Armenia's microbusiness tax regime has garnered significant international attention for its exceptional 0% tax rate on qualifying businesses with annual turnover under AMD 24 million (approximately $60,000). However, not all business activities are eligible for this favorable tax treatment. Understanding the specific qualification criteria is essential for entrepreneurs considering this structure. In this comprehensive guide, we'll examine exactly which business activities qualify for Armenia's tax-free microbusiness status and which are explicitly excluded, helping you determine whether your business model fits within this tax-advantaged framework.

Ready to establish your tax-free Armenian microbusiness? Click here to access our complete registration guide and discover how to determine if your business qualifies.

Understanding Armenia's Microbusiness Qualification Framework

Before examining specific eligible and excluded activities, it's important to understand the fundamental qualification criteria for Armenia's microbusiness tax regime:

Primary Qualification Requirements

- Annual Turnover Limit: Must not exceed AMD 24 million (approximately $60,000)

- Eligible Entity Types: Commercial organizations (LLCs), sole proprietors, or individuals without formal business registration (for specific activities)

- Registration: Must submit certification statement to tax authorities and renew annually

- Activity Restrictions: Business activities must not fall into excluded categories

Tax Benefits for Qualifying Businesses

- 0% Corporate Income Tax (standard rate: 18%)

- 0% Value Added Tax (VAT) (standard rate: 20%)

- 0% Turnover Tax (standard rates: 1.5%-10%)

- No advance tax payments required

- Minimal reporting requirements (simple annual filing)

Note: While the business itself is exempt from taxation, dividend distributions to shareholders are subject to a 5% withholding tax.

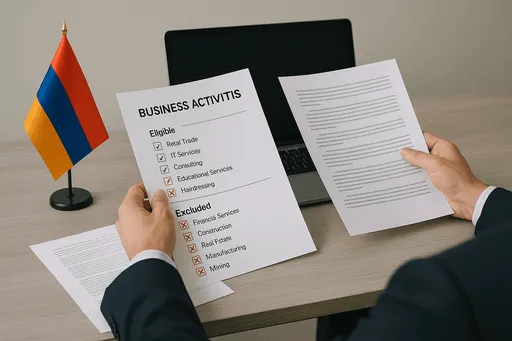

Excluded Business Activities: What Doesn't Qualify

Armenia's microbusiness legislation specifically excludes certain activities from qualifying for the tax-free status, regardless of whether they meet the turnover threshold. Understanding these exclusions is the first step in determining eligibility:

Financial and Investment Services

The following financial service providers are excluded:

- Banks and credit organizations

- Insurance companies, agents, and brokers

- Investment companies and fund managers

- Securities market professionals

- Pawnshops

- Currency exchange businesses

- Payment processing organizations

Professional Services

Professional service providers that cannot qualify include:

- Consulting services

- Legal services

- Accounting and auditing services

- Engineering services

- Advertising and marketing services

- Design services

- Translation services

- Expert evaluation and examination services

- Medical services and dental technicians

- Software development

- Information processing and transmission services

- Real estate brokerage and valuation

Trade and Commercial Activities

Trading activities excluded from microbusiness status:

- Wholesale and retail trading businesses

- E-commerce businesses

- Car dealerships

- Marketplace operators and intermediaries

- Businesses trading in dedicated facilities, shopping centers, or fairs

- Organizations and sole proprietors supplying goods to other businesses

Other Excluded Activities

Additional business types that cannot qualify:

- Notaries

- Gambling, casino, and lottery operators

- Public transportation providers

- Saunas, baths, and steam bath operators

- Public catering in Yerevan (with exceptions)

- Scientific research and experimental development

- Construction and architectural design

- Organizations receiving rental income, interest, or royalties

- Vending machine operators

- Coin-operated gambling machine operators

Eligible Business Activities: What Qualifies for Microbusiness Status

Now that we've covered what's excluded, let's examine the business activities that typically qualify for Armenia's microbusiness tax regime. These opportunities are particularly relevant for location-independent entrepreneurs, online businesses, and digital professionals:

Digital Creation & Artistic Services

Content creators and artists producing their own work:

- Digital art and illustration creation (not design services)

- Music composition and production

- E-book authoring and self-publishing

- Voice acting and narration

- Content creation (non-marketing)

- Original digital product creation

- Photography (artistic, non-commercial)

- Videography and film production (original content)

Key distinction: These activities must involve creating and selling one's own work rather than providing creative services to clients.

Educational Services

Teaching and knowledge dissemination activities:

- Online tutoring and coaching

- Language teaching

- Course creation and delivery

- Skill instruction and training

- Educational content development

- Knowledge sharing services

- Workshop facilitation

- Specialized training in arts, crafts, or skills

Key distinction: Focus must be on direct teaching or educational content creation rather than educational consulting.

Performance & Entertainment

Performance-based activities and entertainment services:

- Storytelling and performances

- Musical performances

- Virtual experience hosting

- Poetry and literary performances

- Character acting services

- Cultural demonstrations

- Personal coaching (non-consulting)

- Artistic exhibitions and showcases

Key distinction: These should be direct performance services rather than event management or consulting.

Administrative & Support Services

Back-office and administrative support activities:

- Virtual assistance (administrative)

- Data entry services

- Transcription services

- Document preparation (non-legal)

- Community moderation

- Basic administrative support

- Appointment scheduling

- Basic research assistance (non-professional)

Key distinction: These should be basic administrative services, not specialized professional services or consulting.

Manufacturing & Production

Small-scale production activities:

- Handicraft production

- Small-scale manufacturing

- Custom product creation

- Artisanal food production

- Textile creation and clothing production

- Jewelry making

- Furniture creation

- Artisanal goods production

Key distinction: Focus must be on creating products rather than reselling purchased goods.

Specialized Repair Services

Repair and maintenance activities:

- Repair of watches and time measuring devices

- Musical instrument repair

- Clothing and textile repair

- Furniture repair

- Jewelry repair

- Basic household item repair

- Bike repair

- Shoemaking and shoe repair

Key distinction: Note that auto repair services are specifically excluded from the microbusiness framework.

Agricultural Activities

Small-scale farming and agricultural production:

- Crop cultivation

- Animal husbandry

- Beekeeping

- Herb and flower growing

- Specialty crop production

- Seedling cultivation

- Small-scale organic farming

- Traditional agricultural practices

Key distinction: Focus must be on direct agricultural production rather than trading agricultural products.

Hospitality & Tourism

Selected hospitality and tourism services:

- Hostel services

- Tourist homes and guesthouses

- Bed and breakfast operations

- Small lodging facilities

- Tour guiding (direct service)

- Cultural experience hosting

- Rural tourism experiences

- Catering (outside Yerevan)

Key distinction: Public catering in Yerevan is excluded, with some exceptions for tourist facilities offering meals connected to accommodations.

Eligible Investment Activities

Despite the exclusion of financial services, certain investment activities may qualify:

- Stock portfolio holding (for dividend income)

- Capital gains activities

- Holding shares in other companies

- Managing personal investment holdings

Key distinction: While entities receiving rental income, interest, or royalties are excluded, companies receiving dividends or capital gains can potentially qualify for microbusiness status.

Activities Without Registration

Certain activities can qualify without formal business registration:

- Language teaching and tutoring

- Dance instruction

- Arts and music instruction

- Sports coaching

- Crafting and handmade goods

- Household and personal services

- Traditional skills instruction

- Cultural knowledge sharing

Key distinction: These activities allow individuals to qualify for microbusiness status without establishing a formal entity, though they still must register for the microbusiness certification.

Gray Areas and Qualification Considerations

When evaluating whether your business qualifies for Armenia's microbusiness status, you may encounter activities that fall into gray areas or require careful interpretation. Here are some important considerations to help navigate these nuances:

Content Creation vs. Marketing

The distinction between content creation (potentially eligible) and marketing services (explicitly excluded) can be subtle:

Likely Eligible

- Creating and selling your own blog content

- Producing and monetizing your own videos

- Writing and publishing your own books

- Creating and selling online courses

- Producing and selling stock photography

Likely Excluded

- Creating content for clients' marketing purposes

- Managing social media for other businesses

- Providing SEO or digital marketing services

- Creating advertising materials for clients

- Offering brand consulting services

Creation vs. Trade

The distinction between creating products (potentially eligible) and trading/reselling products (excluded) is crucial:

Likely Eligible

- Creating and selling handmade jewelry

- Producing and selling your own artwork

- Making and selling custom furniture

- Creating and selling your own digital products

- Growing and selling your own agricultural products

Likely Excluded

- Buying and reselling products

- Dropshipping businesses

- Operating an online store with others' products

- Importing and selling goods

- Acting as a distributor or retailer

Teaching vs. Consulting

The distinction between educational activities (potentially eligible) and consulting services (excluded) requires careful consideration:

Likely Eligible

- Teaching language skills to students

- Providing structured courses on specific topics

- Tutoring students in academic subjects

- Teaching artistic or musical skills

- Leading fitness or wellness classes

Likely Excluded

- Providing business strategy consulting

- Offering professional advice to organizations

- Performing business analysis services

- Advising on organizational development

- Providing expert opinions in a professional capacity

Digital Products vs. Software Development

The line between creating digital products (potentially eligible) and software development (excluded) can be particularly challenging:

Likely Eligible

- Creating digital art and illustrations

- Producing digital templates or printables

- Creating and selling digital educational resources

- Producing digital audio or music files

- Creating simple digital tools using existing platforms

Likely Excluded

- Custom software development for clients

- Mobile app development

- Website development services

- Programming and coding services

- Creating complex software products

Practical Application: Case Studies and Examples

To help illustrate how these eligibility distinctions apply in practice, let's examine several business scenarios and evaluate their qualification status:

Case Study: Online Course Creator

Business Model: Creating and selling online language courses to international students, generating approximately $48,000 annually.

Activities: Course creation, video production, material development, and direct teaching.

Qualification Status: Likely Eligible

Reasoning: This business focuses on educational content creation and direct teaching rather than consulting or professional services. The creator is producing and selling their own educational content, which falls outside the excluded categories.