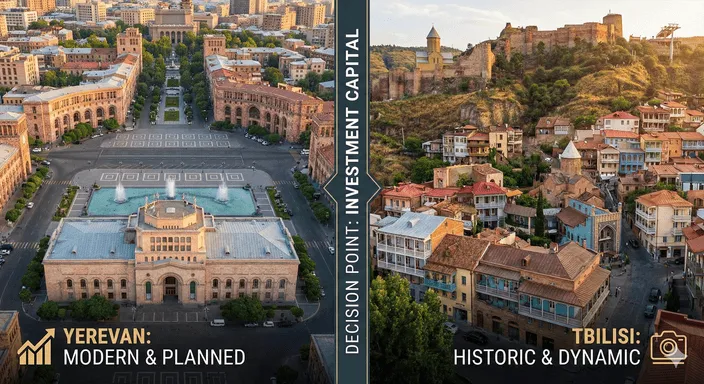

TL;DR

- Both cities now offer gross rental yields in the 6–9% range for typical investment apartments, with low transaction costs and no serious restrictions on foreign ownership.

- Tbilisi is better for hands-off income: slightly higher yields on small units, 5% rental tax, very low transaction costs, and a deeper, more liquid market.

- Yerevan is stronger for capital preservation: tighter, smaller market, AMD has appreciated ~25% vs USD since 2021, and 0% capital gains tax on most individual sales.

- Risks differ: Georgia has more political uncertainty after the "foreign agents" law and frozen EU track; Armenia carries geopolitical risk linked to its border situation with Azerbaijan.

- For many investors, the most resilient approach is: Tbilisi for yield and liquidity, Yerevan for long-term "safe haven" capital parking.

1. Big Picture: What Changed Since 2020?

From 2020 to 2025, the residential markets in both capitals went through the same "movie," but with different endings:

2020 – COVID + regional shocks:

Transactions slowed, construction paused, but neither market collapsed.

2021 – Recovery and cheap mortgages:

Both cities saw double-digit price growth as local buyers came back.

2022 – The game-changer: Russia–Ukraine war:

- Tens of thousands of new residents arrived in both Yerevan and Tbilisi.

- Rents jumped 50–100% in a single year in many districts.

- Sale prices surged; yields briefly hit double digits.

2023–2025 – Normalisation:

- New supply delivered, some migrants left or bought.

- Rents cooled, prices stabilised at a much higher plateau.

- Yields compressed but remain attractive by European standards.

By late 2025, both markets look less like speculative "spikes" and more like maturing investment destinations.

2. Snapshot 2025: Yerevan vs Tbilisi at a Glance

2.1 Key Market Metrics (Late 2025)

| Metric (late 2025) | Yerevan (Armenia) | Tbilisi (Georgia) |

|---|---|---|

| Central price / m² | $2,200–2,500 (Kentron) | $2,000–2,900 (Mtatsminda / Vake) |

| Non-central price / m² | $600–1,200 (outer districts) | $1,000–1,400 (Gldani, Didi Dighomi, Samgori) |

| Price change 2020–2025 | ~+70% central, ~+50% outer | ~+100% citywide (prices roughly doubled) |

| 1BR rent, central | $520–730 / month | $500–600 / month |

| 2BR rent, central | $655–915 / month | $650–850 / month |

| Gross yield, central | 5–7% | 5–7% |

| Gross yield, outer | 6–10% | 7–10% |

| Transaction costs (total) | ~3–5% | ~0.5–4% |

| Rental income tax | 10% flat | 5% flat (if registered) |

| Capital gains tax | 0% on individual-to-individual sales | 0% if held 2+ years |

| Property tax (annual) | Typically $50–200 on a $100k flat | Often $0 (income-based exemptions) |

| Foreign buyer share | ~3–4% of deals | 17%+ of deals |

| Annual transactions | ~25,000 (all property types) | ~40,000 residential in Tbilisi alone |

| Currency vs USD (5-year trend) | AMD +≈25% vs USD | GEL +≈10–15% vs USD |

Very short version:

- Prices: Roughly comparable in the centre, Yerevan cheaper in outer districts.

- Yields: Slight edge to Tbilisi, especially on smaller, cheaper units.

- Taxes & costs: Georgia wins (5% rental tax, near-zero property tax; Armenia 10% rental tax).

- Liquidity: Tbilisi is much deeper and faster.

- Currency & CGT: Yerevan offers the better currency story and cleaner 0% capital gains for individuals.

3. Yerevan: Compact, Scarce, and AMD-Boosted

3.1 Prices and Districts

Yerevan is a bowl-shaped city with an extremely tight centre:

Kentron (Center):

- 2020: around $1,300/m².

- 2022: jumped to about $2,100/m².

- 2025: $2,300–2,500/m² on average; elite projects can go far above.

- New monolith buildings trade at a strong premium to old stone/panel stock.

Arabkir: "Smart money" semi-central district.

- Around $1,600–1,800/m².

- Easier resale for units in the $80–150k range than ultra-prime Kentron.

Davtashen / Ajapnyak / Nor Nork:

- Typically $1,100–1,300/m².

- Benefited heavily from the government mortgage tax refund programme, now being phased out.

Budget districts (e.g. Nubarashen):

Around $580–600/m² – roughly ¼ of central prices.

Storyline: Yerevan's prices exploded in 2021–2022, especially in Kentron, then shifted to single-digit annual growth and small corrections in 2024–2025 as the market hit an affordability ceiling.

3.2 Rents and Yields

Rents in Yerevan doubled or more in 2022 and then partly corrected:

- Before 2022: central 1BR often AMD 150–180k (~$300–370).

- Peak 2022: many 1BRs at AMD 300–450k (~$700–$1,100).

- Late 2025: central 1BR typically $520–730, 2BR $655–915.

Typical gross yields:

- Kentron: 4.5–7% (capital-preservation segment; strong prices cap yields).

- Arabkir / Davtashen: 5–8% (sweet spot for many investors).

- Outer districts: 6–10% (on paper), but tenant quality and vacancy risk rise.

Short-term rentals (Airbnb etc.) in central Yerevan can push gross yields into the 8–12% range if managed well, but with significant seasonality and higher operational effort.

3.3 Taxes, Costs, and "Friction"

On the cost side, Armenia is still very investor-friendly:

Transaction costs:

- State registration ~$115.

- Notary + legal typically $700–2,500 combined.

- Buyer-side agent fee 0–2% (often negotiated).

- All-in: roughly 3–5% of purchase price.

Ongoing costs (for a $100k flat):

- Property tax: usually $80–150 per year today, rising gradually with market-value-based reform (full rates in 2026, still modest by global standards).

- HOA / building fees: maybe $500–1,200 per year in modern buildings.

- Rental management (if used): typically 8–20% of rent depending on service level.

Taxes on income and gains:

- Rental income: 10% flat on gross (20% above a high threshold).

- Capital gains: 0% when selling to another individual (typical exit scenario).

- 10% withholding if selling to a company / entrepreneur.

Foreigners can own apartments directly; land has some restrictions, but flats are straightforward.

3.4 Liquidity, Demand, and Risks

Liquidity:

- Around 25,000 transactions per year nationwide, a big share in Yerevan.

- Mid-priced units ($50–150k) in good districts are reasonably liquid; luxury can sit on the market longer.

Demand drivers:

- Large, wealthy diaspora; many pre-buy new projects.

- Strong IT and services sector in the capital.

- Russian relocations and later the influx from Nagorno-Karabakh.

- Tourism numbers hitting record highs, supporting short-term rentals.

Key risks:

- Security risk is mainly geopolitical (Azerbaijan border), not city-level. Yerevan itself has remained physically safe.

- Regulatory risk is modest: biggest change is the gradual shift to market-value property tax and tighter enforcement of rental income tax.

- Currency: AMD has appreciated strongly, which has been great for existing owners but makes new USD-based buyers pay more.

Bottom line on Yerevan:

- Strong case for capital preservation + moderate yield.

- Very compelling for those who value AMD strength, diaspora demand, and 0% capital gains more than ultra-high yields.

4. Tbilisi: High-Velocity, High-Liquidity, Tax-Efficient

4.1 Prices and Districts

Tbilisi is larger, more segmented, and heavily influenced by tourism and migration:

- Mtatsminda / Old Town: $2,400–2,900/m², historic buildings and tourist heart.

- Vake: $2,000–2,500/m²; embassy / elite area; "prestige" district.

- Saburtalo: $1,500–1,750/m²; metro access, lots of new builds; the "beta" of Tbilisi market.

- Gldani / Didi Dighomi / Samgori: Around $1,000–1,400/m²; mass-market zones with high volume.

Citywide average prices roughly doubled from around $600–650/m² in 2020 to about $1,200–1,250/m² by early 2025.

The new-build premium is clear: primary developer sales sit ~$1,320/m² vs $1,060–1,250/m² for older stock.

4.2 Rents and Yields

2022 saw rents explode (in some segments 100%+ YoY), then correct:

- Central 1BR pre-2022: often $300–450.

- Peak 2022: $600–900 not unusual.

Late 2025:

- Central 1BR: $500–600.

- Central 2BR: $650–850.

- Non-central 1BR: $350–450.

- Non-central 2BR: $400–550.

Yields by area:

- Didi Dighomi / Gldani / Isani: 7–10% gross (cheap entry, solid local demand).

- Saburtalo: 6–7% gross.

- Vake / Mtatsminda: 5–6% gross (premium price, lifestyle focus).

Short-term rentals in Old Town / tourist belts can deliver 12–18% gross with strong occupancy, but this is more of a business than a passive investment.

4.3 Taxes, Costs, and "Friction"

Georgia is almost textbook "frictionless" for property investors:

Transaction costs:

- Registration: roughly $20–75 depending on speed.

- Notary (if used): $40–75.

- Legal: typically $200–1,000.

- Buyer agency fee: 0–3%, often effectively paid by the developer/seller.

- No transfer tax, no stamp duty.

- All-in: 0.5–4% of price in most cases.

Ongoing costs:

- Property tax: often 0 for non-residents and lower-income owners.

- Condo fees: roughly $130–450 per year for typical flats.

- Management: 10–25% of rent (higher for full Airbnb service).

Tax regime for individuals:

- Rental income: 5% flat on gross if you opt into the simplified regime.

- Capital gains: 0% if held more than 2 years; 5% if sold earlier.

- Territorial system: only Georgian-source income is taxed.

Foreigners can buy apartments directly; agricultural land is restricted, but residential property is open.

4.4 Liquidity, Demand, and Risks

Liquidity:

- About 40,000 residential transactions per year in Tbilisi alone.

- That's roughly 3,000+ deals a month, making it one of the most liquid mid-size markets in the region.

Demand drivers:

- 7m+ tourists annually (pre- and post-COVID trend).

- Strong digital nomad, expat, and student community.

- Ongoing Russian, Ukrainian, Belarusian presence.

- Growing local middle class with access to mortgages.

- High participation from foreign buyers (~17%+ of transactions).

Key risks:

- Political: the "foreign agent" law, EU accession suspension, and high-profile protests created real uncertainty about long-term political orientation.

- Currency: GEL has moved between 3.4 and 2.5 per USD in recent years; volatility remains a factor.

- Oversupply risk: construction pipeline is large; some districts could see pressure if demand slows.

Bottom line on Tbilisi:

- Excellent for income-seeking investors and those who prize speed, liquidity, and simple tax rules.

- The trade-off is higher political noise and potential regulatory shifts over time.

5. Which City Fits Which Investor Profile?

5.1 Investor Personas

| Investor Profile | Better Fit | Why |

|---|---|---|

| Passive income, 5–10 year hold | Tbilisi | Higher typical yields, 5% tax, deep rental pool |

| Short-term rental / Airbnb-driven strategy | Tbilisi | Stronger tourism, more mature STR ecosystem |

| Long-term capital appreciation & FX hedge | Yerevan | AMD strength, 0% CGT, scarcity in the centre |

| Ultra-conservative, low political tolerance | Leaning Yerevan | Georgia's political path more uncertain at the moment |

| Maximum liquidity / fast exit options | Tbilisi | Larger, more international buyer base |

| Diaspora / emotional connection to Armenia | Yerevan | Lifestyle and identity factors may outweigh pure financial metrics |

| Diversification within one region | Both | Split: Yerevan for "club-like" core, Tbilisi for scalable yield |

5.2 Income vs Appreciation: A Simple Illustration

Imagine the same $100,000 invested in each city in a typical rental flat:

Tbilisi

- Gross yield: say 7.5% → $7,500/year rent.

- After 5% tax → $7,125 net (before costs).

Yerevan

- Gross yield: say 7% → $7,000/year rent.

- After 10% tax → $6,300 net (before costs).

The annual difference (~$825 in this simplified example) compounds over time in favour of Tbilisi.

On the other hand, if over 5–10 years AMD outperforms GEL and USD and core Yerevan continues to re-rate, your total capital gain (price + FX) could be higher in Yerevan even with slightly lower net yields.

6. Operational Reality for Non-Resident Owners

Both cities are workable for remote investors, but the "feel" is different.

Banking & Payments

Tbilisi:

- Very slick digital banking; opening a multi-currency account is usually straightforward.

- No capital controls; easy to move funds in and out.

Yerevan:

- Also open, but procedures can feel slightly more "manual".

- E-banking works well once set up; FX is easy and AMD accounts are standard.

Property Management

Tbilisi:

- Several English-speaking firms offering full-service management (long-term and Airbnb).

- "Turnkey investor packages" are common.

Yerevan:

- Management ecosystem is growing from a smaller base.

- Good managers exist, but you'll typically rely more on personal relationships and recommendations.

Legal & Compliance

Both cities: property registration is fast and digital; title systems are centralised and reliable.

Georgia's taxation and filing for rental income are extremely simple; Armenia's are still straightforward, but with a few more moving parts (property tax reform, rental enforcement, etc.).

7. Practical Takeaways and How to Use This Comparison

If you're considering the region for the first time, here's a simple decision tree:

Your #1 priority is cash flow and simplicity.

→ Start with Tbilisi, in mid-market or budget districts (Saburtalo, Didi Dighomi, Gldani, Isani), and use a professional manager.

You care more about preserving and compounding capital in a scarce, "club-like" market.

→ Focus on Yerevan, especially Kentron and Arabkir, and think in 10+ year horizons, not 2–3.

You want diversification across political and currency risk within one region.

→ Split your capital: one unit in Yerevan, one or two in Tbilisi. You'll be exposed to different demand drivers and risk factors.

You have a personal or business connection to Armenia.

→ The "soft" factors (language, community, sense of home base) arguably matter more than a 0.5–1% yield difference; in that case, Yerevan is the natural anchor.

8. A Note on Professional Advice

This overview is designed to give foreign investors a solid, data-based starting point. It can help you narrow down:

- Which city aligns with your risk/return profile.

- Which districts and strategies (long-term vs short-term rent) make sense.

- What ballpark numbers to expect on prices, rents, and taxes.

However, property, tax, and residency rules are still local law questions, and the best results come when your real-estate decisions fit coherently with your wider legal and immigration planning.

If you would like tailored advice on structuring an investment or combining a property purchase with residency or business setup in Armenia (and potentially the wider region), our team at Vardanyan & Partners can assist.

Contact Us