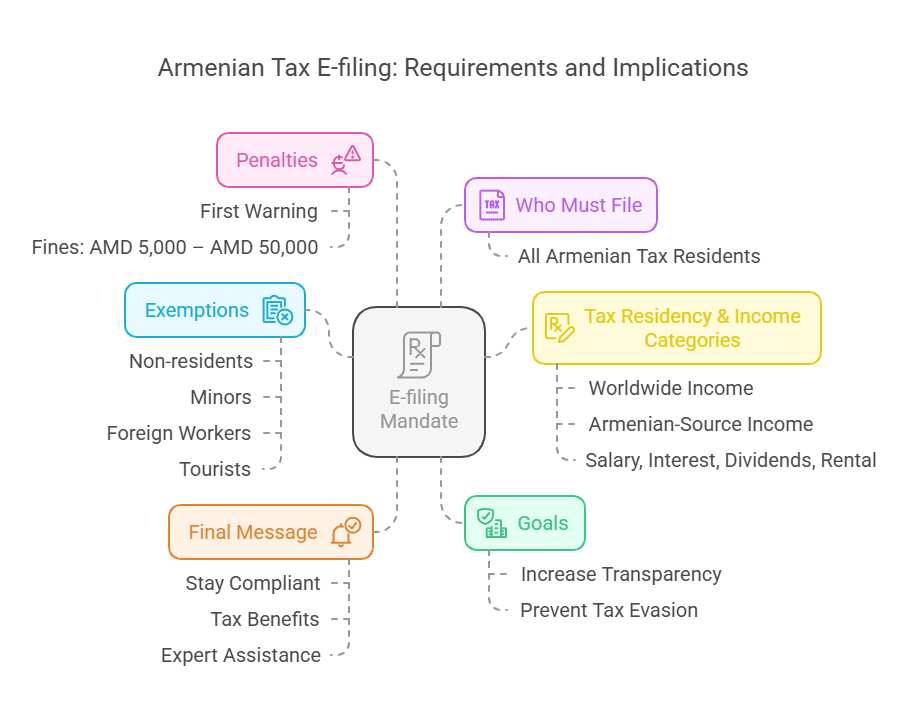

The Republic of Armenia, has recently overhauled its individual tax return filing system, moving to a mandatory electronic filing of personal income tax returns for most citizens. This change is part of a broader “universal income declaration” reform aimed at improving tax compliance and transparency. Below is an in-depth look at the current individual taxation framework in Armenia, the recent shift to e-filing, instructions on how to file electronically, and the implications for taxpayers.

Overview of Individual Taxation in Armenia

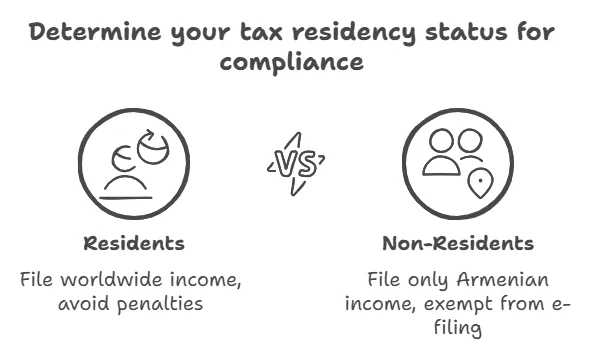

Tax Residency and Scope: Under Armenian tax law, residents (those living in Armenia ≥183 days a year or having center of vital interests in Armenia) are taxed on their worldwide income, whereas non-residents are taxed only on their Armenian-source income. The tax year is the calendar year.

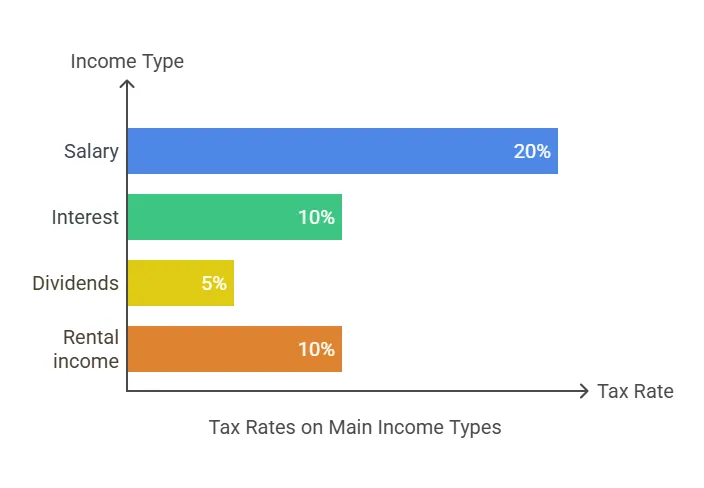

Income Tax Rates: Armenia employs a largely flat income tax system for individuals. As of recent years, the standard personal income tax rate on most employment and self-employment income paid is a flat 20%. This flat rate resulted from a phased reduction of the tax rate (from 23% in 2020 down to 20% by 2023), simplifying the tax regime. Key tax rates and taxable income types include:

-

Employment and Business Income: Generally taxed at a flat 20% rate (with tax typically withheld by employers at source).

-

Interest Income: 10% (if not exempt under specific conditions).

-

Royalties: 10% (final tax, often withheld at source by the payer).

-

Rental Income: 10% on rental receipts. (Note: If an individual’s rental income exceeds AMD 60 million in a year, an additional 10% tax applies on the amount above that threshold, effectively bringing the rate on the excess to 20%).

-

Capital Gains and Property Sales: Taxed at 0% to 20% depending on the asset and circumstances. For example, gains from sale of property to another individual can be exempt, but certain sales (or sales to organizations) may incur 10%–20% tax.

-

Dividends: Typically taxed at 5% for both Armenian citizens and foreign investors.

Armenia adheres to the worldwide income principle for residents, providing mechanisms to avoid double taxation through international treaties.

Residents vs. Non-Residents: While residents must report all global income, non-resident individuals are only taxed on income earned within Armenia’s borders. Employers in Armenia withhold tax from salaries of both residents and non-residents at the flat rate. Traditionally, most Armenian employees did not have to file annual tax returns at all – their tax was fully settled via employer withholdings. Only individuals with untaxed income (e.g. independent contractors, landlords, or others with income not subject to withholding) needed to file yearly returns (usually by April 20 of the following year). This long-standing system has now been upended by the new universal declaration mandate. Individuals receiving any kind of taxable income, referred to as income subject to tax, are required to file a return.

Certain categories of residents who hold significant shares in a legal entity or exercise control over it are affected by specific tax regulations starting in 2023.

Individuals must report all types of income, including any additional income that may not be tied directly to employment, such as income from civil contracts or rental properties, referred to as other taxable income.

Various forms of earnings such as dividends, interest, and royalties fall under the category of passive income, which are subject to specific tax rates and regulations.

Recent Changes in Tax Law and Return Filing

Universal Income Declaration: In late 2022, the Armenian government approved amendments to the Tax Code to introduce a “universal income declaration” system for individuals. This reform expands the requirement to file tax returns to virtually all Armenian resident citizens, implemented in stages over 2023–2025. Previously, only certain groups (like entrepreneurs or those with non-withheld income) filed returns, but under the new system most citizens must declare their annual income, even if all taxes were already paid through withholding. The goal is to capture all income (including passive and non-taxable income) in a declaration to identify any unregistered earnings, combat tax evasion, and enhance transparency in personal finances.

Phased Rollout (2023–2025): The mandate is being rolled out in three phases:

-

Phase 1 (for 2023 income, filing in 2024): Initially, certain categories of individuals were required to file for the 2023 tax year. These included public officials, large shareholders, beneficial owners, and those with substantial loans. Specifically, as of end of 2023: officials in state or community service positions, residents who were shareholders/owners of companies with gross income ≥ AMD 1 billion in 2022, those identified as “beneficial owners” under anti-money-laundering laws, and anyone who received loans of AMD 20 million or more during 2023 were required to file a personal income declaration. The filing deadline for 2023 income was May 1, 2024. This marked the first time many individuals ever had to submit a tax return in Armenia. The state registration certificate issued confirms the registration of individuals or entities conducting business activities within the Republic of Armenia.

-

Phase 2 (for 2024 income, filing in 2025): The requirement broadened to cover the “vast majority of tax residents” of Armenia. In fact, all adult working Armenian citizens considered tax-resident (i.e. spent 183+ days in Armenia) are now generally required to file for 2024. This includes regular employees (anyone with a labor or services contract in 2024), freelancers with taxable civil-contract income, all the categories from Phase 1 (officials, large shareholders, etc.), and essentially most ordinary working citizens. Even those with no income during the year must file a “zero” declaration if they fall into the required categories (for instance, if they had filed the previous year). The original legal deadline was May 1, 2025. However, due to implementation challenges, the government announced an extension to November 1, 2025 for filing 2024 income declarations. This one-time extension was granted because many citizens lacked the newly issued ID cards necessary for the electronic filing system, causing backlogs in obtaining the required electronic signatures.

-

Phase 3 (2025 and beyond): By 2025, the “universal declaration” system will be fully in place, meaning all adult resident citizens of Armenia will be filing annual tax returns going forward. The expectation is that starting with income earned in 2025 (to be filed in 2026), the process will become routine. The standard deadline is slated to revert to May 1 of each year (post-2025), unless further changes are announced.

Mandatory Electronic Filing: A key aspect of the reform is that declarations must be filed electronically – paper submissions are no longer the norm. Personal income tax returns are required to be submitted through the Unified System of Electronic Services for Individuals (accessible via the self-service portal: https://self-portal.taxservice.am/). This web-based system (with a forthcoming mobile app) is available in Armenian, English, and Russian for user convenience. The Armenian government integrated this e-filing requirement into law alongside the declaration mandate, effectively making electronic submission compulsory for all who must declare. As a result, Armenian taxpayers had to adapt to using online tools (or seek assistance) to fulfill their new obligations.

How to File an Electronic Tax Return in Armenia

Filing an electronic tax return in Armenia involves a few preparatory steps and the use of the online portal. Here is a step-by-step guide to the e-filing process, including the platforms and documentation needed:

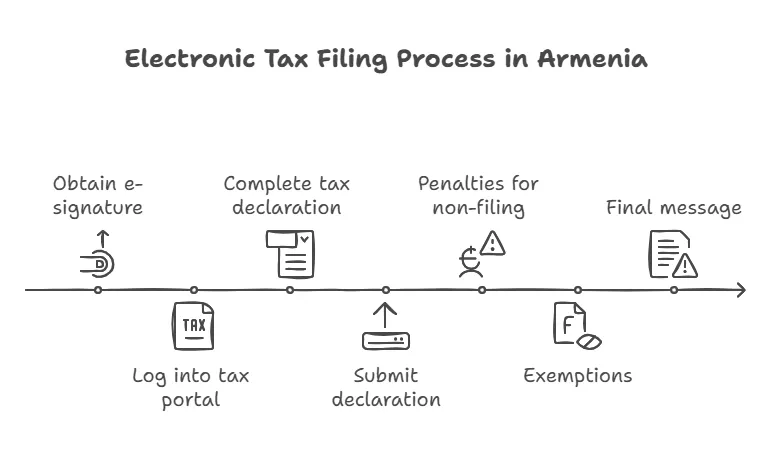

1. Obtain an Electronic Identification and Signature: To access the tax e-filing system, taxpayers must authenticate themselves with a secure electronic signature. There are several ways to obtain this digital ID credential:

-

ID Card (eID): Armenia’s citizen identification cards contain an electronic chip that can hold digital certificates. If you have a newer ID card (issued in recent years) and its PIN codes, you can use it for login. You’ll need a smart card reader to connect the ID card to your computer and activate the e-signature.

-

Mobile ID (mID): This is a convenient option using your mobile phone. It requires obtaining a special ID-SIM card from a local mobile operator (available at carrier service centers) and registering it with your identity documents. The ID-SIM, once activated with an e-signature service (often through the operator or online), allows you to sign in via your phone number – essentially turning your phone into an authentication token.

-

Cloud-Based Signature (e.g. “CoSign” service): Armenia also offers a cloud electronic signature service (sometimes referred to as CoSign). You can apply for a cloud signature through authorized providers like EKENG CJSC or at Passport and Migration Service offices. This method doesn’t require a physical card or SIM; instead, your digital certificate is stored securely online, and you log in with credentials and second-factor authentication to sign electronically.

Tax agents are responsible for withholding taxes from different types of income at the source and calculating the final tax amounts owed by taxpayers.

To get any of these, you typically apply at the Passport and Visa Department (Migration and Citizenship Service) of the Ministry of Internal Affairs or through EKENG (the government’s e-Governance Infrastructure provider). Once obtained, ensure your electronic ID/sig is active. (If you already have an active electronic ID and signature, no further action is needed on this step).

2. Access the Online Tax Portal: The next step is to enter the SRC’s online filing system for individuals. The platform can be reached in two ways:

-

Visit the State Revenue Committee’s official website (src.am). Navigate to the “Natural Person” or “Individual” section and look for the link to the annual income declaration system (often labeled “Annual Declaration for Individuals”).

-

Directly go to self-portal.taxservice.am, which is the Unified System of Electronic Services for Individuals.

Tax agents play a crucial role in the taxation system, particularly in relation to withholding tax on various types of income.

At the portal’s login page, you will be prompted to sign in via the “Yes Em” national identification system (branded as «Այո եմ» or “It’s me” in Armenian). Choose your login method (Mobile ID, ID card, or other available option) and follow the prompts to authenticate. For example, if using an ID card, you’ll insert it in the reader and enter your PIN; if using mobile-ID, you’ll confirm a code sent to your phone. The “Yes Em” system is essentially the unified login gateway for e-government services, and it will issue your Taxpayer Identification Number (TIN) if you don’t already have one during the registration process. New users can also obtain their TIN through this portal as part of first-time registration (the system will guide you to a “Get TIN” process if needed).

3. Complete and Submit the Tax Declaration: Once logged in, you will find your personal dashboard. The tax authority may have a pre-filled draft declaration for you, populated with information they have (e.g. your officially reported salary income, taxes withheld, etc.). Review the pre-filled data carefully. You will need to add any additional income that wasn’t pre-reported (for instance, freelance earnings, rental income, foreign income, large gifts or loans received, etc.), and you should include both taxable and certain non-taxable income as required by the rules. The system has fields and forms to enter various income types and allowed deductions. Follow the on-screen instructions to fill out all required sections of the “Personal income tax and social contribution calculation (declaration)” form. The interface is available in English, Armenian, and Russian, and will guide you step-by-step. Key pieces of information or documentation you may need at hand include: details of any self-employment or contract income (amounts earned), documents for any abroad income or taxes paid abroad (to claim credit if applicable), and receipts for certain expenses if you plan to claim allowable refunds (more on this below). After confirming that all information is correct and complete, you will submit the declaration electronically through the portal.

Upon successful submission, the system will usually provide a confirmation or reference number. Any tax due (for incomes not already taxed via withholding) should be paid by the same deadline – the portal will compute any balance owed. Conversely, if you have a refund due (for example, via the “social credit” for expenses), the system will record that and the SRC will process the reimbursement to your bank account after verification.

Key Dates: For the 2024 tax year (filed in 2025), the deadline is November 1, 2025 (extended from the usual May 1). In general, going forward the annual filing deadline is expected to be May 1 of the year following the income year (e.g. May 1, 2026 for 2025 income), unless otherwise announced. It’s advisable to file well before the deadline to avoid last-minute technical glitches and to give yourself time to resolve any login or submission issues (especially given the high volume of new users on the system).

Necessary Documentation: While the e-filing system is intended to be largely pre-populated, taxpayers should gather any relevant documents such as: evidence of any untaxed income earned (contracts, invoices, bank statements showing freelance or rental payments), proof of taxes paid abroad (if claiming foreign tax credit), and receipts for eligible expenses if they plan to utilize the government’s reimbursement (social credit) for expenses like education, healthcare, or mortgage interest (since those need to be reported to get the tax refund). Residents working for foreign companies should note the foreign income and tax paid, as they will declare that income and possibly pay the difference if the foreign tax was below Armenia’s rate. For most regular employees, the main “documentation” is already with the tax authorities (your employer’s payroll reports), so the process should be straightforward – you mainly need to verify the data and submit.

Impact on Taxpayers (Tax Residents and Non-Residents)

The shift to mandatory e-filing has significant impacts on taxpayers, both positive and challenging. Here we discuss the benefits, common challenges, and compliance issues for different groups:

Benefits and Opportunities:

-

Streamlined Tax Management: The new system creates a one-stop portal for individuals to handle tax matters. Taxpayers can now easily view their recorded income and withheld taxes in one place. This transparency allows individuals to double-check that their employers have properly reported their income and taxes.

-

Pre-Filled Data and Simplified Compliance: For those whose only income is salary from Armenian employers, the declaration is largely pre-filled by the SRC. Filing in such cases becomes a quick review-and-approve task online, meaning compliance is not burdensome in terms of calculation (it’s an extra administrative step, but not an extra tax burden).

-

Tax Refunds through “Social Credit”: A notable positive impact is the introduction of a social credit incentive program. Individuals who file declarations can get refunds (credits) on income tax for certain personal expenses. The government allows reclaiming some portion of costs paid for education or health insurance for the taxpayer or their family. For example, if you paid tuition fees or health insurance bills, a part of those expenses can be credited back to you as an income tax refund after you declare your income. By early 2025, authorities reported hundreds of citizens already receiving such refunds on their 2024 filings, totaling hundreds of millions of drams in reimbursements under the social credit program.

-

Fighting the Shadow Economy: From a societal perspective, the universal declaration aims to bring more incomes out of the shadow. Law-abiding taxpayers may benefit in the long run if overall compliance increases – it could lead to a more fair distribution of the tax burden and potentially better public services funded by improved revenue. The system also helps identify individuals’ true economic status, which the government can use to target social assistance or subsidies to those who genuinely need it (since they will have comprehensive data on everyone’s income).

-

Convenience of E-Filing: Electronic filing means taxpayers do not need to physically visit tax offices with paper forms. This is especially beneficial for citizens living in regions far from tax service offices or those abroad (if they still qualify as residents). The online system is accessible 24/7 from anywhere, and it supports three languages, making it user-friendly for many, including diaspora returnees who may prefer English or Russian interfaces. Over time, the availability of a mobile app (as hinted by SRC) will further improve convenience, enabling people to file via their smartphone.

Challenges and Adjustment Issues:

-

Initial Confusion and Technical Glitches: The rollout of the new system has been met with public confusion and some panic. Many citizens were unfamiliar with filing tax returns at all, leading to uncertainty about what needs to be declared and how. The process of obtaining an e-signature (ID cards, mobile IDs) created bottlenecks — with long waiting times to get new ID cards, as noted by the Prime Minister. Additionally, in early 2024, the SRC’s electronic portal experienced technical difficulties and downtime due to the unprecedented volume of users, causing frustration. These issues required deadline extensions and continuous public education efforts.

-

Digital Literacy and Access: Not all residents are equally tech-savvy. Elderly taxpayers or those in rural areas with limited internet access faced challenges using the online system. Although Armenia has a high rate of mobile phone usage, navigating an electronic form might be daunting for some. This has led to many people seeking help from tax consultants or tech-savvy relatives, especially in the first year of filing. The government has responded by setting up helpdesks and tutorials (including FAQs and even Instagram video guides) to assist citizens in the process.

-

Compliance Burden for Certain Income Types: Residents with multiple income sources (e.g. freelancers working for foreign clients, landlords, or those receiving remittances from abroad) now must carefully track and report all that income. Under the old system, some of this income might have gone unreported; now there’s a legal obligation to declare it. For example, an Armenian resident doing remote IT work for a foreign company must declare that income and may owe Armenian tax if the foreign-paid tax was below 20%. This creates a new compliance burden – they may need to calculate and pay additional tax, or at least file paperwork to claim foreign tax credits. Ensuring awareness of these rules (especially in the growing expat and digital nomad community in Armenia) is an ongoing challenge.

-

Non-Residents and Foreigners: One notable aspect is that non-citizens (foreign nationals) working or living in Armenia are not required to file under the new universal system. They continue to be taxed via withholding or under the previous rules. This distinction means foreign residents have a simpler process (no annual declaration), whereas Armenian citizens must file if they meet residency criteria. However, some foreigners may still choose to file if they have Armenian-source income not taxed at source. For Armenians in the diaspora, the law could be confusing: an Armenian citizen living abroad most of the year is exempt if they spend less than 183 days in Armenia. But if they frequently travel to Armenia or moved back in mid-year, they might inadvertently become “tax resident” and thus obligated to declare worldwide income. The 183-day rule is crucial for dual citizens and diaspora members to understand to stay in compliance or know if they qualify for an exemption.

In summary, the impacts on taxpayers range from greater empowerment and potential financial benefits (through easier refunds and a transparent record of one’s taxes) to growing pains in adapting to a digital tax compliance era. Over time, as familiarity increases and the system stabilizes, the hope is that annual e-filing will become a normal, straightforward aspect of personal finance for Armenian residents.

Exemptions and Penalties for Tax Agents under the E-Filing Mandate

Who Is Exempt from Filing? The universal filing requirement applies broadly, but there are specific exemptions. You are not required to file an annual income declaration if you fall into any of these categories:

-

Non-Resident Citizens: Armenian citizens who spend less than 183 days in Armenia during the tax year are not considered tax residents, and thus are exempt from filing for that year. For example, an Armenian citizen living abroad who visits the country only briefly does not need to declare income in Armenia.

-

Tourists and Special Status Residents: Foreign citizens visiting Armenia (tourists) or those who hold a special 5-year or 10-year residency passport (often a status granted to members of the Armenian diaspora or certain investors) are generally exempt. Their income from Armenian sources, if any, is typically handled via withholding or other mechanisms, and they have no declaration duty.

-

Non-Citizens Working in Armenia: If you are not an Armenian citizen (regardless of days spent in country), you are not subject to the new universal declaration system. (Such individuals may still pay Armenian tax on local income via payroll or file under old rules if necessary, but they are outside the citizen-based mandate.)

-

Minors: Individuals who were under 18 years of age as of the end of the tax year do not need to file a declaration.

-

Individual Entrepreneurs (IEs) and Sole Proprietors: This category is a bit nuanced. Registered entrepreneurs (sole proprietors) in Armenia already file separate tax reports for their business activities. The SRC has clarified that if an individual is registered as an “Individual Entrepreneur” and all their income is from their business which they report separately, they do not need to include that in the personal income declaration. In fact, IEs are not required to file the new declaration for their business income. But if they have other income as well (like a side job as an employee, or any of the categories that require declaration), then they must file for those incomes. In short, business owners don’t double-declare their business earnings, but they must declare other personal income outside the business.

It’s important to note that being exempt from the filing requirement doesn’t exempt one from paying any due taxes. For instance, a non-resident still pays applicable Armenian tax on local income (through withholding or by separate return if needed), but they are exempt from the annual declaration formality. The above categories are essentially carve-outs to narrow the scope to “resident citizens” – i.e., the policy’s focus is on citizens of Armenia who principally live in Armenia.

Penalties for Non-Compliance: To enforce the new rules, the government has put in place a penalty regime, though it starts gently to allow people to adjust. Here’s how it works if a person fails to file by the deadline:

-

For a first-time miss, the individual will typically receive an official warning. The SRC will notify the taxpayer that they have not submitted their declaration and give them a short window (e.g. 30 days) to remedy the situation.

-

If the person does not file even after the warning period (30 days), then a monetary fine is imposed. The fine amounts are differentiated by the category of taxpayer:

-

Ordinary individuals face a fine of AMD 5,000 (approximately $10–$15) for failure to file.

-

Those who are major participants in companies (e.g. shareholders or partners of large firms with gross income over ~AMD 1 billion) face a higher fine of AMD 50,000 (around $120–$130), reflecting the greater responsibility expected from those in significant financial positions.

-

-

Continued non-compliance or repeated violations in subsequent years could lead to higher fines or other administrative sanctions under the Code of Administrative Offenses, which was amended to include penalties for the declaration system. In extreme cases, willful failure to file combined with tax evasion could potentially lead to legal liability, but for most individuals the immediate risk is the administrative fine.

It’s worth emphasizing that the government’s approach initially is more carrot-and-stick combined with leniency: the first year (2023 filing in 2024) saw mostly warnings and an educational approach. The Prime Minister and SRC have indicated understanding that people need time to obtain IDs and get used to the system, which is why deadlines were extended and first offenses are only warned. However, as the system matures, taxpayers are expected to comply annually. To avoid penalties, individuals should mark their calendars for the annual deadline and file on time, even if they have no income to report (in which case filing a zero-income declaration is required if they are in the mandated group).

Armenia’s mandate for electronic filing of individual tax returns represents a major shift towards digitization and transparency in tax administration. While it presents short-term challenges for taxpayers adapting to new requirements, it lays a foundation for a more comprehensive and modern tax system. The government’s rationale centers on fairness and efficiency – bringing all citizens into the tax net, leveraging technology for easier compliance, and rewarding good behavior with tax credits.

Frequently Asked Questions (FAQs)

-

Who is required to file an income tax return under Armenia’s new system?

Nearly all Armenian tax residents, including employees, must file annual tax returns, even if taxes have been withheld at the source. -

What is the deadline for filing my tax return?

For income earned in 2024, the filing deadline is November 1, 2025 (extended from the usual May 1). Starting from 2026, the standard deadline will revert to May 1 each year. -

How do I obtain an electronic signature to file my tax return?

You can use Armenia’s ID card (eID), Mobile ID (mID), or cloud-based signature services to authenticate your identity for e-filing. These can be obtained through EKENG or passport service centers. -

What happens if I fail to file my tax return?

First-time non-compliance typically results in a warning. Repeated failure may lead to fines of AMD 5,000 for individuals and AMD 50,000 for major shareholders. -

Are non-residents required to file a tax return?

No, non-residents (including Armenian citizens who spend less than 183 days in Armenia) are exempt from the universal declaration mandate.

Need guidance on Armenia’s new tax filing system? Our legal experts at Vardanyan & Partners are here to help you navigate electronic tax returns and ensure compliance. Contact us today for personalized assistance!