dec, and the return for each quarter is due by the 20th of the month following the quarter’s end. So Q1 (Jan–Mar) is due by April 20, and so on.

- If you also provide services to non-VAT registered businesses (legal entities) in Armenia, initially the law expected monthly returns for those transactions; but in practice, the e-VAT system now consolidates all your e-service sales into the quarterly return. So effectively, all your B2C and non-VAT B2B e-services can be reported quarterly.

For foreign businesses with a local branch or regular registration (not via the e-service portal), expect monthly filing requirements, as you’d be treated like any Armenian company. There is no option to file quarterly in that standard regime.

3. Payment of VAT: Payment of any VAT due must accompany the filing:

- The deadline for payment is the same as the return deadline (20th of the following month or quarter). By that date, the VAT you’ve charged in the period must be remitted.

- The e-VAT portal provides convenient payment options: you can pay via bank transfer to the Armenian Treasury in various foreign currencies (they accept several major currencies and will convert to AMD) or even pay by credit/debit card directly through the portal interface. This means you do not need an Armenian bank account to pay your VAT liabilities – a very helpful feature for non-residents.

- If you file through the standard system, you will likely pay by international bank transfer to a designated account of the Armenian state budget. Ensure to use your TIN and the correct payment codes so that the payment is credited to your tax account. Payment should be in AMD; if sending a different currency, your bank will convert it, possibly incurring fees. It’s crucial to initiate the transfer a few days before the deadline to account for any international banking delays.

- Late payment will incur interest (currently, Armenian law sets penalty interest at 0.075% per day of the unpaid tax as of 2025, which is roughly 27% annualized, up to a certain cap), so timely payment is important.

4. Record-Keeping: VAT-registered businesses must keep detailed records of:

- All sales made that are subject to Armenian VAT, including date, customer details (if B2B), amount, VAT charged.

- All purchase invoices where Armenian VAT was paid (if you have any, see Input VAT below).

- Import/export documents, if applicable, to reconcile any import VAT paid or exports (zero-rated sales).

- Any credit notes or adjustments issued.

- These records should be retained for a number of years in case of audit. Armenia generally requires taxpayers to maintain records for at least 3-5 years (five years is a common standard, though check local law; many companies keep VAT records for at least five years).

If you are using the e-VAT system, much of your reporting is simplified, but you should still keep an internal log of transactions that were taxed. If the tax authority ever inquires, you’ll need to provide supporting data.

5. Input VAT and Deductions: One of the benefits of VAT is the ability to claim input VAT credits on business expenses. However, this aspect may be limited for foreign businesses:

- A non-resident digital service provider with no physical presence in Armenia likely has no local input VAT to claim (since it probably doesn’t incur Armenian VAT on its expenses abroad). That business will simply remit the VAT collected on sales, with no offset.

- A foreign company that imports goods or incurs expenses in Armenia (e.g., a trade fair fee that had Armenian VAT, or local supplier costs at 20%) can claim input VAT on those costs, provided they are a registered VAT payer and the costs relate to their taxable activities. For instance, if your registered branch buys office supplies in Armenia and pays AMD 100,000 + VAT (AMD 20,000) to a local vendor, that AMD 20,000 can be taken as input credit on your VAT return.

- One important limitation: If a business is not established in Armenia (no PE) and just registered for VAT, Armenia does not generally allow refunds of excess VAT or input credit carryovers for that non-established entity. In fact, many countries restrict VAT refunds to non-established businesses unless reciprocal agreements exist. Armenia’s system for non-residents is mostly to collect output VAT; it may not entertain refunding input VAT to a non-resident easily. (There is no formal “VAT refund for foreign businesses” scheme published for Armenia as, say, in the EU for non-EU companies).

- That said, if you have a local branch or subsidiary, it is treated like a local company and can claim input VAT and get refunds if it ends up in a refund position (for example, exporters who have more input VAT than output VAT can get refunds in Armenia).

6. Invoicing Requirements: If you are a foreign business issuing invoices under your Armenian VAT number:

- Include your Armenian TIN/VAT number on the invoice.

- If selling to a VAT-registered Armenian customer, also include their VAT number and indicate that VAT was charged (or if reverse-charged, indicate “VAT reverse-charged by customer”). In B2B cases where you are charging VAT (which would only happen if the customer isn’t VAT-registered), you must give an invoice so that the customer has proof of VAT paid (though they cannot reclaim it since they’re not in the system, but it’s for their records).

- Show the VAT amount in Armenian drams. You might show the sale in foreign currency and then the equivalent AMD and VAT.

- Armenian tax invoices have specific sequential numbering and formatting in local language when issued by Armenian companies. As a foreign supplier using an online platform for B2C, you won’t follow local language format, but for any official transactions you should try to comply as much as possible with invoice best practices.

- Keep a copy of all invoices/receipts issued, as the tax authority could request to see them.

7. Returns and Payment Reporting: File your returns through the appropriate online system. The VAT return will summarize:

- Total taxable sales in Armenia for the period and output VAT due.

- Total taxable purchases (if any) and input VAT claimed.

- Net VAT payable or refundable. (In most foreign non-established cases, this will simply be the output VAT payable.)

- Zero-rated or exempt sales can also be reported in the return (though likely zero for a foreign company unless exporting via its branch).

Make sure to submit by the deadline. The Armenian SRC e-filing system will usually provide a confirmation or reference number once you file. If you realize an error in a filed return, Armenian law allows corrections (often via an amended return or adjustment in a subsequent period, depending on the nature of the error). Promptly correct any mistakes to avoid penalties.

8. Local Representation (Optional): While not required, some foreign businesses opt to appoint a local accounting firm or consultant to handle ongoing VAT compliance – especially if language barriers or complexities arise. Since filings are periodic and rules can change, having local expertise can be useful. They can also interface with the tax authorities if any issues or audits occur.

9. Other taxes: Keep in mind that VAT is separate from other taxes. If you have a branch, you may also have to file profit tax returns annually, etc. But if you’re just a non-resident VAT payer, you typically only worry about VAT (and perhaps any withholding taxes for specific income streams).

By staying on top of these compliance tasks – timely filings, accurate VAT charging, and proper record-keeping – foreign businesses can operate in Armenia without incurring penalties or compliance risks. Speaking of which, let’s discuss the common pitfalls and risks of non-compliance with Armenian VAT rules, and the potential penalties for mistakes or failure to comply.

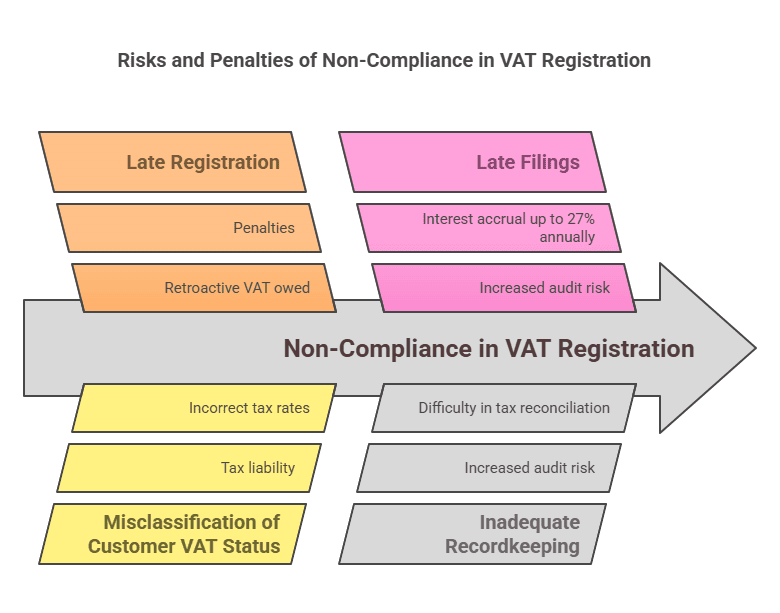

Common Compliance Risks and Penalties

Operating in a foreign tax jurisdiction can be challenging, and businesses may inadvertently run into compliance issues. Here are some common risks for foreign companies regarding Armenia’s VAT, and the consequences if obligations are not met:

1. Failure to Register on Time: One of the biggest risks is simply not realizing you needed to register. A foreign company might start selling to Armenian customers (especially online) and not be aware of Armenian VAT law. If you delay registration past the point of requirement, unreported VAT liability will accumulate. The tax authority can later assess the VAT that should have been collected on your past sales. The foreign business would then have to pay that out of pocket (since it likely didn’t charge it to customers initially), which directly impacts your revenue from those sales. Additionally, late registration or non-registration itself can incur penalties.

2. Incorrect Application of Reverse Charge vs Charging VAT: Misclassifying your customers can lead to errors. For example, treating a sale as B2B reverse-charged (not charging VAT) when the Armenian client was not actually a VAT registrant means no one paid VAT on that transaction. If audited, the authorities will hold the supplier responsible for that VAT. Conversely, charging VAT to a VAT-registered customer (when it should have been reverse charged) can create confusion; the customer might refuse to pay the VAT or you might have to refund it and adjust the procedure. Always verify customers’ VAT status. Obtain their Armenian VAT number if they claim to be VAT-registered. The Armenian tax authority issues VAT numbers to registered taxpayers – these can be validated through official sources or with help of the customer’s VAT certificate.

3. Not Charging VAT When Required (Undercharging): If a foreign business neglects to charge VAT to consumers when it should, it can’t later easily go back to customers to collect it. That means if discovered, the foreign business must pay the 20% VAT itself on those past sales, effectively losing 20% of that revenue. This is a direct financial hit and is considered tax evasion/non-compliance until rectified.

4. Late Filing or Non-Filing of VAT Returns: Missing a filing deadline can result in penalties. Armenian tax law imposes fines for failure to file or late submission. While exact penalty amounts can vary, typically a fixed fine or a percentage of the VAT due might be charged. Moreover, each day overdue can accrue penalty interest on any unpaid tax. For instance, as of 2025 the penalty interest rate is 0.075% per day on outstanding tax. That adds up quickly – nearly 2.25% per month. There is usually a cap (interest might stop accruing after 2 years), but no business wants to pay 50%+ extra because of a late payment or filing.

5. Errors in VAT Calculation: Exchange rate mistakes, arithmetic errors, or misunderstanding what is taxable can occur. If you accidentally undercalculate VAT (e.g., used an outdated exchange rate leading to less AMD reported), the difference could be assessed later with interest. Always double-check calculations and use official exchange rates. If language barriers cause misunderstanding of exempt vs taxable items, consult local experts to avoid misapplying a zero rate or exemption.

6. Poor Record-Keeping: If audited (tax audits can happen at random or if something triggers it), you will need to produce documentation for your transactions. Not having invoices, receipts, or contracts to support your VAT filings is a risk. The tax authority could disallow input credits or even estimate your sales if records are insufficient, often to the detriment of the taxpayer. Keeping clear digital and physical records of all Armenian-related sales and purchases is the best defense.

7. Ignoring Local Correspondence: As a foreign business, you must ensure that any communications from the Armenian tax authorities (which might be in Armenian) are addressed. If you provided an email or local address during registration, monitor it. Missing an audit notice or a request for information can lead to penalties or assessments by default. If language is an issue, have a translator or local representative check any official notices.

8. Penalties and Fines: Armenia’s Tax Code outlines various penalties:

- Late payment interest (mentioned above) which increases the longer tax remains unpaid.

- Fixed fines for late filing or failure to file a VAT return. For example, there might be a flat fine per overdue return or a percentage of the overdue VAT. (As an illustration, if a return is late by more than a certain number of days, a penalty of say 5% of the tax due might be levied, increasing if delays continue – the exact figures can change, so one should check the latest code, but the principle stands that lateness costs money).

- Penalties for tax understatements: If an audit finds that you underreported VAT (whether by error or intentional), they can impose a penalty on the underreported amount, often a percentage (e.g., 20% or more), on top of collecting the tax and interest. If there’s evidence of deliberate evasion, penalties can be harsher.

- In extreme cases of tax evasion or fraud, legal consequences can include further fines or even criminal charges (though for a foreign company selling remotely, that is unlikely unless large sums are involved and willful evasion is proven).

9. Compliance Risks for Specific Business Types:

- Digital services: One risk is not meeting the place-of-supply criteria properly. Armenia uses multiple criteria to decide if a service to an individual is consumed in Armenia (residence, IP address, payment method country, etc.). A business must have processes to collect this info. For example, if an individual’s billing address is Armenian but they’re actually living elsewhere at the time of service and you have conflicting indicators, you need a consistent policy. The tax authority could challenge if you are not charging VAT to someone with Armenian indicators. It’s safer to charge Armenian VAT whenever in doubt for B2C digital sales with Armenian connections, to avoid missing tax.

- E-commerce goods: Logistics and customs can be tricky. If you rely on the customer to import the goods (deliver DDU – duties unpaid), then the customer pays VAT at customs and you don’t charge it. But if you deliver DDP (delivered duty paid) or maintain stock in Armenia, ensure you handle import VAT correctly. Not doing so could mean goods get stuck at customs or you end up paying penalties for mis-declaration. Also, if using couriers, make sure they know who is responsible for the VAT.

- Services with intermittent presence: If you send staff to Armenia to perform a project over many months, you might inadvertently create a PE (if over 183 days, etc.) which would mean you should have registered not just for VAT but possibly as a branch for all taxes. This is beyond just VAT compliance – it’s corporate tax compliance too. To mitigate, plan projects carefully and consult on whether a formal registration is needed if your personnel will be in-country extensively.

10. Currency and Repatriation: Ensure you convert and pay VAT in the correct amount of AMD. Overpaying due to conversion errors is also a risk (though that just ties up your money until corrected). And do not attempt to pay in a foreign currency unless using the official allowed methods – paying in the wrong way could result in the payment not being recognized properly.

In essence, the biggest risk is lack of awareness – which this guide aims to eliminate. The penalties for non-compliance can be significant, but they are avoidable. Armenian tax authorities are increasingly sophisticated (especially with the new digital systems in place) and can track digital transactions and imports, so it’s unwise to assume a small foreign business will fly under the radar indefinitely.

Mitigation tips:

- Register early once you know you need to, and err on the side of caution with B2C sales.

- Consult local experts if anything is unclear; a modest advisory cost can save huge penalty costs.

- Use the e-VAT system if applicable – it simplifies compliance and reduces error potential.

- Monitor regulatory changes: Tax laws can change. For instance, thresholds could update, or new rules for marketplaces might emerge. Staying informed (through tax news or local partners) ensures you remain compliant in the future.

Comparison of VAT Requirements by Business Type

To illustrate how VAT registration requirements differ by type of foreign business, see the comparative table below:

Foreign Business Type | When VAT Registration is Required | VAT Threshold | VAT Return Frequency | Special Notes |

|---|---|---|---|---|

Digital service provider (no local presence, e.g. SaaS, streaming) | Must register if providing digital services to Armenian individuals or non-VAT businesses (from the first sale in Armenia). Not required if only selling to VAT-registered companies (B2B reverse charge applies). | No threshold (VAT due on all B2C sales from first dram). The general AMD 115m threshold does not apply to non-residents. | Quarterly (via e-VAT portal) for B2C services. If also selling to non-VAT businesses, those are included in quarterly filings. | Use Armenia’s e-VAT online portal for quick registration and filing. No local representative needed. VAT at 20% on digital services. |

E-commerce retailer (goods) (no local entity, selling goods into Armenia) | If goods are sold delivered in Armenia to consumers (and the foreign seller is responsible for import or local delivery), must register to charge VAT on the sale (unless VAT is collected at import). If selling only to Armenian businesses that import the goods themselves under their VAT number, registration not needed (the import VAT and reverse charge covers it). | No specific threshold for requiring registration for goods sales. Any regular direct selling to consumers would trigger VAT obligations. | Monthly (most likely), since these sales fall under normal VAT rules (the e-VAT portal is mainly for services). | Import VAT: Usually paid at customs. The foreign seller should be importer of record or ensure the customer pays it. No special distance selling threshold – treat every B2C sale as VAT-applicable. |

Foreign service company (non-digital) (e.g., consulting, engineering, event services, with no fixed base in Armenia) | Must register if performing services in Armenia for non-VAT clients or charging fees to Armenian individuals or non-VAT entities. Not required if all clients are VAT-registered businesses (they’ll reverse charge). | No threshold; any taxable service to a non-registered customer triggers requirement. | Monthly (since you’ll register under normal regime). | If physically present in Armenia for projects, monitor PE status (183 days rule). A long project might force a full branch registration. Short-term projects for individuals require VAT registration as non-resident. |

Foreign company with a physical presence (branch or subsidiary in Armenia) | Must register as a VAT payer as soon as the local entity is established and before making any taxable sales. (Branches of foreign companies cannot use the small business exemption.) | No threshold for branches of foreign companies – they are treated as VAT taxpayers from day one. (A local subsidiary, being an Armenian company, would have the threshold available if independent – but if foreign-owned and likely above threshold, it will register immediately too.) | Monthly (all local entities follow standard monthly filing). | Branch or PE registration typically occurs with business registration. They will charge VAT on local sales, can claim input VAT, and must follow all Armenian accounting rules. |

Import/Export trader (foreign business importing goods into Armenia for resale, or exporting from Armenia) | Importing for resale: Must register to handle import VAT and charge VAT on domestic sales. Exporting from Armenia: If a foreign entity somehow exports goods from Armenia (zero-rated sales abroad), registration is needed to reclaim any input VAT in Armenia (since exports are 0% VAT, but you want to get refund of VAT on costs). | No threshold; registration needed based on activity, not volume. | Monthly. If regularly importing/selling, monthly returns reporting imports (as input VAT) and local sales (output VAT). | Coordination with customs is key. Exports are VAT-free but require documentation to prove goods left Armenia. Importers can credit the import VAT on their VAT return if properly registered. |

This table highlights that virtually all foreign business types have no minimum threshold – the duty to register hinges on who you sell to and how you operate, rather than how much you sell (unlike domestic small businesses). Digital service providers benefit from a simplified quarterly system. E-commerce and other non-resident services follow the regular regime. Physical presence anchors you in the local system fully.

Summary

Armenia welcomes foreign businesses but expects them to comply with local VAT laws when doing business in the country. In summary, VAT registration for foreign businesses in Armenia is required whenever a non-resident is making taxable supplies on Armenian soil to customers who cannot themselves account for VAT. There is a standard VAT rate of 20%, and generally no registration threshold applies to non-residents – unlike local small businesses, foreign companies must account for VAT from their first taxable transaction in Armenia (outside of purely B2B-with-VAT-payer scenarios).

Foreign digital service providers have been specifically brought into the VAT net since 2022 and can register and file easily via an online portal. Other foreign businesses (like those dealing in goods or other services) either register a local branch or register directly with the tax authorities to obtain a VAT number. Once registered, ongoing compliance – filing VAT returns (monthly or quarterly as applicable), paying taxes by the due date, issuing proper invoices, and keeping records – is crucial to avoid penalties.

Armenia does not require a fiscal representative, making it simpler to register and manage VAT obligations as an overseas entity. However, compliance should not be taken lightly: failing to register or to charge VAT when required can result in back taxes, fines, and interest that erode your profits and goodwill. On the flip side, timely compliance allows foreign businesses to operate in Armenia’s market on an equal footing with local businesses, with the ability to charge VAT and (if applicable) reclaim VAT on costs.

In closing, understanding the VAT registration requirements for foreign companies in Armenia ensures you can expand or serve Armenian clients without unexpected tax surprises. Register when required, follow the procedures, and keep accurate records. With that approach, Armenia’s tax system is manageable and transparent. The FAQ below addresses some common questions that foreign businesses often have about Armenian VAT in practice.

FAQ: Armenia VAT Registration for Foreign Businesses

Q1. Do foreign companies need to register for VAT in Armenia?

A: Yes, a foreign (non-resident) company must register for Armenian VAT if it is making taxable supplies in Armenia to customers who are not themselves registered for VAT. This commonly includes sales to Armenian private individuals (B2C sales) and sales to Armenian businesses that are too small to be VAT-registered. For example, if you are a foreign software-as-a-service provider selling to Armenian consumers, you need to register and charge Armenian VAT. On the other hand, if you only sell to large Armenian companies that are VAT-registered, you generally do not register – those Armenian companies will self-account for VAT under the reverse charge mechanism.

Q2. What is the VAT registration threshold in Armenia for non-resident businesses?

A: There is effectively no sales threshold for foreign businesses. The standard threshold of AMD 115 million turnover per year applies to Armenian resident businesses (allowing them to avoid VAT until they grow larger). Foreign businesses cannot use that exemption. If a non-resident has any obligation to charge Armenian VAT, it must register from the first taxable sale – whether that sale is worth AMD 1 or 100 million. So, non-residents should not wait to reach a certain revenue level; they should register as soon as they know they will be making taxable supplies in Armenia that require it.

Q3. If I only sell to Armenian businesses (B2B), do I need to register?

A: Not if those Armenian businesses are VAT-registered. In a pure B2B scenario where every client in Armenia is a VAT payer, you as the foreign supplier do not charge VAT and do not need to register. The Armenian client will handle the VAT via reverse charge. However, if even one of your Armenian business clients is not VAT-registered (for instance, a small LLC not in the VAT system), then for that client you would need to charge VAT – meaning you’d need a VAT registration. In practice, many foreign B2B suppliers stay unregistered by ensuring their Armenian clients are all VAT-registered. It’s wise to obtain the VAT number of each client to have on file. If you cannot verify a client’s VAT status and they purchase from you, it’s safer to register and charge VAT than risk non-compliance.

Q4. What is the VAT rate that foreign businesses must charge in Armenia?

A: The VAT rate is 20%, which is the same for foreign and local businesses. Armenia has a single standard VAT rate of 20% on most products and services. Some supplies are zero-rated (0%) such as exports or international transportation, and some are exempt (financial services, etc.), but if your activity is standard commercial sales in Armenia, you will be charging 20% VAT. There are no special reduced rates in Armenia’s VAT regime as of 2025.

Q5. Do I need an Armenian fiscal representative or local agent to register for VAT?

A: No, Armenia does not require foreign taxpayers to appoint a fiscal representative for VAT. You can register directly with the Armenian tax authorities. The process has been made quite straightforward with the introduction of the e-VAT portal for non-resident e-service providers. While you may choose to hire a local consultant to help navigate the process or manage filings, it’s not a legal requirement. The VAT registration will be in your company’s name, and you will liaise directly with the tax authority.

Q6. How can a foreign company pay its Armenian VAT liabilities from abroad? Do I need an Armenian bank account?

A: You do not need a local bank account. The Armenian tax authority provides options to pay remotely:

- Through the e-VAT online system (for those registered there), you can pay by credit card or via international bank transfer in one of several accepted currencies. The system provides the necessary bank details and references to include. Card payments are processed instantly.

- For those filing in the regular system, you can arrange an international wire transfer to the Armenian Treasury’s account. They typically allow payment in foreign currency (USD, EUR, etc.) which will be converted to AMD. As long as you use your tax I.D. and the proper payment code, the payment will be credited to your VAT account. Make sure to initiate payment ahead of the deadline to allow for any transfer time. The flexibility of payment methods means settling your tax from overseas is relatively convenient.

Q7. Is there any exemption from VAT for digital services or small foreign businesses?

A: No special exemptions exist for digital services – in fact, digital services are explicitly taxable at 20% if consumed in Armenia. There are also no special exemptions for “small” foreign businesses beyond what we discussed (the threshold which doesn’t apply to them). All digital goods and services (like streaming, software, e-books, online advertising to local users) are subject to VAT. Only if the nature of the service itself is exempt under general VAT law (for example, maybe certain financial services or insurance) would it be not subject to VAT. But common digital services do not fall under exemptions. So, a foreign app seller or streaming service must charge VAT on sales to Armenian consumers regardless of their size or volume of sales.

Q8. How long does VAT registration take for a non-resident business in Armenia?

A: It can be very quick, especially for digital businesses using the online system. The e-VAT portal registration can be completed in a matter of minutes once you input all required information, and your account becomes active almost immediately. For other types of registration (through the SRC office), it might take a few days to a couple of weeks to process, depending on the completeness of your application and whether any manual review is needed. In most cases, you should expect confirmation within 1-2 weeks maximum. Planning ahead is important: don’t wait until you have a large transaction imminent. Start the registration process as soon as you determine you need it, so that you’re ready to charge VAT legally when sales commence.

Q9. What records do I need to keep for my Armenian VAT?

A: You should keep all records related to your Armenian transactions:

- Sales invoices or receipts showing VAT charged.

- Evidence used to determine the location of your customer (for digital services, logs of IP address, billing address, etc., in case you need to justify why you charged or didn’t charge Armenian VAT).

- Import documents and purchase invoices if you are importing or incurring Armenian VAT on expenses, to support any input VAT claims.

- VAT returns filed and proof of VAT payments made. These records should be kept for at least five years (to be safe) following the tax year, as audits can look back several years. Digital copies are acceptable, but ensure they are backed up and can be provided on request. Good record-keeping helps you defend your tax position and also simplifies the preparation of your VAT returns.

Q10. What happens if I don’t register for VAT in Armenia, even though I should?

A: If you ignore the requirement to register and continue making taxable sales in Armenia, you run significant risks:

- The Armenian tax authorities could identify your activities (for instance, through monitoring of cross-border digital services or customs records for goods) and contact you or your local customers. They may issue an assessment for the VAT that should have been paid.

- You would likely be charged the VAT due retroactively on those sales, plus penalties and late payment interest on the amounts. This can considerably increase the cost – for example, a year’s worth of unpaid VAT could accrue roughly ~27% in interest on top, plus possible fines.

- Your local customers might also be impacted. For example, if you sold goods and didn’t pay import VAT properly, those customers might have trouble clearing shipments.

- Non-compliance can tarnish your company’s reputation and could lead to legal enforcement. While Armenia might have limited reach to enforce against a company with no presence, they could coordinate internationally or detain company officials if they enter Armenia, in extreme cases of tax evasion. In short, it’s not worth operating under the radar. It’s best to voluntarily comply – Armenia has made it easier through online systems, and by complying you avoid these risks entirely.

Q11. Can a foreign company use Armenia’s turnover tax (simplified tax) instead of VAT?

A: No, foreign companies (and their Armenian branches) are excluded from the turnover tax regime. The turnover tax (a simplified tax in lieu of VAT and profit tax for small businesses) is only available to Armenian-resident individual entrepreneurs and organizations that meet criteria, and specifically not available to non-resident legal entities or their PEs. Therefore, a foreign business must go the standard VAT route; you cannot opt for the 5% turnover tax instead of charging 20% VAT. If a foreign investor wants to benefit from small business rules, the only way would be to create a local company that is independent – but even then, if that local company is foreign-owned, certain restrictions might apply. In general, assume that any foreign involvement puts you in the normal VAT system.

Q12. Are there special VAT rules for online marketplaces or platforms in Armenia?

A: Currently, Armenia does not have specific “marketplace” VAT rules like the EU or some other countries do. There is no concept of deeming an online marketplace as the supplier for third-party sales or requiring marketplaces to collect VAT on behalf of others, as of 2025. Each foreign seller is responsible for their own VAT compliance. However, Armenia did consult major marketplaces during the introduction of e-services VAT, and it’s possible that in the future regulations could evolve. For now, if you run an e-commerce platform:

- If the platform itself is the seller of record (buying and reselling goods/services to Armenians), then the platform is treated as any seller and must register for VAT if selling to consumers.

- If the platform merely connects buyers and sellers and takes a commission, the sellers (even if foreign) are the ones responsible for VAT on the sales, and the platform’s commission is another service (possibly subject to VAT depending on where the platform is located and if the seller is in Armenia or not). In practical terms, big platforms like Amazon or eBay, if directly selling to Armenia, would register and charge VAT. Smaller marketplaces should make sure their foreign sellers are aware of Armenian VAT obligations. Always keep an eye on law changes, as many countries are shifting some responsibilities to platforms for tax collection.

Q13. How does VAT work on imports into Armenia by foreign businesses?

A: VAT on imports into Armenia is usually collected by customs at the border. The rate is 20%, applied to the customs value of the goods plus any customs duty. If you as a foreign business are the importer of record (meaning the goods are declared in your name), you will need to pay that import VAT to clear the goods. If you’re registered for VAT in Armenia, you can later claim that import VAT on your VAT return as input tax (effectively offsetting it against the VAT you charge on sales). If your Armenian customer is the importer of record (goods shipped DDU and they handle customs), then they pay the import VAT, and if they are VAT-registered they can claim it. As a foreign seller, you wouldn’t charge VAT on the invoice in that scenario because the tax was handled at import.

For exports (goods leaving Armenia), VAT is 0% (zero-rated) provided the export is properly documented (customs export declaration, etc.). Usually, foreign companies would only be involved in exporting from Armenia if they have a presence (like a branch buying goods locally and then exporting). In that case, the branch would charge 0% VAT on the export sale and could reclaim any input VAT incurred on local purchases related to the export.

Q14. How does Armenia’s VAT compare to neighboring countries or the EU for foreign businesses?

A: In principle, Armenia’s approach is similar to many countries:

- The 20% rate is in line with international norms.

- The concept of requiring non-residents to register for B2C sales is similar to the EU’s approach for digital services after 2015, or other countries implementing “VAT on digital services” regimes.

- Unlike the EU, Armenia doesn’t yet have an OSS (One-Stop Shop) union-wide system, but since it’s just one country, your compliance is contained to Armenia.

- Armenia not requiring a fiscal rep is a bit more lenient than some countries (like in some cases in EU or Asia where a local agent is mandatory).

- The high threshold for local businesses (AMD 115m) is generous, but as noted, doesn’t apply to foreigners. One difference in Armenia is the quarterly filing for non-resident e-services, which is convenient and shows flexibility. The compliance burden is manageable, especially given the online tools in English/Russian. In summary, foreign businesses might find Armenia’s VAT rules relatively straightforward once understood, and broadly consistent with global VAT/GST practices.

By addressing these FAQs, we hope foreign entrepreneurs and advisors have clarity on practical points. Armenia’s VAT system, while detailed, is not impenetrable. With the information in this guide, foreign businesses can confidently assess their VAT duties in Armenia, ensure they register when needed, and maintain compliance, thereby avoiding any tax pitfalls while tapping into the Armenian market.