High-net-worth individuals, entrepreneurs, digital nomads, and corporate investors are increasingly looking to low-tax countries in Eastern Europe as potential bases for residency or business, with corporate income tax rates playing a crucial role in these decisions. Among these, Bulgaria, Latvia, and Armenia stand out for their business-friendly tax regimes and investment incentives. This article provides a deeply researched comparison of the tax environments in Bulgaria, Latvia, and Armenia – covering personal and corporate tax rates, residency and citizenship options, special tax incentives, ease of doing business, and the regulatory/legal landscape.

| Criteria | Bulgaria | Latvia | Armenia |

|---|---|---|---|

| Personal Income Tax Rate | Flat 10% | Progressive 25%/33% (36% top rate with surcharge) | Flat 20% |

| Corporate Tax Rate | Flat 10% | 20% (only on distributed profits) | Flat 18% |

| Tax on Retained Earnings | Taxed annually | 0% – retained earnings untaxed | Taxed annually |

| Dividend Withholding Tax | 5% (final tax) | 0% if CIT paid; high earners may owe extra 3% | 5% |

| Residency by Investment | Yes – From ~€307,000 in real estate or €512,000 in funds | Yes – From €50,000 business or €250,000 real estate | Yes – Via any business (low threshold) |

| Digital Nomad Visa | No specific nomad visa, but flexible D visa | Yes – For OECD nationals, valid up to 2 years | No specific nomad visa, but visa-free + TRP options |

| Startup Tax Incentives | Limited – R&D expensing, regional CIT relief | Yes – Payroll tax cap, stock options tax-free | Yes – special regimes for IT sector |

| Microbusiness Regime | No formal regime, but low thresholds and flat tax help | No micro regime, but simplified schemes for SMEs | Yes – 0% for micro-entrepreneurs < AMD 24M/year |

| Free Economic Zones | Yes – customs/VAT benefits in zones | Yes – SEZs and Free Ports, up to 80% tax reduction | Yes – 0% CIT/VAT/customs/property tax |

| Ease of Doing Business (WB 2020) | 61st | 19th | 47th |

| EU Membership | Yes | Yes | No |

| Dual Citizenship Allowed | Yes | No | Yes |

| Corruption Perceptions Index | 43/100 | 59/100 | 46/100 |

| Legal System Transparency | Moderate, EU-aligned, some inefficiencies | High, digital-first, OECD-aligned | Improving post-2018, investor friendly |

| Banking & Compliance Openness | Stable, requires in-person steps for foreigners | Highly regulated, strict KYC in banks | Open, flexible with diaspora-friendly banks |

Personal Income Tax Rates and Structure

Personal income tax (PIT) affects individual investors, remote workers, and anyone drawing a salary or business income in these countries. The three jurisdictions take distinctly different approaches: Bulgaria and Armenia levy flat income tax rates (regardless of income level), whereas Latvia uses a progressive two-tier system with an additional surcharge on very high incomes. Different levels of annual incomes are taxed differently in each country.

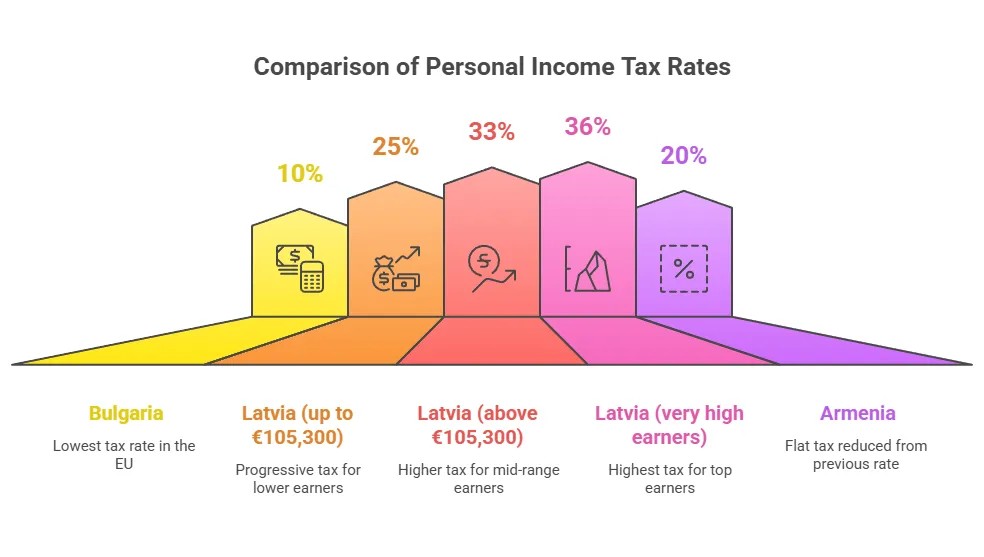

Bulgaria: Flat 10% Personal Tax – Lowest in the EU

Bulgaria has a simple, flat 10% personal income tax rate on taxable income. This flat tax applies to virtually all types of personal income (employment, business, etc.), making Bulgaria’s PIT one of the lowest in Europe. There are only minor exceptions (certain capital gains or dividends may be taxed at different final rates), but for most taxpayers – including salaried employees, self-employed entrepreneurs, or freelancers – the rate is a straight 10%. The simplicity of Bulgaria’s income taxes makes it an attractive option for individuals seeking straightforward tax obligations.

Such a low flat tax means that a high-earning individual pays the same proportion of tax as someone with lower income. For example, an entrepreneur earning €200,000 in Bulgaria would owe around €20,000 in income tax (10%), whereas in many Western European countries the top bracket could exceed 40-50%. Indeed, Bulgaria (10%) and Romania (10%) levy the lowest personal tax rates in Europe. This flat regime is very attractive for expatriates or digital nomads who establish Bulgarian tax residency to minimize their income tax.

It’s worth noting that social security contributions are separate from PIT. In Bulgaria, employers and employees must contribute to social insurance (around 32.7% combined on salaries, capped at a maximum income). Even with these contributions, the overall tax burden on high incomes remains modest compared to high-tax jurisdictions. Bulgarian tax residents are taxed on their worldwide income, but non-residents pay Bulgarian tax only on Bulgarian-source income. Becoming a tax resident generally requires spending >183 days/year in Bulgaria or having center of vital interests there.

Latvia: Progressive Tax up to ~33% (36% for Top Earners)

Latvia employs a progressive personal income tax system with two main brackets plus a high-income surcharge. Annual income up to €105,300 is taxed at 25%, and any income above €105,300 is taxed at 33%. In addition, if an individual’s total income exceeds €200,000 in a year, an extra 3% solidarity tax applies on the portion above €200k. This effectively brings the top marginal rate to 36% for ultra-high earners. For example, a Latvian resident earning €250,000 would pay 25% on the first €105,300, 33% on the next portion up to €200k, and 36% on the amount above €200k.

While Latvia’s rates are higher than Bulgaria’s flat tax, they are still moderate by EU standards – the average top EU rate is ~43%. Latvia recently increased its top rate from 31% to ~36% to raise revenue from high incomes. There are personal allowances and deductions that can reduce taxable income (e.g. allowances for dependents or pension contributions), but the core structure remains two-tiered. Dividend income in Latvia is generally taxed at 25% (if not already taxed at corporate level), but notably dividends distributed from profits that have been taxed at the corporate level are exempt from further PIT. This integration rule means if you own shares in a Latvian or EU company that paid corporate tax on its profits, you won’t be double-taxed on the dividend (except that the 3% surcharge still applies for high incomes). Capital gains and other investment income are usually taxed at 20–25% (often as “capital income” at 20% or as part of overall income).

For foreign professionals and remote workers, Latvia’s personal taxes may be higher than Bulgaria’s, but quality of life and services (funded by those taxes) might be a trade-off. Some relief exists: for example, Latvia does not tax foreign-source income of non-residents, and tax residents can get credits for foreign taxes paid. Overall, tax residency in Latvia means worldwide income is taxable, so high-net-worth individuals often plan carefully – perhaps keeping investment income in corporate structures to take advantage of Latvia’s corporate tax deferral (discussed below).

Armenia: Flat 20% Personal Tax (Reduced from 23% in Recent Reforms)

Armenia has recently transitioned to a flat personal income tax of 20% on almost all types of income. This flat rate was introduced as part of sweeping tax reforms: from 2018 to 2023, Armenia gradually lowered the PIT rate from 23% down to 20% to improve competitiveness. As of 2024, an Armenian tax resident pays 20% on salary, self-employment, and other personal income, regardless of amount. There are no tax brackets, which simplifies tax calculation significantly. For instance, whether you earn AMD 5 million or AMD 500 million in a year, the income tax rate remains 20%.

Armenia’s flat 20% is higher than Bulgaria’s 10% but still relatively low globally – and notably lower than many EU countries’ rates (the flat rate is on par with Georgia’s 20%). The flat tax, combined with a low cost of living, has made Armenia increasingly attractive to expatriates and remote professionals in recent years. Moreover, certain types of income have even lower rates: for example, interest income and royalties can be taxed at 10% final withholding, and dividends paid to individuals can be taxed at 5%.

It’s important to note Armenia doesn’t have a broad range of deductions or allowances – the flat tax is largely applied without a personal allowance (income is taxed from the first dram earned). However, Armenia offers special tax regimes for micro-entrepreneurs and IT workers that effectively reduce personal tax (discussed under incentives). In summary, an individual establishing tax residency in Armenia (generally 183+ days presence or Armenian citizenship) will face a straightforward 20% tax on worldwide income, with potential reductions if they qualify for specific programs. The simplicity and certainty of this flat rate is a selling point for investors who prefer predictable tax obligations.

Corporate Tax Rates and Structures

For corporate investors and entrepreneurs, the corporate income tax (CIT) regime of a country is crucial, as corporate taxes significantly influence business decisions. All three countries offer low or unique corporate tax systems designed to attract businesses. Below we compare how Bulgaria, Latvia, and Armenia tax corporate profits in 2024/2025, and what that means for companies and their owners:

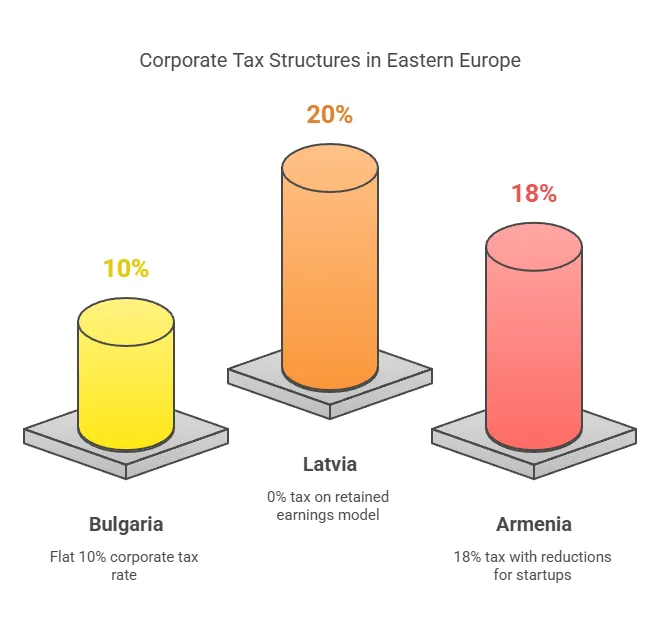

Bulgaria: 10% Flat Corporate Tax on Profits

Bulgaria imposes a flat corporate income tax of 10% on net profits of companies. This rate has been steady for years and is one of the lowest statutory CIT rates in the EU (only Hungary, at 9%, is slightly lower). Compared to other countries in the world, Bulgaria’s tax rate is highly competitive, making it an attractive destination for businesses. The 10% tax applies to all Bulgarian companies and local branches on their taxable profits, with no progressive tiers. In practice, a Bulgarian LLC or JSC will calculate its profit (revenues minus deductible expenses) and then pay 10% of that to the government. For example, if a company’s profit in Bulgaria is €1,000,000, the corporate tax due is €100,000. By comparison, the European average CIT rate is around 21.3% – more than double Bulgaria’s rate – highlighting Bulgaria’s appeal as a low-tax jurisdiction in Eastern Europe.

Despite the low rate, Bulgaria’s tax base rules are fairly standard (similar to other EU countries). All undistributed profits are still subject to the 10% tax annually – there is no deferral or exemption for retained earnings. This means even if a Bulgarian company reinvests its profit into the business, it still pays 10% CIT for that year, unlike the situation in Latvia (discussed next). On the other hand, dividends paid to individuals from a Bulgarian company are typically subject to a 5% withholding tax (which is a final tax on that income). Combined with the corporate tax, the effective tax on distributed corporate earnings to a Bulgarian resident individual comes to about 14.5%. However, Bulgaria has no withholding tax on dividends paid to EU resident companies, due to the EU Parent-Subsidiary Directive, making it attractive for international holding structures.

Bulgaria’s straightforward 10% CIT, along with EU membership guarantees (e.g. access to EU’s network of tax treaties and EU Directives), provides certainty for corporate investors. Notably, Bulgaria has adopted the OECD’s global 15% minimum tax (Pillar 2) as of 1 January 2024, but this affects only large multinational groups – the standard 10% rate remains for local businesses. In summary, for a typical entrepreneur or a company setting up operations, Bulgaria offers a very low flat corporate tax with a conventional taxation model (profits taxed yearly). This is ideal for companies that generate profits and distribute them regularly, as the combined tax burden stays low.

Latvia: 0% Tax on Retained Earnings, 20% on Distributed Profits (Estonia-Model CIT)

Latvia’s corporate tax system is uniquely designed to encourage reinvestment and reduce tax burdens for businesses. Since 2018, Latvia adopted an “only taxed upon distribution” model of CIT (often called the Estonia model). All undistributed corporate profits are exempt from tax – meaning if a Latvian company reinvests or simply retains its earnings, it pays 0% CIT on those profits indefinitely. Corporate income tax of 20% is only triggered when profits are distributed or deemed distributed (for example, paid out as dividends to shareholders, or used for non-business expenses).

The 20% rate is applied in a particular way: the taxable base is the grossed-up amount of the distribution. In practical terms, if a company wants to pay a dividend of €80 (net to shareholder), it must pay €20 tax, which is 20/80 = 25% of the net dividend. But the convention is to quote the rate as 20% of the gross profit (100 in this example). Effectively, €100 of profit distributed results in €20 tax and €80 to the shareholder. If the company distributes nothing, no corporate tax is due for that year. This system offers a form of tax deferral – companies can reinvest earnings tax-free until they decide to pay dividends.

From an investor’s perspective, Latvia’s CIT regime is extremely advantageous for growth companies and holding companies. A startup can plow back its earnings to expand without a tax drag, and a holding company in Latvia can receive dividends from subsidiaries and not pay tax until it passes them on to its owners. Moreover, Latvia operates a territorial principle for foreign dividends and income: foreign-source dividends received by a Latvian company (from non-tax haven jurisdictions) are often exempt from tax, and since Latvia’s own distributions are taxed as CIT (not as a withholding tax), treaty benefits usually don’t reduce that tax. Essentially, the 20% is a final tax at the corporate level for profit distributions, and no additional dividend tax is imposed on individuals if the company has paid that 20%. One exception: very high-earning individuals may still owe the 3% solidarity PIT on large dividends, as noted earlier.

It’s also noteworthy that Latvia abolished the traditional concept of taxation on annual profit – if a company earns profit but retains it, that profit isn’t reported for CIT that year. This can simplify accounting for tax purposes (though for financial accounting, profit is still calculated normally). The effective corporate tax rate on distributed profits is 20% (or 25% of net, as explained), which is still competitive regionally (and equal to Estonia’s rate). Additionally, Latvia offers special reduced CIT rates (as low as 3%–14%) in certain cases such as relief for companies in Special Economic Zones or for qualifying small distributions (discussed under incentives). In summary, Latvia’s corporate tax system is one of the most business-friendly in Europe, allowing entrepreneurs to build up their companies tax-free until they choose to take profits out. This contributes greatly to Latvia being ranked the 2nd most competitive tax system in the world in 2023.

Armenia: 18% Standard Corporate Tax (with Special Small Business Regimes)

Armenia levies a standard corporate profit tax of 18% on company earnings. This flat rate (sometimes cited as “profit tax”) was reduced from 20% in 2020 as part of Armenia’s economic reforms to stimulate investment. For most medium and large companies, the 18% rate applies to taxable profits annually – a traditional tax system more akin to Bulgaria’s (i.e., profits are taxed in the year they are earned). For example, a firm earning AMD 100 million in profit (~€240,000) would owe 18% (AMD 18 million) in profit tax. Armenia’s 18% rate is moderate by international standards (lower than the global average ~23% and the OECD average ~21-22%). Although Armenia is not in the EU, its rate is comparable to many European countries (for instance, Poland 19%, Lithuania 15%, Czech Republic 19%). Armenia does not impose an inheritance tax, which can be a significant consideration for individuals and families planning their estate.

What differentiates Armenia is the array of special tax regimes for small businesses and startups. Armenia has a “micro-business” regime and a “turnover tax” regime that effectively serve as simplified alternatives to the standard 18% CIT + 20% VAT system. Micro-enterprises (small businesses with under AMD 24 million turnover, approx €55,000) are exempt from all taxes except a small fixed amount per employee. Specifically, registered micro businesses pay 0% profit tax, 0% VAT. This is a significant incentive for solo entrepreneurs, consultants, or small startups – effectively a tax holiday up to a certain revenue threshold. Next, for slightly larger small businesses, Armenia’s “turnover tax” is a simplified tax on gross revenues (10%, with some reductions) that replaces VAT and profit tax for businesses under ~AMD 115 million turnover. This can result in a lower effective tax than 18% on profit if profit margins are high, and it greatly simplifies compliance.

For regular corporations outside these small-business regimes, the 18% tax is accompanied by 5% withholding tax on dividends. Armenia also provides tax holidays or exemptions in certain industries and regions – for instance, companies operating in Free Economic Zones pay 0% profit tax, 0% VAT, and enjoy customs and property tax exemptions. Additionally, since 2015 Armenia has offered IT startup tax incentives, granting certified tech startups a 0% corporate tax rate for a set period and only 10% income tax on their employees’ salaries (instead of 20%). These IT incentives were recently extended and enhanced: from 2025, qualifying high-tech companies can get a turnover tax rate of 1% (instead of 18% profit tax) and a 10% personal tax on R&D-related wages. Effectively, a young software company in Armenia could operate almost tax-free in its early years.

In summary, Armenia’s headline corporate tax is 18%, but many businesses, especially smaller or strategic ones, can benefit from significantly reduced effective rates through special regimes. Unlike Latvia, there is no across-the-board deferral of tax on retained earnings – profits are taxed each year – but Armenia’s targeted incentives (zero-tax micro firms, IT sector relief, etc.) can result in zero or minimal tax for those who qualify. For larger investors, the 18% rate combined with relatively inexpensive operations can still be attractive, and export-oriented companies enjoy VAT refunds and no export duties, keeping the tax burden on international business low.

Comparative Note: For a corporate group or entrepreneur deciding between these countries, the choice may depend on business model. If one plans to reinvest profits heavily, Latvia’s 0% on retained earnings is extremely appealing. If one wants the absolute lowest statutory rate and simplicity, Bulgaria’s 10% CIT is hard to beat. If one is building a small startup (especially in tech) or seeking a mix of moderate tax and special exemptions, Armenia’s regime might yield the lowest tax bill (potentially 0% under certain programs).

Residency and Citizenship Options for Investors and Nomads

Tax considerations often go hand-in-hand with questions of residency and citizenship. Each country offers different pathways for foreign investors or remote workers to reside there legally, which in turn can establish tax residency. Below we outline the residency and citizenship options in Bulgaria, Latvia, and Armenia – including any “golden visa” investor programs, digital nomad visas, or fast-track citizenship routes:

Bulgaria: EU Residency via Investment and Standard Permits

Bulgaria, as a member of the EU, is an attractive base for those seeking European residency and eventual citizenship. While Bulgaria previously had a fast-track citizenship-by-investment program, that program was officially cancelled in 2021 under EU pressure. However, Bulgaria still offers a “Golden Visa” type residency by investment (RBI) scheme. By investing a significant sum in Bulgaria, a non-EU national can obtain permanent residence relatively quickly, which can lead to citizenship through naturalization (typically after 5 years).

The current Bulgaria Investor Program for Residence requires, for example, an investment of at least €512,000 into approved assets (such as Bulgarian stock or government bonds, or into an Alternative Investment Fund) to receive permanent residency. Another option is investment in Bulgarian real estate – purchasing property worth at least BGN 600,000 (~€307,000) can qualify an individual for a residence permit. These investments must be maintained for a number of years. The key benefit is that permanent residents of Bulgaria can live and work in Bulgaria long-term and travel visa-free in the Schengen area. After holding permanent residency for five years (and meeting language and integration requirements), one can apply for Bulgarian citizenship via the ordinary naturalization process. Bulgarian citizenship then grants the right to live anywhere in the EU.

For entrepreneurs and digital nomads, Bulgaria does not have a labeled “digital nomad visa,” but it offers national long-term Type D visas and residence permits that can serve a similar purpose. One popular route is the Freelance/Remote Worker visa, which allows non-EU foreign nationals to reside in Bulgaria if they are self-employed or working for a foreign company. Applicants must show relevant qualifications or business registrations and sufficient funds. Essentially, Bulgaria can issue a one-year renewable residence permit for freelance work, which many remote workers use as a de facto nomad visa. Another route is to register a Bulgarian company and appoint oneself as the representative – this can qualify the person for a Business residency permit as a trade representative, under certain conditions.

In terms of tax residency, simply obtaining a Bulgarian residence permit doesn’t automatically make you a tax resident – you still need to spend more than 183 days in Bulgaria or demonstrate that Bulgaria is your center of vital interests for the year. But the combination of an easy-to-maintain residency permit and the 10% flat tax has made Bulgaria a favorite among international consultants and nomads who want an EU base.

Bottom line: Bulgaria offers a relatively streamlined path to EU permanent residency for those willing to invest or do business. While instant citizenship is no longer on the table, Bulgaria’s passport (once obtained) is very powerful. And even at the residency stage, Bulgarian PR coupled with tax residency can unlock the full benefits of Bulgaria’s low taxes and EU market access. Additionally, Bulgaria’s attractive corporate income tax rates make it an appealing destination for potential residents looking to optimize their business operations.

Latvia: Golden Visa (Residency by Investment) and Digital Nomad Visa

Latvia has been known for its residency-by-investment program (Latvian “Golden Visa”) which has several affordable options compared to other EU countries. As of 2024, Latvia’s Golden Visa allows third-country (non-EU/EEA) nationals to obtain a 5-year temporary residence permit in exchange for an investment in Latvia. The main investment pathways include:

Real Estate Investment: Purchase real estate in Latvia valued at €250,000 or more, plus a one-time fee (currently €50,000). The property must be in certain areas and meet criteria. This was historically the most popular route.

Business Investment: Invest at least €50,000 in equity of a Latvian company (plus a €10,000 state fee) if it’s a small company, or €100,000 in a larger company, creating jobs. This is one of the lowest entry points (effectively ~€60k total).

Government Bonds: Purchase €250,000 in special government bonds and pay a €38,000 fee.

Bank Deposit: Make a €280,000 subordinated deposit in a Latvian bank for 5 years, plus a €25,000 fee.

Once the investment is made and application approved, the investor gets a temporary residence permit (TRP) valid for 5 years (with renewals or checks periodically). There is no minimum stay requirement to keep the permit (apart from visiting Latvia once a year to renew registration), which means an investor could maintain Latvian residency rights without physically living there full-time. However, to transition from the TRP to permanent residency (PR) after 5 years, one must actually live in Latvia for the majority of that time (4 out of 5 years, >183 days per year). And citizenship in Latvia has strict requirements including language proficiency and long-term residence (typically 5 years PR and integration exams).

For digital nomads and remote workers, Latvia introduced a specific Digital Nomad Visa in 2022. This visa allows remote workers from OECD countries (e.g. USA, Canada, UK, etc.) to live in Latvia for up to one year, with a possible one-year extension. Applicants must prove they work remotely (employed or freelance) for a company outside Latvia and have a sufficient monthly income (at least 2.5 times the Latvian average monthly wage, roughly €2,800 per month as of 2023). The remote work visa does not grant the right to local employment (you cannot take a local Latvian job), but it lets you reside and work online from Latvia legally. This is an attractive option for non-EU nomads who want to base in an affordable EU country and enjoy Schengen travel. Latvia’s nomad visa is fairly streamlined (application through Latvian migration, proof of income, background checks) and valid for up to 2 years total.

In summary, Latvia offers both investment-based residency and remote work residency options. The Latvian Golden Visa has been one of the more accessible in the EU, though there have been discussions about tightening it (and some restrictions for certain nationalities). It attracted many investors by granting EU residency starting at €50k investment, which is significantly lower than similar programs in Western Europe. Meanwhile, the Digital Nomad Visa underscores Latvia’s openness to the growing community of location-independent professionals – allowing them to enjoy Latvia’s high quality of life (Riga’s vibrant culture, reliable infrastructure) while contributing economically. For tax purposes, a holder of any of these visas would need to spend >183 days in Latvia to become a tax resident; merely holding the visa doesn’t automatically impose Latvian taxation if one stays shorter periods. But those who do settle can then leverage Latvia’s tax advantages (like the corporate tax deferral and competitive corporate taxes).

Armenia: Easy Residency Paths, Dual Citizenship Friendly

Armenia is very welcoming to foreign investors and individuals when it comes to residency. Although Armenia is not in the EU, it provides a straightforward residency permit process and even allows for relatively quick naturalization in certain cases. There isn’t a formal “golden visa” program with large investment requirements because regular investment or employment routes are already accessible and not very costly.

Temporary Residence Permit (TRP): Any foreigner can apply for a one-year renewable temporary residence in Armenia if they have a legitimate reason – such as work in Armenia, owning a business, or being Armenian by origin/marriage. For entrepreneurs, a common route is to register a local company or invest in an Armenian business, which can qualify one for a TRP as an investor or shareholder. The financial threshold is low; even a small LLC formation might suffice if it’s active. For remote workers, Armenia currently doesn’t require visas for many nationalities for up to 6 months in a year, and if longer stay is needed, one can either extend or obtain a TRP by registering as a PE, for example, and showing freelancing activity and local address. The process is relatively quick (a few weeks) and inexpensive (state fees are modest). Armenia’s laws ensure foreigners receive equal treatment to citizens in business and property rights.

Permanent Residence (PR) Permits: After holding temporary residency for typically 3 years, or if a foreigner has a business or is of Armenian origin, they can apply for a Permanent Residence Card (valid 5 years, renewable). PR offers more security and is a step toward citizenship. Notably, Armenia also has a special Special Residence status for Diaspora Armenians and other distinguished foreigners – this is a 10-year residency card often given to ethnic Armenians from abroad or investors, which is quite advantageous.

Citizenship: Armenia allows dual citizenship freely and has been known to grant citizenship to foreign investors, entrepreneurs, and those of Armenian ancestry. Additionally, any person who has lived in Armenia for 3 years and passes a language/history exam can naturalize. The residency requirement can be waived for those with Armenian origins or other special merit. This means that, unlike Bulgaria or Latvia, Armenia could potentially confer citizenship in a shorter timeframe on a case-by-case basis – granting the individual an Armenian passport (which allows visa-free or e-visa access to countries like Russia, Iran, EU-Schengen visa facilitation, etc., though not as powerful as EU passports).

For digital nomads, Armenia is extremely accommodating: Many nationals (U.S., EU, UK, etc.) can stay visa-free in Armenia for 180 days per year, and others can easily get e-visas. Setting up local tax residency is possible without needing a formal “nomad visa” – essentially, if you like Armenia and decide to stay, you can register as an individual entrepreneur under the micro-business regime or set up a company, and then apply for a residence card. The low bureaucratic barriers and low cost of living (plus a booming tech scene in Yerevan) have recently drawn many remote IT workers to Armenia.

In summary, Armenia’s residency options are flexible and welcoming: there’s no high investment threshold; even a small business can facilitate residency. Foreign investors are treated equally under the law, and the country actively seeks to attract foreigners to settle and invest. The pathway to citizenship is also relatively liberal, making Armenia a noteworthy option for those who want a “plan B” residence or a new passport in a hospitable, low-tax country. Tax-wise, once you spend 183 days in Armenia, you become tax resident and can then enjoy the flat 20% tax (or special regimes if eligible) and Armenia’s growing network of tax treaties.

Tax Incentives and Special Programs

Beyond standard tax rates, each country offers tax incentives and special regimes to attract certain investors, industries, or activities, which can significantly reduce income taxes for those who qualify. These can significantly reduce the effective tax burden for those who qualify. Here we compare key tax incentives for individuals and corporations in Bulgaria, Latvia, and Armenia – such as R&D credits, startup tax breaks, regional incentives, and other programs in 2024/2025:

Bulgaria – Incentives: Regional CIT Relief and Hiring Credits

Bulgaria’s tax system is simple and low-rate by default, so it has relatively few special tax incentives. However, there are targeted programs to encourage investment in certain regions and to promote employment, which can significantly reduce personal income taxes for individuals and businesses:

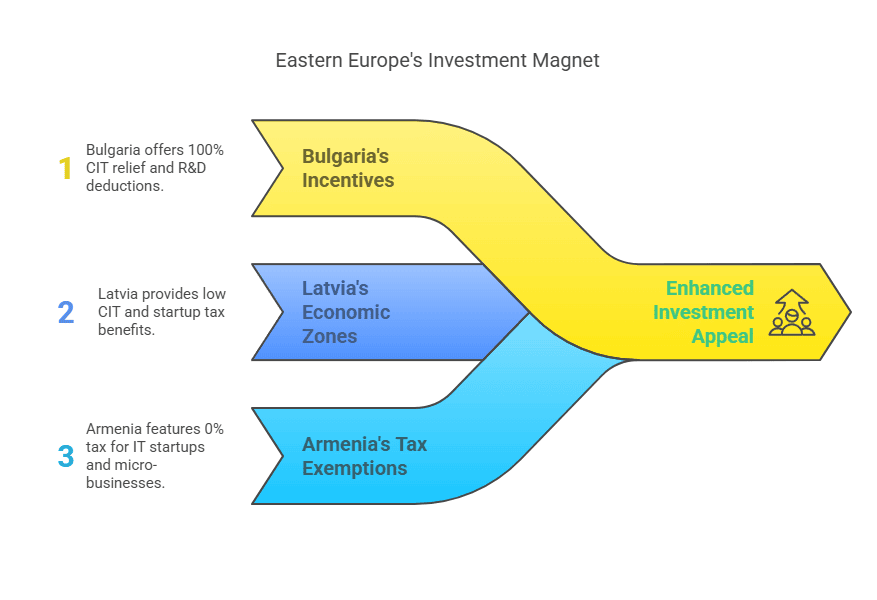

Regional Investment Incentive: Companies investing in municipalities with high unemployment can receive a CIT break of up to 100%. Essentially, if a company meets criteria (such as investing in manufacturing and creating jobs in a designated economically disadvantaged region), the government may grant back the corporate tax due, resulting in an effective 0% corporate tax for a period. This incentive is often used for sizable industrial projects and is aligned with EU state aid rules.

Hiring Incentives: Bulgaria provides additional tax deductions for employers hiring long-term unemployed, disabled, or older workers. This social incentive allows a company to deduct an extra amount from its taxable profit for each such hire, lowering its CIT.

Agricultural Incentive: Certain agricultural producers enjoy a partial exemption or reduction of CIT on their farm income, to support the farming sector.

R&D and Innovation: Bulgaria allows 100% immediate expensing of R&D costs (which is standard in many places) and has improved its IP regime. While Bulgaria doesn’t have a patent box regime, it aligns with EU innovation policies. According to one report, intangible assets from R&D can be deducted 100% which effectively encourages research investment.

VAT and Customs: Companies in Bulgaria can benefit from EU-wide regimes like Intra-Community supply 0% VAT (for exports to EU) and various EU customs reliefs. Bulgaria also has free zones but they mostly confer customs duty/VAT deferral rather than tax holidays.

Notably, Bulgaria does not impose local taxes on personal wealth, inheritance (for close relatives), or financial transactions, which is an implicit incentive for high-net-worth individuals. Also, capital gains on listed securities are exempt from tax, encouraging stock market investments.

For individual investors moving to Bulgaria, while there isn’t a special expat tax regime (like “non-domiciled” regimes elsewhere), the flat 10% rate itself is the incentive – it applies equally to locals and foreigners, and there are no foreign income remittance taxes. Bulgaria’s extensive network of double tax treaties (over 70 treaties) can reduce withholding taxes on cross-border income and provide tax credit mechanisms, benefiting international businesspeople.

Latvia – Incentives: Special Economic Zones, Startup Regime, and Holding Benefits

Latvia complements its unique CIT system with several tax incentives targeting investors that significantly reduce corporate income tax rates:

Special Economic Zones (SEZ) and Free Ports: Latvia has five designated zones (including Riga Free Port, Ventspils Free Port, Liepāja SEZ, Rēzekne SEZ, Latgale SEZ) where companies can receive 80% reductions in corporate tax and property tax. Companies operating in an SEZ under certain conditions effectively pay only 20% of the normal tax, which makes the effective CIT rate as low as 4% (since 20% of the normal 20% CIT = 4%). They also get an 80% rebate on real estate tax and relief on withholding taxes for certain payments. These incentives are to attract manufacturing, logistics, and industrial projects to specific regions.

Large Investment Relief: Latvia has, at times, provided CIT relief for major investments (above certain tens of millions of euros) in the form of allowing those investors to reduce future CIT when they do distributions. This is usually negotiated case-by-case in line with EU state aid.

Startup Tax Regime: To foster the startup ecosystem, Latvia introduced a special regime for certified innovative startups. Instead of the usual labor taxes (which are considerable, ~34% employer+employee social tax plus PIT), qualifying startups can opt for a fixed flat social tax per employee (around two minimum salaries) and a 0% PIT on those employees’ stock options (provided they hold them for at least 12 months). This significantly lowers the cost of employing highly skilled workers (like developers) in early-stage startups. In essence, the government subsidizes the startup by capping the tax per job, making Latvia a competitive location for new tech companies.

Holding Company Advantages: Latvia has a 100% exemption on dividends received from foreign subsidiaries (except those in blacklisted tax havens) and generally does not tax capital gains on the sale of shares (if certain conditions are met, e.g., the subsidiary was held for at least 36 months). This, combined with the no tax on undistributed earnings, makes Latvia very attractive as a holding company jurisdiction for Eastern Europe. Profits can flow into a Latvian holding company with little or no tax, and be redeployed elsewhere.

Personal tax incentives: Latvia provides a non-taxable minimum income allowance for low earners and certain deductions (for mortgage interest, education, etc.), but for high-net-worth expats, a notable point is that foreign pension income can be exempt for retirees under certain treaties, making Latvia a potential retirement haven. Additionally, real estate rental income can be taxed under a special regime at 10% (if one opts for simplified taxation), which is favorable for property investors.

In 2023, the International Tax Competitiveness Index ranked Latvia #2 globally (only behind Estonia) in large part due to these competitive tax features. The government’s aim is clearly to incentivize reinvestment and attract global business. Whether you are launching a startup, building a manufacturing plant in Latgale, or setting up a holding company, Latvia’s tax system has tailored benefits to minimize the tax friction.

Armenia – Incentives: IT/Tech Tax Holidays, Micro-business Exemption, Free Zones

Armenia, seeking to become a tech and investment hub in its region, has implemented generous tax incentives that significantly reduce corporate taxes:

IT Startup Incentive: Armenia’s flagship incentive has been its tech startup tax holiday. Startups in information technology (software, etc.) can apply for a certification that grants zero percent profit tax and only 10% income tax on employees’ salaries, valid up to 5 years (this program, launched in 2015, was extended through 2024). As noted earlier, new legislation effective 2025 refines this: certified high-tech companies get a 1% turnover tax (instead of 18% profit tax) and a 10% personal tax rate on R&D and engineering staff until 2031. This means a qualifying tech firm essentially keeps almost all its earnings tax-free and can offer a low 10% flat tax to its talent, making Armenia extremely competitive in tech. This incentive has been a key driver of the rapid growth of the IT sector in Armenia.

Micro-entrepreneurship Exemption: Small businesses (individual entrepreneurs or very small firms) under AMD 24 million turnover (~$60k) qualify as “microbusiness” and pay no VAT, no profit tax. Many local and foreign consultants, artisans, and small traders use this regime – effectively enjoying tax-free status on their business income. There are restrictions (certain activities like consulting for large companies might be excluded to prevent abuse), but it’s a broad boon to grassroots business.

Turnover Tax Regime: Slightly larger SMEs can opt for a turnover tax (a simplified tax on gross revenue) instead of the normal VAT and profit tax. Rates vary by sector (e.g., 1.5% for trading, 5% for consulting services, etc.). This often reduces the tax burden for businesses with lower profit margins or simpler operations, and it simplifies bookkeeping (no need for full accrual accounting for taxes).

Free Economic Zones: Armenia has established Free Economic Zones focusing on high-tech, manufacturing, and logistics (e.g., Alliance FEZ for tech, Meghri FEZ on the Iran border). Companies in an FEZ enjoy 0% profit tax, 0% VAT, 0% import/export customs duties, and 0% property tax on their operations within the zone. This is aimed at export-oriented businesses – for instance, a manufacturing company producing in Armenia for export can operate tax-free in an FEZ (only paying employee taxes).

Sectoral Incentives: Beyond IT, Armenia also offers incentives in sectors like agriculture (e.g., farmers benefit from reduced tax; small agricultural producers pay almost no income tax), and in border regions. As a national security and development measure, businesses operating in certain border villages get full tax exemptions (no profit tax, no VAT, no turnover tax) to encourage economic activity in those vulnerable areas. The government also occasionally grants tax holidays for strategic investments via individual agreements, such as postponing VAT on imported equipment for 3 years for large projects.

Personal Incentives: For individual taxpayers, Armenia’s system is straightforward (20% flat), but there is a 0% tax on interest from Armenian government bonds, and certain foreign-source incomes might be exempt under specific circumstances or treaties. Additionally, repatriates (members of the Armenian diaspora returning) have no special tax on bringing in assets, and foreign pensions aren’t taxed. Foreign citizens who hold residency cards in Armenia are required to pay social security contributions, including pension payments. Therefore, social security tax is not waived based on foreign citizenship alone, and standard contributions apply. However, Armenia’s overall labor tax burden remains relatively modest compared to many countries, which helps keep the cost of employing expats competitive.

Overall, Armenia’s incentives reflect its strategy to attract key industries and empower small entrepreneurs. A foreign investor could practically start a small venture and pay almost no tax for years under these programs. These layers of relief can make Armenia a kind of tax haven for active business operations, even though it is a normal-tax country on paper.

Ease of Doing Business

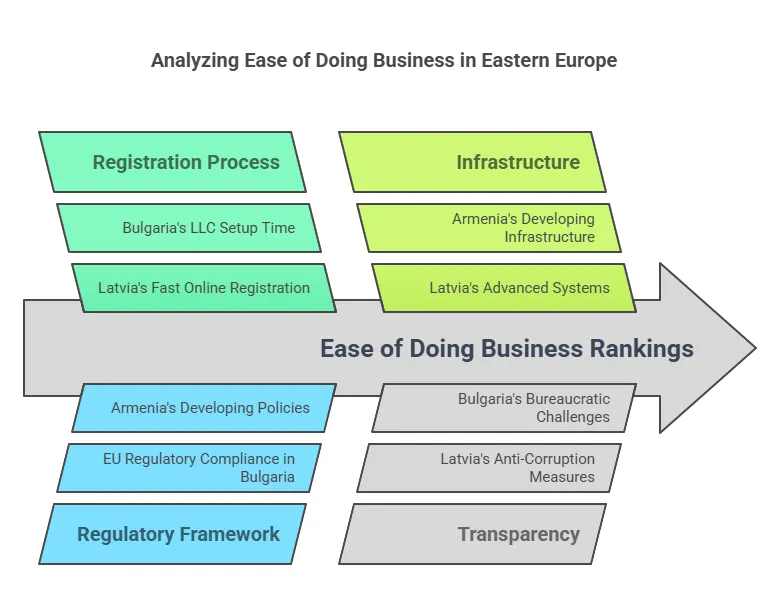

When choosing a jurisdiction, the ease of doing business – how quickly and simply one can start and run a company, deal with permits, and comply with regulations – is critical. All three countries have worked to improve their business climates, but they rank differently in global surveys compared to other countries in the world. According to the last World Bank Doing Business 2020 report (which ranked regulatory ease among 190 economies), Latvia outranks Bulgaria and Armenia by a significant margin. Latvia was 19th in the world for ease of doing business in that 2020 index, whereas Bulgaria was 61st and Armenia 47th. This suggests Latvia has a more streamlined business environment overall. Let’s break down some practical aspects:

Company Formation: Latvia – Company registration is very quick and largely online. Using an e-ID and e-Signature, one can incorporate a new SIA (Latvian LLC) in 1–3 days. The minimum share capital can be as low as €1 (for a “startup SIA”) if certain conditions are met, otherwise €2,800 for a standard SIA. The process can be done remotely for foreign investors (through Latvia’s user-friendly online business registry). Bulgaria – Company registration requires some notarized documents but is still relatively fast: typically around 3–5 working days with all paperwork in order. The minimum capital for an LLC (OOD) is only BGN 2 (~€1), essentially zero, which is a big plus. Foreigners can own 100% of a company and even complete registration via power of attorney if not physically present. Bulgaria has also introduced online filing for some steps, but it may not be as fully digitized end-to-end as Latvia’s system. – Starting a business in Armenia is straightforward and can often be done in 1–2 days as well. The minimum capital for an LLC is not required (0 AMD) unless otherwise specified by founders. Armenia’s business registry allows online name reservation and there are one-stop shops that handle tax and social registration automatically upon incorporation. In the Doing Business 2020 “Starting a Business” sub-index, Armenia was actually ranked #10 globally, reflecting very quick procedures. One can register a business on the government portal, and formalities usually take no more than 1–2 weeks even in worst case.

Administrative Burden & Compliance: Latvia shines in having a transparent, digital administration. Tax filing and payments are online via the Electronic Declaration System. Getting permits, registering property, and accessing public services are relatively efficient. For example, VAT registration or getting export/import documentation in Latvia is known to be smooth. Latvia’s government has even implemented a “Green Corridor” to fast-track administrative procedures for large investors, cutting approval times in half for things like territorial planning and work permits. Bulgaria, while improved over the years, still has a reputation for bureaucracy. Online tax filing exists, but businesses often need local counsel to navigate procedures, especially for construction permits or obtaining certain licenses. Nevertheless, routine tasks like paying taxes have become easier – Bulgaria was ranked fairly well on the “Paying Taxes” indicator. One common observation is that registering property or getting electricity can be slower in Bulgaria than in Latvia. Armenia has significantly reformed its processes post-2018. Many services are going online (for instance, you can file taxes online and even register employees through e-governance portals). Armenia also merged many inspections into a unified body to reduce red tape. According to investors, Armenia’s small size means you can often get things done by directly contacting officials, and the legal requirements are not overly complex. However, some areas (like customs procedures or court enforcement) can still pose challenges.

Time to Start Operations: If an investor landed in each country, roughly how fast could they be up and running? In Latvia, potentially within a week you could have a fully registered company with a bank account. In Bulgaria, within 1–2 weeks given the need for notarization and local bank account setup (which can take a few days). In Armenia, similarly within a week or so; plus, interestingly, a foreign individual in Armenia can operate initially as a sole proprietor (registering as an “IE”) even faster, and later incorporate if needed.

Infrastructure & Banking: All three countries have modern banking systems open to foreigners, though Latvian banks are highly EU-regulated and may have stringent compliance (as Latvia cleaned up issues related to non-resident banking). Bulgarian banks are stable (Bulgaria is in the EU Banking Union) and opening an account for a local company is straightforward. Armenian banks are quite foreigner-friendly and often allow remote account opening once you have proper ID and registration – they are used to serving diaspora and investors from Russia/Iran etc., and they have English online banking interfaces.

In terms of World Bank Doing Business scores: Latvia’s high rank indicates it offers a generally easier environment across multiple metrics. Armenia did quite well too, especially in starting a business and getting credit, but was weighed down by things like getting electricity or trading across borders. Bulgaria, while the lowest of the three in rank, still isn’t a terribly difficult environment – its overall score was around 72/100, meaning regulations are reasonably conducive, but it lagged in areas such as enforcing contracts and dealing with construction permits.

To sum up, Latvia is the leader in ease of doing business among the three, with a very fast company setup and digital administration – a plus for entrepreneurs who value efficiency. Armenia is surprisingly agile for a non-EU, developing economy – one can start businesses quickly and deal with relatively business-friendly authorities (and it’s improving its e-government). Bulgaria, while having the advantage of EU integration, still contends with some old-school bureaucracy, but it offers a stable framework and has improved gradually. All three allow 100% foreign ownership and have no restrictions on profit repatriation, which are fundamental ease-of-business factors.

Regulatory Transparency and Legal Environment

The broader legal environment – including transparency, rule of law, and regulatory stability – is a crucial factor for investors and HNW individuals. A transparent regulatory environment can significantly reduce tax burdens, making it an attractive option for businesses and individuals. Here’s how Bulgaria, Latvia, and Armenia compare:

European Union Framework vs. Emerging Market: Bulgaria and Latvia, as EU members, adhere to EU regulations on trade, competition, and investor protection. This means robust legal protections (e.g. enforcement of contracts under EU law, intellectual property protections aligned with EU directives, and recourse to European courts in some cases). Latvia in particular has been praised for strong reforms in governance and fighting corruption since joining the EU and OECD. Armenia, not being in the EU, has its own legal system which has been modernizing, especially after a peaceful revolution in 2018 brought a reformist government. Armenia signed a Comprehensive Partnership Agreement with the EU to harmonize many regulations, but it’s still developing its institutions independently.

Transparency and Corruption: According to Transparency International’s Corruption Perceptions Index, there are clear differences. Latvia scores around 59/100, reflecting a mid-to-high ranking (it is viewed as having relatively controlled corruption, comparable to Czech Republic or Spain). Bulgaria, unfortunately, scores lower (around 43/100 in CPI) – one of the lower scores in the EU – indicating ongoing challenges with corruption and rule of law (e.g., slow judicial processes, issues in public procurement). Armenia scores around 46/100 (improved after 2018 from mid-30s previously), indicating moderate corruption: better than many CIS countries, but still with room to strengthen institutions. However, Armenia’s upward trajectory in CPI suggests reforms are yielding results.

Legal System and Courts: Latvia’s judiciary is generally considered fair and in line with European standards, though like many countries, complex cases can be slow. It has specialized courts for economic disputes and investment protection as part of the EU framework. Bulgaria’s judiciary has had criticism regarding inefficiency and susceptibility to political influence, but as an investor, one benefits from Bulgaria being part of international arbitration conventions and the ability to appeal to EU-level institutions. Armenia’s legal system is mixed: laws on the books are quite investor-friendly (e.g., strong protections in the Foreign Investment Law guaranteeing no discrimination and allowing international arbitration). In practice, contract enforcement through courts can be slow, but arbitration is available. The government actively encourages investors to use arbitration (Armenia is a member of ICSID). Notably, foreign investors in Armenia are entitled to the same treatment as locals by law, and there’s no expropriation risk without fair compensation (and no such cases in recent history).

Regulatory Stability: All three countries have been relatively stable in their tax laws – no sudden drastic changes without notice. Bulgaria has kept its low tax rates consistent for over a decade. Latvia made a big change in 2018 for CIT but that was a pro-business reform; recent personal tax increases were telegraphed in advance and still keep rates moderate. Armenia undertook comprehensive tax reform in 2019, lowering rates and simplifying the code. Investors generally prefer Armenia’s new tax code for its clarity. Each country has investment promotion agencies (InvestBulgaria, LIAA in Latvia, Enterprise Armenia) that provide transparency about incentives and legal procedures to investors.

Treaties and International Agreements: Bulgaria and Latvia as EU members are part of EU free trade agreements and Bilateral Investment Treaties (BITs) through the EU umbrella (though intra-EU BITs are being phased out). They also follow EU banking regulations (CRS – Common Reporting Standard – for automatic exchange of tax information, etc.). Armenia is part of the Eurasian Economic Union (with Russia, Kazakhstan, etc.), which means free trade and movement of goods with those countries, and a common external tariff. Armenia also benefits from EU GSP+ trade preferences (duty-free export on many products to the EU). In terms of tax, Armenia joined the OECD Inclusive Framework and is implementing international standards (like BEPS minimum standards). All three have double taxation treaties: Bulgaria ~70, Latvia ~60, Armenia ~50 treaties – providing investors ways to avoid double taxation when operating internationally.

Investor Protections: Each country offers some form of investment incentives legislation and protection against arbitrary changes. For example, Armenia’s Law on Foreign Investments guarantees 5-year stability of business environment – meaning if laws worsen, an investor can choose the older law for up to 5 years from investment. Bulgaria and Latvia, under EU law, cannot discriminate against foreign EU investors, and in practice extend the same courtesy to others; plus, they are subject to EU investment court jurisdiction for disputes in some cases.

Political and Geopolitical Context: It’s worth noting non-tax factors: Bulgaria and Latvia are NATO members and politically integrated in the West, which adds a layer of geopolitical stability for investors from allied countries. Armenia’s region is more geopolitically tense (borders with Azerbaijan and Turkey closed, recent conflicts in the area). While Armenia itself has been stable internally and very welcoming to global tech firms (many relocated from Russia/Belarus recently), investors should be mindful of regional dynamics. However, Armenia maintains good relations with big powers (Russia security alliance, EU partnerships, and recently improving dialogue with neighbors), and this hasn’t resulted in any foreign investor exodus – in fact FDI in Armenia has been rising.

In terms of transparency: Latvia often scores well on governance indices and has a relatively transparent public sector (e.g. e-procurement systems, open data). Bulgaria is improving but still has some opacity in public administration. Armenia made significant strides in transparency after 2018 – for example, asset declarations of officials are public, and efforts to digitalize services reduce face-to-face corruption opportunities.

Bottom line: For an international investor or entrepreneur, Latvia offers the most confidence in regulatory transparency and rule of law, closely aligned with Nordic standards. Bulgaria, while offering excellent tax terms, may require a bit more due diligence and local advice to navigate bureaucratic quirks, but it benefits from the overarching EU legal order which protects investors from extreme outcomes. Armenia offers a surprisingly open and equal legal playing field for foreigners and very pro-business laws, but as an emerging market, one might encounter more practical hurdles in bureaucracy or courts – though the government’s pro-investor stance often helps resolve issues. Many investors in Armenia rely on personal relationships and government support programs to get things done efficiently.

Conclusion

Bulgaria, Latvia, and Armenia each present compelling low-tax, business-friendly environments, but for slightly different strategic niches:

Bulgaria is a classic low-tax EU jurisdiction – a flat 10% tax on personal and corporate income, making it one of the best EU tax jurisdictions in 2025 for flat taxes. It appeals to entrepreneurs and HNWIs who want simple and ultra-low taxes while being in the EU. Bulgaria offers the additional draw of EU residency (with a path to citizenship) for investors. It’s ideal for someone who wants to live in or service the EU market, keep taxes minimal, and can handle a bit of local bureaucracy. A hypothetical case: A high-net-worth individual moves to Sofia, becomes tax resident – all his worldwide income is then taxed at 10%. If he sets up a Bulgarian company for his consulting business, it pays 10% CIT and he pays 5% on dividends – an extremely low effective tax while enjoying an EU lifestyle.

Latvia stands out for its innovative corporate tax system and overall ease of business. It may not have as low a personal tax as Bulgaria, but it still stays moderate (progressive 25%/33%, with ~36% at the very high end). Crucially, entrepreneurs reinvesting profits pay 0% CIT in Latvia – a huge advantage for growth companies and holding structures. Combined with high transparency and an efficient government, Latvia is often seen as a tax-efficient gateway to the EU. For example, a tech startup in Riga can raise funding, reinvest earnings without tax until profitable, benefit from startup payroll incentives, and the founders pay themselves reasonable salaries taxed at 25%. If they later exit, the corporate retained profits can be distributed at 20% CIT and no additional dividend tax – rewarding them for deferring distribution. Latvia also provides residency options from the relatively accessible Golden Visa (starting ~€60k investment) to a Digital Nomad visa, making it flexible for different types of investors.

Armenia offers a non-EU alternative with surprisingly competitive tax benefits. With a flat 20% income tax and 18% corporate tax (often reduced to 0–10% under special regimes), Armenia is attracting entrepreneurs, especially in tech and IT. Its special tax benefits – micro-business exemption, and free economic zones – can make the effective tax rate nearly zero for qualified investors. Residency in Armenia is easy to obtain and comes with no-nonsense equal treatment for foreigners. Consider a digital nomad or investor who sets up a base in Yerevan: they register as a micro entrepreneur (0% tax) for their freelancing and enjoy a low cost of living. Armenia is especially appealing for those who don’t mind being outside the EU bloc and perhaps have interest in the Eurasian region.

In choosing between these jurisdictions, investors should weigh tax benefits vs. other factors: Latvia and Bulgaria give the advantage of EU membership (market access, stronger legal recourse, mobility), while Armenia offers ultra-flexible incentives and a blank-slate environment eager for investment. Bulgaria vs Latvia vs Armenia in taxes comes down to the specifics of one’s situation:

For purely lowest personal and corporate tax rates, Bulgaria wins on headline numbers (10% flat).

For corporate tax optimization and reinvestment, Latvia’s system is unparalleled in the EU (0% until distribution).

For startups and small business support, Armenia’s targeted tax holidays can deliver near-zero tax and its bureaucracy will not overwhelm a small operation.

All three countries are actively courting foreign investors and digital nomads, and tax benefits in Armenia, Latvia, and Bulgaria are part of that strategy. They have positioned themselves among the low tax countries in Eastern Europe that combine favorable tax policy with improving business climates. A savvy investor or advisor will consider not just the tax rates, but also lifestyle, legal stability, and strategic location. The good news is that whether it’s the EU corners of the Baltics or Balkans, or the Caucasus gateway, Eastern Europe offers some of the best tax jurisdictions for those seeking a hospitable home for themselves and their businesses.