International investors often compare Romania vs Bulgaria when seeking low tax EU jurisdictions for corporate expansion. Both countries offer relatively favorable tax regimes in Eastern Europe, but they differ in key aspects of corporate taxation and business climate. This article provides a comprehensive tax comparison – covering corporate income tax, withholding tax, VAT, social contributions, R&D incentives, sector-specific perks, and regulatory factors – to help corporate planners and tax advisors determine which jurisdiction offers more advantageous conditions for establishing and growing a company.

Romania and Bulgaria, both EU member states, have become attractive to international investors due to their competitive tax rates and developing markets. Bulgaria is known for its ultra-low flat taxes and stable macroeconomy, whereas Romania boasts a larger domestic market and ongoing simplification of bureaucracy. Each country’s tax system has unique advantages and drawbacks. Investors must weigh factors such as corporate tax rates, tax incentives, labor costs, and ease of doing business.

Corporate Income Tax Rates and Structures

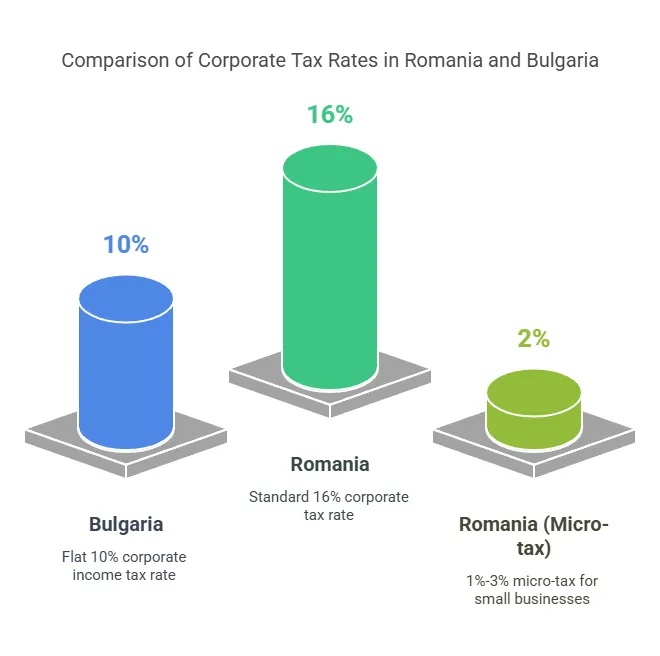

One of the first considerations is the corporate income tax (CIT) rate. Both Romania and Bulgaria levy flat corporate tax rates, but Bulgaria’s rate is significantly lower:

Bulgaria’s CIT Rate: 10% flat on taxable profits – one of the lowest in the EU. This rate applies uniformly to resident and non-resident companies on Bulgaria-source profits. The low 10% CIT is a major Bulgaria tax benefit attracting holding companies and cost-sensitive businesses.

Romania’s CIT Rate: 16% flat on taxable profits. Romania’s standard CIT is higher than Bulgaria’s, but still below the EU average (~21%). Notably, Romania offers an alternative micro-company tax regime for small businesses, which can substantially reduce the effective tax burden for qualifying firms.

Micro-Enterprise Regime in Romania

Romania’s micro-enterprise income tax regime provides a turnover-based tax for small companies, instead of the 16% profit tax. Key features as of 2025:

Eligibility: Companies with annual revenues below €500,000 (approx. RON 2.5 million) may opt into the micro-enterprise regime, provided they meet certain criteria (e.g. having at most 20% income from consulting, and other conditions). Newly established companies initially default to profit tax but can switch to micro tax if eligible.

Micro Tax Rates: 1% or 3% of turnover, depending on conditions. Specifically, 1% applies to micro-firms with annual revenues up to €60,000 that do not operate in certain excluded sectors. A higher rate of 3% applies to micro-companies with revenues above €60,000 up to €500,000, or those engaged in designated activities (such as software development, hospitality, legal and medical services, etc.). These tiered rates were introduced in 2023 to better target the micro-tax’s benefits. Notably, Romania eliminated its 3% rate for micro-firms with no employees; now all qualifying micros pay 1% or 3% based on turnover and sector.

Impact: The micro regime can be highly advantageous for small businesses with high profit margins. For example, a consulting SRL with €100,000 revenues and €50,000 profit would owe only €3,000 under the 3% turnover tax, instead of €8,000 under the 16% profit tax. However, sectors like software development and hotels are mandated to use the 3% rate even at low turnover, reflecting Romania’s policy to ensure certain industries contribute a bit more. If a micro-firm exceeds the €500k cap, it must switch to the 16% profit tax regime mid-year.

Bulgaria, by contrast, does not have a separate micro-company tax – all companies face the 10% profit tax regardless of size. This simplicity can be seen as a plus for predictability, though it means small firms in Bulgaria don’t get a further reduced rate beyond the already-low 10%.

Comparative Corporate Tax Overview

To summarize the basic corporate tax parameters in each country, the table below highlights key figures:

| Tax Aspect | Romania | Bulgaria |

|---|---|---|

| Corporate Income Tax (CIT) | 16% standard on profits. Micro-enterprises: 1% or 3% of revenue if turnover ≤ €500k | 10% flat on profits (applies to all companies) |

| Dividend Withholding Tax | 10% standard. 0% intra-EU (EU parent holding ≥10% for ≥1 year) | 5% standard. 0% intra-EU (EU parent holding ≥10% for ≥1 year) |

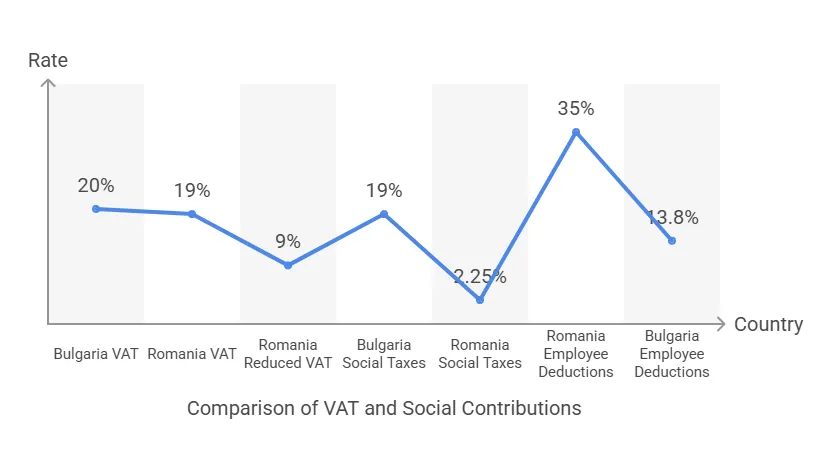

| VAT (Standard Rate) | 19% standard (reduced rates 9% and 5% on specific items) | 20% standard (reduced rate 9% for some goods/services) |

| VAT Registration Threshold | ~RON 300,000 annual turnover (≈ €60,000) for mandatory VAT registration | BGN 100,000 annual turnover (≈ €51,000) for mandatory VAT (see VAT section for 2025 ch |

| Employer Social Contributions | ~2.25% of gross salary (standard work conditions) + 4% or 8% for special/hazardous conditions | ~18.9–19.6% of gross salary (varies slightly by accident risk category) |

| Employee Social Contributions | 35% of gross salary (25% pension + 10% health) | ~13.8% of gross salary (10.58% pension + 3.2% health) |

| Personal Income Tax (PIT) | Flat 10% on most income.Tech/Constr./Agric. employees exempt on first ~RON 10k | Flat 10% on income (no general sector exemptions) |

As shown, Bulgaria’s headline rates (10% CIT, 5% dividend tax, 20% VAT) are lower across the board than Romania’s (16% CIT, 8% dividend tax, 19% VAT). However, Romania’s special regimes (micro-tax, sector incentives) can narrow the gap for certain businesses. Next, we examine each tax category in detail.

Dividend Withholding Tax

When a company distributes profits as dividends, the withholding tax (WHT) on dividends is another important consideration for investors, especially those planning to repatriate profits.

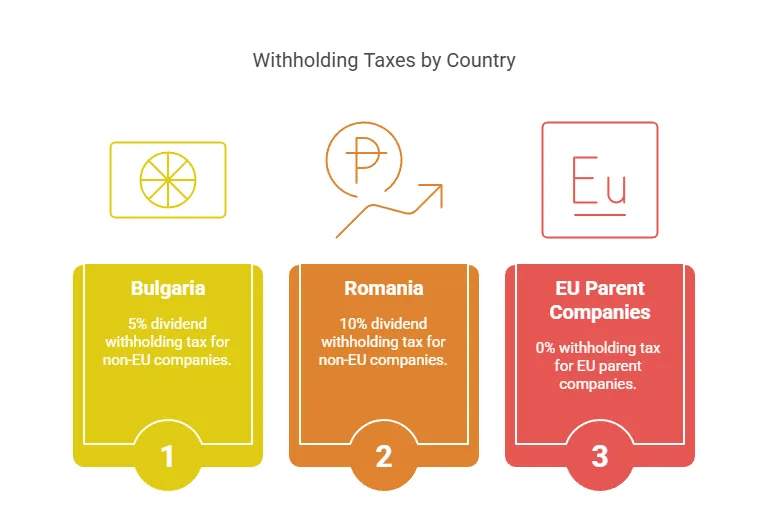

Bulgaria – Dividend Tax: Bulgaria imposes a 5% withholding tax on dividends paid to individuals or foreign corporate shareholders. This rate applies to dividends paid to most non-residents, but there is no dividend WHT for EU/EEA parent companies meeting the EU Parent-Subsidiary Directive conditions (at least 10% ownership for ≥1 year) – those distributions are exempt. Many of Bulgaria’s tax treaties can also reduce the 5% rate on dividends to 0–5% for other jurisdictions. A 5% dividend tax is very low by EU standards (e.g. Germany 25%, Poland 19%).

Romania – Dividend Tax: Romania’s dividend tax rate has recently increased. It was long set at 5%, but from 2023 it rose to 8%, and as of January 1, 2025 it further increased to 10%. In 2025 investors should expect 10% WHT on dividends. Like Bulgaria, Romania implements the EU Parent-Subsidiary Directive, so dividends paid to a qualifying EU parent company (≥10% share for ≥1 year) are exempt from withholding. Domestic dividends between Romanian companies are also tax-exempt to avoid double taxation. For non-EU or non-treaty destinations, the 8%/10% rate applies by default.

Impact: Bulgaria clearly has an edge with its 5% dividend tax versus Romania’s 8–10%. For investors planning regular profit repatriation to a parent company in a non-EU jurisdiction, Bulgaria’s lower rate means more post-tax dividends. For EU-based investors, however, this difference may be moot, since both countries allow 0% withholding on EU dividends under EU rules. In practice, many international groups structure investments via EU holding companies to utilize the 0% EU WHT – in such cases, neither Romania nor Bulgaria would levy dividend tax on the exit.

It’s worth noting Romania’s increasing rate trend: the jump to 10% aligns the dividend tax with its flat PIT of 10%. This could slightly reduce Romania’s attractiveness for holding companies. Bulgaria, on the other hand, has kept its rate at 5% for years.

Real-World Scenario: If a U.S. investor owns a Bulgarian company, a $1 million dividend would incur $50k Bulgarian tax (5%). The same dividend from a Romanian company in 2025 would incur $100k tax at 10%. By routing the investment through, say, the Netherlands or Cyprus (EU jurisdictions with tax treaties), investors often can reduce or eliminate these withholding taxes. Both Romania and Bulgaria have extensive tax treaty networks to mitigate cross-border dividend taxation.

VAT Systems and Registration

Value-Added Tax (VAT) affects companies’ cash flow and pricing, especially those selling goods/services locally or across the EU. Both countries use the EU VAT framework, but with different rates and thresholds:

VAT Rates: Romania’s standard VAT rate is 19%, slightly lower than Bulgaria’s 20% standard rate. Both have reduced VAT rates for specific categories: 9% in each country on items like books, pharmaceuticals, hotel accommodations, etc. Romania also has a super-reduced 5% VAT on certain goods (e.g. residential housing, cultural events). The difference of 1 percentage point in standard VAT is minor, but could influence large consumer-oriented businesses (Romania’s slightly lower VAT may ease end-customer prices by ~1%).

VAT Registration Threshold: This is a key difference as of 2024. In Romania, businesses must register for VAT once annual turnover exceeds RON 300,000 (approximately €60,000). In Bulgaria, the threshold was historically BGN 50,000 (€25k), but was raised to BGN 100,000 (≈ €51,000) from 2023. Thus, Romania currently allows a higher sales volume before mandatory VAT than Bulgaria does. However, EU legislation permits thresholds up to €85,000, and Bulgaria planned to raise its threshold further to the equivalent of €85k (BGN 166,000) in 2025. (As of early 2025, Bulgarian lawmakers decided to revert the threshold back to BGN 100k from April 2025 onward, after briefly allowing the higher limit. Investors should check the latest threshold, as policy has fluctuated.) In short, a small business can operate VAT-free on somewhat higher revenues in Romania (€60k) than in Bulgaria (~€50k).

VAT Compliance: Both countries require filing periodic VAT returns (monthly or quarterly, depending on turnover). Being EU members, Romanian and Bulgarian companies can obtain EU VAT numbers and trade across the EU using the reverse-charge mechanism and One-Stop-Shop (OSS) systems where applicable. Compliance has some differences – e.g., Romania introduced SAF-T digital reporting for VAT for large taxpayers, whereas Bulgaria has been slower in such mandates. But generally, VAT administration is comparable.

For international investors, the main VAT consideration is often cash-flow impact and registration hassle. If an investor plans only to export services/goods (zero-rated for VAT) and remain under the threshold, they might initially avoid VAT registration. In Romania, three small related companies could each use the €60k threshold (Romanian law allows up to 3 VAT-exempt firms per individual owner), potentially aggregating €180k sales VAT-free. In Bulgaria, the threshold is slightly lower, and splitting businesses to avoid VAT is more limited.

Example: A startup software firm expects €50k annual domestic sales in the first year. In Romania, it can delay VAT registration until it grows past €60k, sparing it from charging and filing VAT initially. In Bulgaria, it would cross the ~€51k threshold and need to register a bit sooner. On the flip side, once registered, Romanian VAT is 19% vs Bulgarian 20%. Either way, both countries’ VAT regimes grant full input VAT deduction on business purchases and align with EU directives, so VAT should not be a cost if managed properly, just an administrative factor.

Employer and Employee Social Contributions

Beyond corporate taxes, labor taxation – social security and payroll costs – affect the total cost of doing business, especially for companies with significant staffing. Both Romania and Bulgaria have flat income tax of 10% on individuals (making them attractive for employees), but social contributions differ in rates and structure:

Romania – Social Contributions: In a major 2018 reform, Romania shifted most social security burden onto employees. As of 2024, employees pay 25% for pension (social insurance) and 10% for health insurance, totaling a 35% employee contribution withheld from gross wages. Employers pay only a small Work Insurance contribution of 2.25% on gross payroll in normal conditions. (If employees work under special conditions – e.g. hazardous jobs or early retirement roles – the employer must contribute an extra 4% or 8% for pensions.) Importantly, Romania has sector-specific relief for social taxes in some industries: for example, the construction sector currently enjoys zero income tax and lower contributions for employees up to a certain wage, as an incentive to combat labor shortage in that field. But generally, for budgeting, a Romanian employer might gross-up an employee’s salary by ~2.25% for employer costs, and the employee’s net will be ~55% of gross after 35% social contributions and 10% income tax (with some nuances at lower incomes).

Bulgaria – Social Contributions: Bulgaria splits the social security burden between employer and employee at roughly 60:40 ratio. For typical office employees, the employer pays around 18.9% of salary (covering social insurance, health insurance, and accident fund) and the employee pays about 13.8%. Specifically, employer rates include ~13.7% for pensions, 4.8% for healthcare, and ~0.4–1.1% for accident insurance (the exact total ranges ~18.9–19.6% depending on risk class). Employees pay 10.58% for pension and 3.2% for health, from their gross pay. Bulgaria’s personal income tax is a flat 10% on top of this. There are no broad sector exemptions for IT or construction; however, Bulgaria does cap the maximum income subject to social security (around BGN 3,400 per month in 2024), which can reduce the relative burden for higher salaries (income above the cap is not charged social contributions). Romania also has an earnings cap for social contributions (the health insurance 10% is capped at 12x minimum wage for certain freelancers, but for employees the pension has a cap of 3x average wage for Pillar II contributions – details vary).

Comparison: For an employer, labor cost per €1 of net salary can be illustrative. In Romania, to give an employee a net €1,000, the gross might be ~€1,315 (since 24.5% total tax: 35% SSC and 10% PIT on gross, offset somewhat by PIT applying after SSC). The employer pays an extra 2.25% of gross (€30), so total cost ~€1,345. In Bulgaria, to net €1,000, gross ~€1,270 (13.8% SSC + 10% PIT on gross), and employer pays 19% of gross (€240), totaling ~€1,510 cost. Thus, Romania’s recent tax shift made its formal labor slightly cheaper for employers (the employee bears more of the tax). However, employees in Romania see a bigger chunk taken from gross pay for social insurance, whereas in Bulgaria the split is more balanced. For investors, both countries offer competitive labor costs compared to Western Europe, but Bulgaria’s average wages are lower to begin with, which often outweighs the percentage differences in social taxes.

Employee Tax Incentives (IT Sector): One notable difference is incentives for tech sector employees. Romania has long granted income tax exemptions for IT professionals – software developers with certain qualifications have been exempt from the 10% PIT (effectively making their income tax 0) up to a limit, a policy to spur the tech industry. In late 2023, Romania adjusted this to exempt IT salaries up to 10,000 RON (~€2,000) per month – meaning most mid-level programmers still pay zero income tax (since their gross might be under that cap), and higher earners only pay tax on the portion above 10k RON. Social contributions still apply, but this is a significant saving. Bulgaria does not offer a similar tax break for IT workers – all employees pay 10% flat tax. As a result, international tech companies often find Romania’s talent pool not only larger but also effectively tax-subsidized for the employee, enabling competitive net salaries.

R&D and Innovation Tax Incentives

For companies focusing on research, development, or innovation, the tax incentives available can tip the scales. Here Romania has a clear advantage with multiple R&D incentives, while Bulgaria relies mostly on its low tax rates and EU grants rather than special R&D tax breaks.

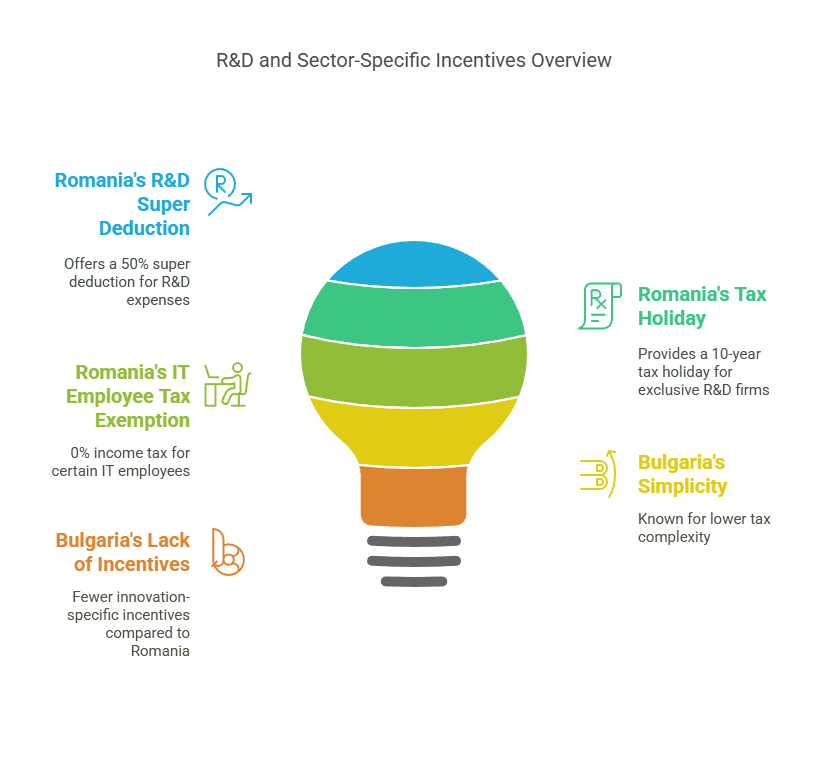

Romania’s R&D Tax Incentives: The Romanian government actively encourages innovation through corporate tax provisions:

Super Deduction for R&D: Companies engaging in qualifying R&D activities can deduct an additional 50% of eligible R&D expenses from their taxable profit, on top of the normal deduction. This effectively means €100 of R&D spend yields €150 deduction, reducing CIT by an extra €8 for every €100 spent (at 16% CIT).

Accelerated Depreciation: Equipment used in R&D can be depreciated faster for tax purposes, allowing companies to defer taxes.

Tax Exemption for Reinvested Profit: Romania offers CIT exemption on profits reinvested in certain technological equipment (e.g. machinery, computers). This is not limited to R&D, but often benefits growing tech and manufacturing firms upgrading their hardware. Essentially, if a company plows its profit into new production technology, that profit can be CIT-free.

10-Year Tax Holiday for R&D Firms: Perhaps the most generous incentive – companies whose exclusive activity is R&D and innovation can qualify for a 10-year corporate tax exemption. This incentive, introduced in recent years, aims to attract R&D centers and startups. In practice, the firm must be truly dedicated to research/innovation activities to qualify (and likely certified by authorities), but it means a pure research lab or tech startup in Romania could go a decade without paying CIT at all.

These incentives make Romania attractive for high-tech industries, pharmaceuticals, software development, and any business with substantial R&D expenditures. For example, a biotech company could get an extra 50% deduction on clinical research costs, lowering its effective tax rate, and if it reinvests profit into lab equipment, those profits aren’t taxed. Romania also has innovation grants and an IT park regime (with local tax benefits) in certain locales, complementing the tax incentives.

Bulgaria’s Tax Incentives: Bulgaria does not have specific R&D credits or super-deductions at the national level. The Tax Foundation notes that Bulgaria’s implied tax subsidy for R&D is negligible, indicating no major special tax breaks. However, Bulgaria offers other incentives:

Regional Investment Incentives: Investors in manufacturing or services in regions with high unemployment can receive a refund or reduction of up to 100% of CIT for a number of years. Essentially, if you invest in a less developed area (setting up a factory or back-office in a poorer region), the government may grant back your corporate tax to reinvest in the project. This can amount to a tax holiday, albeit usually contingent on reinvesting the saved tax in the region and meeting job creation targets.

Hiring Incentives: Bulgarian tax law provides additional deductions or relief for companies that hire long-term unemployed, disabled persons, or those nearing retirement age. These are social policy measures, but they effectively reduce tax for businesses that contribute to employment of vulnerable groups.

Industry-Specific: While not an R&D credit, Bulgaria’s government may offer cash grants or EU-funded incentives for R&D projects through innovation funds or EU programs (Horizon Europe, etc.). Many Bulgarian tech firms benefit from lower operational costs and EU subsidies rather than tax credits.

In summary, Bulgaria’s strategy is “low taxes for all” instead of targeted tax breaks – a tech company pays just 10% CIT on its profits, which is low, but it doesn’t get additional R&D write-offs like in Romania.

Which is better for innovation? For R&D-heavy businesses, Romania’s tax regime is more favorable. A software development subsidiary in Romania could reduce taxable income significantly via the 50% R&D deduction (covering developer salaries and research costs), whereas in Bulgaria the same subsidiary would simply pay the flat 10% on whatever profit remains. If the profit margin is high and R&D spend low, Bulgaria’s lower rate may suffice. But if the company continually invests in new development, Romania might yield a lower effective tax rate after incentives (potentially well under 10%).

Case Example: A multinational opens an R&D center with €2M annual expense and wants to break even. In Romania, that €2M could yield an extra €1M deduction (50%), potentially creating a tax loss to carryforward or shield future profits. In Bulgaria, the €2M is just a normal expense (no extra deduction). Over time, if the R&D leads to IP income, Romania also has R&D parks and is considering IP box regimes (though not yet implemented as of 2025). Companies like Ford and Bosch run R&D operations in Romania, likely taking advantage of such incentives, whereas in Bulgaria companies tend to focus on production and outsourcing where the low 10% tax suffices.

Sector-Specific Tax Benefits (IT, Manufacturing, Startups)

Beyond R&D, certain industries enjoy tailored tax or fiscal benefits in each country:

Information Technology (IT) Sector: Romania has cultivated its IT and outsourcing sector with personal tax exemptions. As mentioned, IT employees meeting certain criteria (job role and education in computer science) are exempt from the 10% income tax on salaries up to a limit. This effectively makes hiring IT talent more cost-effective (employers can offer higher net pay for the same gross). Additionally, Romania has seen the rise of IT hubs (e.g. Cluj-Napoca, Bucharest, Iași) with local incentives and thriving tech ecosystems. Bulgaria, on the other hand, relies on its generally low taxes and labor cost. While Bulgaria doesn’t exempt IT salaries from tax, its average IT wages are slightly lower and the 10% flat tax is still very attractive internationally. Sofia and Plovdiv host many BPO (business process outsourcing) and IT outsourcing centers due to the combination of low tax and skilled workforce. However, on balance, tech startups might lean toward Romania for the tax break on programmers and larger talent pool (Romania has ~150k IT professionals vs Bulgaria’s ~70k). Indeed, Romania produced unicorns like UiPath (RPA software) and Elrond Network (blockchain) in recent years, aided by a supportive tax regime and government grants.

Manufacturing & Industrial: Both countries compete for manufacturing FDI (e.g. auto parts, electronics). Bulgaria’s key advantage is lower wage costs and the possibility of tax-free regions (the CIT refund in high-unemployment areas can effectively eliminate corporate tax for a period if profits are reinvested). For instance, an automotive supplier in northwest Bulgaria (a less developed region) could pay 0% CIT for a number of years if it uses the saved tax to build its factory and train workers – a significant incentive for industrial projects. Romania doesn’t offer regional CIT holidays, but it touts a larger market and infrastructure. Romania is home to large assembly plants (Renault’s Dacia and Ford) and hundreds of automotive suppliers, creating cluster effects. Tax-wise, Romania’s 16% CIT is higher, but profits reinvested in new technology are exempt, which manufacturing firms can utilize to upgrade machinery tax-free. Also, certain industries (e.g. construction, as noted) have payroll tax breaks in Romania which reduce labor costs by waiving income tax and part of contributions until 2028 for companies in building sector. Bulgaria does not have a similar nationwide scheme for construction, though both countries sometimes use reduced VAT for construction materials (temporarily) to stimulate building.

Startups and SMEs: For small startups, Romania’s micro-company regime (1% tax on revenue for many new firms) is a big perk. A tech startup in Romania can pay just 1% of turnover in tax during its early years instead of 16% on profits – if it’s barely breaking even or reinvesting all earnings, that 1% on a small revenue base is negligible. Bulgaria’s 10% tax is low, but a pre-profit startup still pays zero (since CIT is on profit). So if a startup is not profitable initially, neither country taxes it; but if it has small profits or is services-based with low costs, Romania’s 1% of revenue could be lower than Bulgaria’s 10% of profit. Romania also recently introduced a holding company regime (participation exemption on foreign dividends and capital gains) and is considering more startup incentives as part of its Digital Innovation strategy. Bulgaria’s ecosystem benefits from government programs and EU funds but not so much from special tax rules; however, one might argue the simplicity of a flat 10% across all business stages in Bulgaria is easier for startups to plan around.

Others: Both countries have free trade zones where customs duties are eased. Sectorally, Romania had a tax incentive for agriculture (reducing income tax for farmers) and Bulgaria for agri-business CIT (partial CIT forgiveness on certain agricultural income). These are niche but can be relevant for agribusiness investors (e.g. Bulgaria allows 60% of CIT on income from farming to be retained and reinvested). Energy sector investors in Romania should note specific taxes (like a windfall tax on energy producers in 2022–23), whereas Bulgaria’s energy taxation has been more stable. Both countries align with EU rules for renewable energy incentives and subsidies rather than tax breaks.

In sum, sector-based tax benefits are more pronounced in Romania (especially for IT, R&D, construction) whereas Bulgaria’s strategy is broadly low taxes with a few targeted investment incentives (region-based CIT relief, etc.). An investor with a labor-intensive IT/BPO operation might favor Romania for the employee tax savings, while one with a capital-intensive factory might lean towards Bulgaria for the possibility of near-zero tax in a special region and generally lower labor costs.

Regulatory Environment and Ease of Doing Business

Tax advantages alone do not determine a favorable jurisdiction – the regulatory environment, ease of incorporation, and ongoing compliance burden are crucial. Here’s how Romania and Bulgaria compare:

Ease of Incorporation: Both countries allow 100% foreign ownership and have no restrictions on repatriation of profits. Incorporating a limited liability company is relatively quick and inexpensive in each. Romania uses the “SRL” (Societate cu Răspundere Limitată) as the common form, while Bulgaria’s equivalent is the “OOD” ( дружество с ограничена отговорност ). Romania recently eliminated the minimum share capital requirement, which was nominal anyway (previously ~RON 200 ≈ €40). Bulgaria’s minimum capital for an LLC is just BGN 2 (about €1) – essentially no real capital needed. One notable difference: Bulgaria requires non-EU foreign directors to obtain a Bulgarian residence permit to register a company. This can take a few months and adds complexity for, say, an American or British entrepreneur starting a Bulgarian company. Romania, by contrast, imposes no residency requirement for directors or shareholders – a foreign investor can incorporate and appoint non-resident directors without needing local residency. This makes Romania more straightforward for global businesspeople to set up shop. (EU citizens can freely be directors in either country due to freedom of establishment, so this mostly affects investors from outside the EU in Bulgaria.)

Administrative Burden: According to the World Bank’s Ease of Doing Business 2020 report (the last available global ranking), Romania was ranked 55th and Bulgaria 61st out of 190 economies. Both are considered relatively business-friendly, though not top-tier. Romania scores well on starting a business and getting credit, but lags in dealing with construction permits and enforcing contracts. Bulgaria scores well on low taxes (total tax rate for firms) but lower on investor protection and resolving insolvency. Overall, their ease-of-doing-business scores were quite close (Romania 73.3, Bulgaria 72.0), indicating a comparable regulatory climate. Neither country has onerous ongoing corporate compliance: annual financial statements and tax returns are required; Romania mandates an audit once companies grow beyond certain size criteria, as does Bulgaria.

Bureaucracy and Governance: Romania has made strides in reducing red tape – for example, online filing systems (e-guvernare) for taxes and a one-stop-shop Trade Registry service for company formation. Still, investors sometimes face frequent legislative changes and inconsistent enforcement. The U.S. Department of State noted that while Romania “offers a well-educated workforce and large market,” bureaucratic procedures and frequent regulatory changes can weigh on the business climate. Bulgaria, in some respects, offers more regulatory stability (fewer sudden tax changes), but it has its own challenges, such as perceived corruption in public procurement and lower judicial efficiency in commercial disputes. Transparency International’s corruption index tends to rate both relatively low in the EU (Romania often slightly better than Bulgaria).

Incorporation Time & Costs: Setting up a company in Romania can be done in about 3–5 days if all documents are in order (notarized articles, proof of capital, etc.), whereas in Bulgaria it may take 1–2 weeks including the time to handle any director residency paperwork. Both have low setup costs (a few hundred euros for registration and notary fees). One of Romania’s selling points is the “lack of bureaucracy” for company registration – the process is straightforward and there are services to expedite it. Bulgaria’s process is also relatively simple for EU investors, but the added layer for non-residents is a consideration.

Local Operational Regulations: Both countries being in the EU means compliance with EU standards (e.g. GDPR for data protection, competition law, etc.). Romania tends to be slightly more aligned with EU norms in regulations due to its drive to join Schengen and the OECD, which has prompted reforms. Bulgaria has been improving corporate governance regulations as part of its euro adoption preparation. Labor laws are moderately flexible in both (e.g. easy to hire and fire, relatively low severance requirements compared to Western Europe).

Neither Romania nor Bulgaria poses prohibitive regulatory obstacles – they are in fact often praised as reasonably easy places to do business in Eastern Europe. Romania might edge out for those who want quick setup and a larger domestic market to sell into, while Bulgaria might appeal to those who value stable tax laws and simpler tax administration (given the flat taxes). It’s also noteworthy that English is widely spoken in the business community of both countries, and professional services (lawyers, accountants) with international expertise are readily available in major cities.

EU Membership, Market Access, and Compliance

Since both Romania and Bulgaria are EU members (joined in 2007), they offer investors the benefits of EU market access and legal frameworks:

Single Market Access: A company incorporated in either country can freely passport its goods and services throughout the EU. There are no customs duties on trade between Romania/Bulgaria and other EU states. This is a huge advantage for manufacturers and exporters – e.g., a Bulgarian-made product can be sold across the EU without tariffs. Additionally, both countries participate in EU free trade agreements, so an investor can leverage Bulgaria or Romania as a base to export under EU FTAs globally. For instance, an IT firm in Romania can service clients in Germany or France easily, and a Bulgarian auto-parts maker can ship just-in-time to OEMs in the EU with minimal friction.

EU Tax Directives: As touched upon, both implement the EU Parent-Subsidiary Directive (eliminating withholding tax on intra-group EU dividends), the Interest and Royalties Directive (eliminating WHT on cross-border interest and royalties between associated EU companies), and follow EU rules on VAT (with intra-community supply being zero-rated, etc.). This means corporate structures can be optimized: e.g., a Bulgarian subsidiary paying dividends to an Austrian parent would incur 0% Bulgarian tax under the directive, and similarly in Romania. They also adhere to EU anti-abuse rules (ATAD), so substance requirements and transfer pricing rules are in place to prevent aggressive avoidance.

Currency and Eurozone: Neither Romania nor Bulgaria has adopted the euro yet, but both plan to. Bulgaria’s currency, the lev (BGN), is pegged to the euro at approximately 1.95583 BGN/EUR and Bulgaria is actively working toward eurozone accession (now expected around 2025–2026). Romania’s leu (RON) floats (currently around 4.95 RON/EUR) and Romania aims for euro adoption perhaps by 2026–2027, though no fixed date. For investors, currency stability is a consideration: Bulgaria’s peg provides stability and effectively minimal FX risk with the euro (and eventual adoption will remove currency risk entirely). Romania’s leu has been relatively stable but does gradually depreciate; however, operating in RON offers flexibility and the central bank keeps inflation in check. Once both join the euro, this difference fades.

EU Funding and Grants: As EU members, both countries receive substantial development funds. Investors can benefit indirectly through improved infrastructure and directly via grants for investments (especially in sectors like manufacturing, R&D, green energy). For example, an investor in Romania might tap EU co-financing for a factory in an industrial park; in Bulgaria, an IT company might get EU-funded training grants for its staff. The availability of such funds is comparable, though Romania’s larger size means a bigger absolute envelope of EU funds.

Compliance with EU Regulations: Being in the EU also means robust regulatory frameworks: competition law (antitrust) is EU-harmonized, environmental regulations must be met by factories, data protection (GDPR) is strictly enforced for any business handling personal data, etc. Both countries have had to raise their standards over the past decade, which gives foreign investors a level of confidence in legal protections (e.g., IP rights enforcement, though challenges remain).

Schengen Area: A side note on logistics – neither Romania nor Bulgaria is yet in the Schengen passport-free zone. They are EU members but as of 2025, border checks still exist when transporting goods to/from some neighboring EU countries. This is more of a nuisance than a major barrier, and it’s expected they will eventually join Schengen, which will streamline cross-border transport further. Even now, both countries’ ports (Constanța in RO, Varna/Burgas in BG) and Danube river transport give strategic access to Black Sea and European markets.

In essence, choosing Romania or Bulgaria gives investors a platform inside the European Union’s huge market. There is little difference between them in terms of EU single market benefits – both comply with EU standards and allow firms to plug into European supply chains. One could say Romania’s market of 19 million is itself an EU market advantage (for consumer goods companies, Romania offers a larger customer base), whereas Bulgaria’s local market is only 7 million, but many companies in Bulgaria produce almost exclusively for export (for example, 70% of Bulgarian IT companies export their services abroad). So, if market proximity is a priority (e.g. selling in Central/Eastern Europe), Romania’s location and size might be better; if pure EU access with lowest costs is key, Bulgaria might suffice as a gateway.

Real-World Examples and Case Scenarios

To illustrate how these differences play out, let’s consider a few scenarios of international companies choosing Romania or Bulgaria:

Tech Outsourcing Company: A U.S. software development firm is deciding between Sofia (BG) and Cluj-Napoca (RO) for a 100-person development center. Tax factors: In Romania, it could benefit from the IT salary tax exemption, meaning many of its developers would pay 0% income tax, which helps attract talent or reduce salary costs. The firm’s profits could potentially qualify for the 10-year R&D tax holiday if it operates as a standalone R&D entity. In Bulgaria, the firm enjoys a flat 10% tax on profits and 10% on all salaries – simple and low. Outcome: If the key driver is talent availability and incentives for innovation, Romania might be chosen – indeed companies like Microsoft, Oracle, Amazon, and IBM have large tech centers in Romania’s cities, leveraging the skilled workforce and tax breaks. On the other hand, companies like HP, SAP, and IBM also have significant operations in Bulgaria, attracted by the 10% flat tax and lower wage level for BPO functions. A likely strategy is to use Romania for higher-end R&D and product development (to utilize R&D credits and abundant engineers) and Bulgaria for support and outsourcing operations (to take advantage of the ultra-low taxes for a cost-center).

Automotive Manufacturing Plant: A European car parts manufacturer considers expanding production in Eastern Europe. Romania offers proximity to existing big car factories (Renault and Ford are in Romania) and an industrial base of suppliers; Bulgaria offers 10% CIT and the possibility of no tax in a high-unemployment area plus cheaper labor. Tax calculation: Suppose the plant will generate €5M in profits annually. In Bulgaria, CIT would be €0 if the investment meets the criteria for CIT exemption in a designated region (otherwise €0.5M at 10%). In Romania, CIT would be €0.8M at 16%, but the company could get some relief by reinvesting profits into equipment (perhaps saving €0.1–0.2M tax via the reinvested profit exemption). Over a decade, the tax savings in Bulgaria could be substantial. Other factors: Romania’s domestic market for cars is bigger and it has better developed supplier networks; Bulgaria has to import more inputs but it’s improving infrastructure (and both are in the EU, so supply chain flow is okay). Outcome: If the firm highly values the tax holiday and lower recurring costs, it might pick Bulgaria – indeed, many automotive suppliers (wire harnesses, sensors, etc.) have chosen Bulgaria for its cost advantage, contributing to an industry that’s now ~4.5% of Bulgaria’s GDP. If the firm wants to be near major assembly plants or needs a larger pool of engineers, Romania might win (e.g. Continental, Bosch, and Magna have large operations in Romania’s automotive sector, benefiting from both the market size and incentives on R&D and reinvestment).

Holding Company / E-commerce Business: An international entrepreneur wants a European holding company to channel investments or an e-commerce business selling across the EU. Bulgaria’s appeal lies in its 10% tax on retained earnings (if profits aren’t distributed, they accumulate at a low tax cost) and only 5% when paid out as dividends – potentially optimal if the owner wants to take dividends under a treaty or if they redomicile to a low-tax country personally. Romania’s holding regime now exempts foreign dividends if holding >10% for 1 year (so holding foreign subsidiaries is tax-neutral) and capital gains on shares can be exempt similarly. But Romania’s actual tax on domestic profits is 16%, and dividend WHT to a personal owner is rising to 10%. Outcome: For a pure holding or trading vehicle with minimal staff, Bulgaria is often favored simply due to the lower taxes and simplicity. We see many SME online entrepreneurs register companies in Bulgaria to enjoy the 10% rate on global income (sometimes even moving to Bulgaria to become tax resident individuals at 10% flat PIT). Romania might be chosen if the investor plans to also have operations or take advantage of EU-funded programs in Romania. But statistically, Bulgaria has attracted numerous foreign small businesses as a tax-efficient registration jurisdiction for e-commerce, digital services, etc., often mentioned in contexts like “best country to register a company in EU for low taxes” – with Bulgaria and Cyprus frequently topping those lists.

Startup / Innovation Project: Consider a startup developing a new green technology. In Romania, if it qualifies as an R&D startup, it could potentially incubate in an innovation hub and enjoy the 10-year CIT exemption. It could also apply for grants from Romania’s Start-up Nation program or EU structural funds targeted at Romania. In Bulgaria, the startup would pay 10% on any profit (likely none in early years) and could seek funds from sources like the Bulgarian Innovation Fund or EU programs; there’s no tax holiday but the burden is low anyway if profits are low. Outcome: If expecting to be profit-making quickly, Romania’s tax holiday is extremely valuable (0% tax for 10 years is a huge boost to reinvest in growth). If not, both jurisdictions offer a low-cost base, but Romania’s ecosystem (especially in cities like Bucharest, Cluj) is larger and may offer more networking and financing opportunities. That said, Bulgaria’s capital Sofia has a vibrant startup scene too, with several success stories (e.g. Telerik, a software company acquired by Progress Software, started in Bulgaria). Tax-wise it’s a draw for very early-stage (no profit) startups, but Romania’s incentives might yield benefits down the line.

These examples show that the “best” choice can vary by industry and business model. Companies often strategically use both countries – for instance, a firm might incorporate a Romanian entity to leverage a particular incentive and a Bulgarian entity to benefit from the low flat tax, forming a group structure that optimizes both. Fortunately, the two countries are reasonably close geographically and both in the EU, so a dual-presence is not uncommon for larger investors in the Balkans region.

Conclusion: Which Jurisdiction is Better?

Romania vs Bulgaria – which offers better overall benefits? The answer depends on an investor’s priorities and the nature of the business:

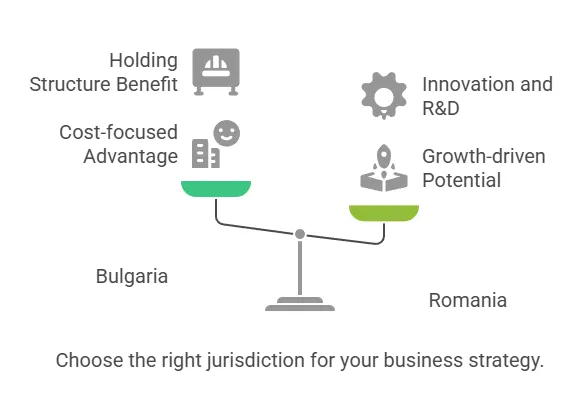

If your top priority is ultra-low tax rates and cost minimization, Bulgaria has the clear edge with its 10% corporate tax and 5% dividend tax. This consistently low tax regime benefits profit-generating companies and holding structures, especially if you plan to reinvest profits globally or eventually distribute dividends to non-EU shareholders. Bulgaria is often the choice for tax-efficient corporate structures in the EU and appeals to businesses like trading companies, outsourcing providers, and holding companies primarily seeking a low-tax jurisdiction.

If you value a larger market, generous incentives, and robust workforce for growth, Romania may offer superior advantages. Romania’s economy (GDP ~€355 billion vs Bulgaria’s €64 billion) and population provide a bigger domestic sales opportunity. Its tax system, while higher in headline rates, offers targeted tax breaks (micro-company 1% tax, R&D deductions, 0% tax for IT employees, etc.) that can outweigh Bulgaria’s low flat tax in specific scenarios. Investors focused on technology, innovation, or high value-add manufacturing might find Romania’s incentives and skilled labor pool lead to better net outcomes. Additionally, the simpler incorporation (no director residency requirement) and faster bureaucratic processes in Romania can be a deciding factor for entrepreneurs who need to get operational quickly.

Labor-intensive businesses and cost-sensitive manufacturing might lean towards Bulgaria due to its lower wage base and moderate social contributions. Over time, total labor costs can be lower in Bulgaria even if employer social tax is higher, because gross salaries themselves tend to be 20–30% lower than in Romania for similar roles. However, Romania’s recent tax changes shifting burden to employees mean that employer’s marginal cost for each additional employee is very low (just ~2.25% on top of salary), which can encourage hiring in Romania as well. If labor availability and skill are key, Romania (with nearly 3 times Bulgaria’s population) offers a deeper talent pool in absolute terms, which can be crucial for larger operations.

Regulatory and stability considerations: Both countries are relatively stable and improving in governance. If an investor is wary of frequent tax law changes, note that Romania has made a number of tax tweaks (e.g. dividend tax from 5% to 8% to 10% in a short span, micro-regime thresholds changing, etc.), whereas Bulgaria’s tax policy has remained virtually unchanged for over a decade (10% flat tax since 2007). In that sense, Bulgaria offers more predictability in tax planning. On the other hand, Romania’s legal system has seen significant reforms and is aligning with OECD standards, which may give more confidence for rule-of-law long-term (Romania has prosecuted high-level corruption in recent years, improving transparency, whereas investors sometimes voice concerns about corruption in Bulgaria as well).

Geography and logistics: If your business benefits from a strategic location, consider that Romania borders five countries and has a coastline, acting as a hub between Central Europe, the Balkans, and the Black Sea – useful for logistics and reaching 19 million local consumers. Bulgaria’s location is slightly further south, with access to the Black Sea and crossroads to Turkey and Greece, which is advantageous for certain trade routes. Both are improving highways and rail, but Romania’s larger size means internal infrastructure investment is ongoing (which can mean future opportunities and also current challenges in some regions).

Both Romania and Bulgaria are low-tax, investment-friendly EU jurisdictions, but they cater to different strategies:

Choose Bulgaria for simplicity and lowest taxes – ideal for companies prioritizing tax savings, relatively smaller operations, or those serving wider markets where local market size is less important. Bulgaria shines for holding companies, outsourcing outfits, and manufacturers focusing on cost efficiency.

Choose Romania for growth-oriented incentives and market potential – ideal for firms that will reinvest, innovate, or sell into a sizable market. Romania is compelling for tech R&D centers, regional headquarters aiming to tap Eastern Europe, and any business that can utilize its tax credits and skilled workforce to drive growth (even if it means a slightly higher tax rate on residual profits).

Ultimately, an investor’s specific situation (industry, profit margins, growth plans, and personal residency/tax situation) will determine which jurisdiction offers “better overall benefits.” Some may even utilize both: for example, setting up a Bulgarian entity for certain activities and a Romanian entity for others, to capitalize on each country’s strengths. With both countries continuing to modernize and integrate into the EU economy, investors can expect competitive tax regimes and improving business conditions in Romania and Bulgaria alike. Conducting thorough due diligence with local tax advisors and leveraging the available incentives can ensure you make the most of whichever jurisdiction (or combination thereof) you choose for your corporate investment in Eastern Europe.