Relocating can open the door to better financing opportunities. Certain countries – especially global financial hubs – offer expats easier access to mortgages, business loans, and insurance, provided you attain legal residency or citizenship status. In this comparative guide, we’ll analyze top expat-friendly financial hubs and how being a resident or citizen there can lead to favorable loan terms, insurance premiums, and overall financial inclusion. Key factors include expat mortgage eligibility, interest rates, insurance access, banking stability, and the residency/citizenship pathways to unlock these benefits. Investors, entrepreneurs, professionals, and remote workers seeking stronger financial footing through relocation will find this data-driven comparison useful.

Comparative Table: Insurance Benefits & Premiums for Expats

| Country | Health Insurance for Expats | Annual Premium (Individual) | Other Insurance & Notes |

|---|---|---|---|

| United Kingdom | Access to NHS for all residents (free at point of use) Many expats don’t need private insurance for basic care. | ~$4,000 for a comprehensive private plan (if desired)– otherwise $0 for NHS coverage. | Ample private options (BUPA, etc.) if one prefers private hospitals. Life & Property: Readily available at standard rates. Car insurance required by law, moderate cost. Strong legal protections for policyholders. |

| Switzerland | Mandatory private health insurance for all residents (standard basic coverage by insurers, community-rated). High-quality care, but no free healthcare. | ~$4,500–6,000 for basic annual premium (adult) – varies by canton/age. International plans often not needed due to excellent local coverage. | Health: No employer subsidy – individual must purchase insurance, though employers often pay part of premiums as benefit. Life insurance: common for mortgage collateral. Property: home insurance often mandatory for fire; low crime keeps premiums low. |

| Singapore | No universal healthcare for expats. Employers usually provide group health insurance. Expats often buy international health plans for wider coverage. | ~$7,000 (average int’l plan) Basic local plans can be cheaper if covering only Singapore. | Health: Government clinics are affordable out-of-pocket for minor needs, but hospitalization can be pricey without insurance. Other: Car insurance costly (due to high car values), travel insurance popular given regional travel. Strong regulatory oversight via MAS ensures insurer reliability. |

| UAE (Dubai) | Mandatory health insurance – employers must provide a base level plan for employees (and often dependents). Expats can top up for better coverage. | ~$5,700 (int’l family plan) basic employer plans are often ~$1,000 per person (paid by employer). | Health: Large network of private hospitals, direct billing widely available. Other: Third-party liability car insurance is mandatory; premiums around $400–$800/yr for average vehicles. Housing contents insurance is optional but inexpensive. No social security system for expats, so many opt for private life and disability cover. |

| United States | No automatic coverage – health insurance is a must. Most expats get an employer plan or buy via ACA marketplace. Without insurance, medical costs are prohibitive. | ~$9,800 (avg. premium) if self-paying comprehensive plan. Employer-sponsored plans vary, with employees often paying ~$1,500–3,000 of the premium. | Health: Plans often have deductibles ($1k+). It’s the most complex aspect of US expat life. Other: Insurance market is highly developed – you can insure virtually anything. Auto insurance ~$1,000/yr on average (varies by state). Umbrella liability policies common for high-net-worth individuals. Federal deposit insurance (FDIC) on banks adds a layer of security for cash holdings. |

| Portugal | National Health Service (SNS) provides public healthcare to residents at minimal cost (small co-pays). Expats with residency can access it. Many still get private insurance to avoid wait times. | ~$1,500–2,000 for a robust private plan (age 30s). Public system itself is tax-funded (no premium). | Health: Public hospitals generally good, but non-Portuguese speakers may prefer private care. Other: Car insurance is mandatory (Portugal has among EU’s higher accident rates, so premiums ~$300–500/yr). Home insurance required with mortgages. Overall insurance costs in Portugal are lower than in high-cost hubs, reflecting lower living costs. |

Notes: Annual premiums are in USD for rough comparison and assume an individual mid-30s on a comprehensive plan. Actual costs vary by coverage level. “Public healthcare” indicates government-provided services available to expat residents (often requiring registration). Each country has nuances – e.g. UAE and Singapore rely entirely on private insurance markets, whereas UK and Portugal offer public care which greatly reduces expenses. Insurance regulators in all these countries ensure policyholder protections, but always review what expat policies cover (especially for medical evacuation or treatment back home).

Comparative Table: Financial Accessibility for Expats (Loans & Credit)

| Country | Mortgage Rates (Typical) | Max LTV for Expats | Expat Business Loan Access |

|---|---|---|---|

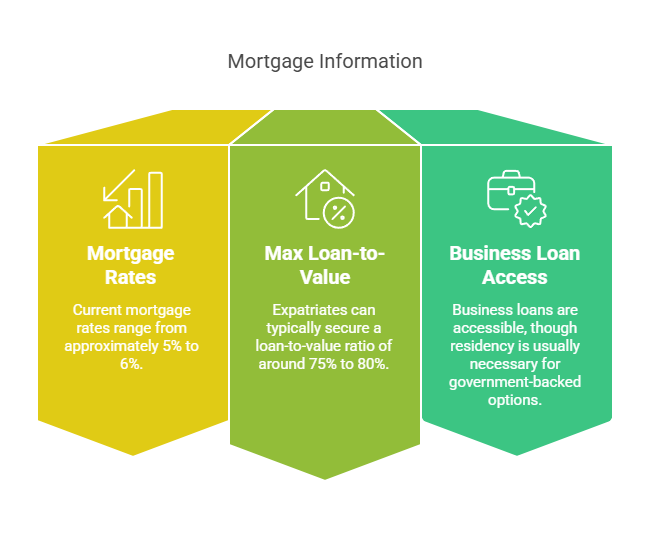

| United Kingdom | ~5–6% (fixed) in 2023 was ~2% in low-rate era. | ~75%–80% (with stable UK income). Some expat-investor mortgages at 60–70% LTV. | Yes – Expats on visas can get loans. Government schemes (e.g. Startup loans) generally require UK residency. Strong credit system; building a UK credit score is essential for good terms. |

| Switzerland | ~1.0–2.0% (fixed) – extremely low by global standards | 80% (standard for all, citizens and expats) – 20% down payment required. | Yes – Local banks lend to companies with Swiss presence. No special expat restrictions beyond usual collateral requirements. Government SME loans exist but often not targeted by nationality. |

| Singapore | ~3.5–4% (fixed) currently < 2% in prior years. | 75% if first property and financially qualified (applies similarly to PRs/foreigners for loan, but foreigners pay 60% tax on purchase). PRs pay only 5% on first home | Yes (with caveats) – Banks lend to expat-owned businesses, but gov’t-backed loans require ≥30% local/PR ownership Expats often seek PR or local partners to fully access business financing. |

| UAE (Dubai) | ~4% (fixed) on new mortgages ;varies with EIBOR. | 80% for expat residents (first property) 50% for non-resident foreign buyers | Yes – Need a UAE trade license and local operations. Local banks require track record; new foreign-owned SMEs may rely on personal funds or investor networks initially. Government funds mostly for Emiratis, but new startup incubators offer financing to expats. |

| United States | ~5–7% (30-yr fixed) as of 2025; historically ~3–4% in 2010s. | 80% typical (< =95% with FHA/VA for residents). Foreign non-residents ~70% LTV with specialized programs. | Yes – Vast options. SBA loans require 51%+ ownership by US resident/citizen Plenty of private and venture funding available. Building US credit score (FICO) is key to accessing cheap credit. |

| Portugal | ~3–4% (variable) in euro terms (Euribor + margin); was ~1% during ECB low-rate period | ~80% for fiscal residents; 65–75% for non-resident foreigners (banks prefer larger down payment if you don’t live/work in Portugal). | Yes – Local banks actively work with expat entrepreneurs. No citizenship requirement for loans, but having residency (NIF number, local address) makes process smoother. EU funding programs available for businesses, accessible to residents. |

Notes: Interest rates are approximate and subject to change with market conditions. “Max LTV” = maximum loan-to-value mortgage allowed. Expats should maintain local bank accounts and credit lines to build history. In all hubs, having a long-term residency status improves banks’ willingness to lend, as it signals commitment to the country.

Many banks require minimum balances to avoid fees or to qualify for certain benefits, which expats should consider when choosing a financial institution.

United Kingdom – Global Finance with Public Healthcare

Expat Loan Access: The UK is a premier financial center (London) with a mature banking sector. Expats on work visas or with permanent residency (Indefinite Leave to Remain) can typically obtain mortgages similar to locals. Lenders often approve up to ~75%–80% loan-to-value for qualified buyers, and there’s a robust market of “expat mortgages” even for non-residents (usually requiring larger down payments). In 2023, UK mortgage rates spiked – a 2-year fixed rate (75% LTV) peaked around 6.44% due to Bank of England hikes, with standard variable rates averaging 8.74%. While high by UK standards, expats with solid UK income or credit can still access financing. Business loans are available through local banks; however, some government-backed loans (like startup loans) may require residency. Overall credit accessibility is high – the UK uses credit scores, but newcomers can build credit quickly by maintaining UK bank accounts and credit cards. Additionally, many UK banks have minimum balance requirements for certain accounts, which expats should be aware of to avoid monthly service fees.

Insurance and Banking Stability: A major perk of UK residency is access to the National Health Service (NHS) – all residents (including expats) enjoy free or low-cost healthcare. This drastically lowers the need for private health insurance – a comprehensive private plan averages about $4,000 yearly, far less than in many countries. Life and property insurance is easy to obtain at standard rates, and many employers offer group plans. The UK has a very stable banking system with strict regulation. Deposits are protected up to £85,000 per person by the Financial Services Compensation Scheme (~$105,000), ensuring peace of mind. Financial services are well-developed – expats can open bank accounts, transfer money freely, and enjoy world-class fintech services in the UK’s open market. Dual citizenship is recognized here; the UK allows British nationals to hold other nationalities.

Residency & Citizenship Options:

Skilled Worker Visa: For those with a job offer in the UK meeting salary and skill requirements. Typically valid 5 years, leading to permanent residency (ILR).

Innovator & Startup Visas: For entrepreneurs investing in a UK business (used to require ~£50k investment; now an endorsement-based system). Can also lead to ILR in ~3 years if business meets criteria.

Investor Visa (Closed): The Tier 1 Investor visa (required £2 million) is suspended as of 2022, but alternative routes exist for high-value migrants (e.g. Global Talent Visa for highly skilled individuals, or Ancestry Visa for those with UK-born grandparents).

Permanent Residency (ILR): Achieved after 5 years on most work visas. ILR grants almost all rights of a citizen.

Citizenship: Eligible 1 year after ILR (so ~6 years total). The UK allows dual citizenship, so expats can naturalize as British without renouncing their original citizenship, making it attractive for those seeking a second passport.

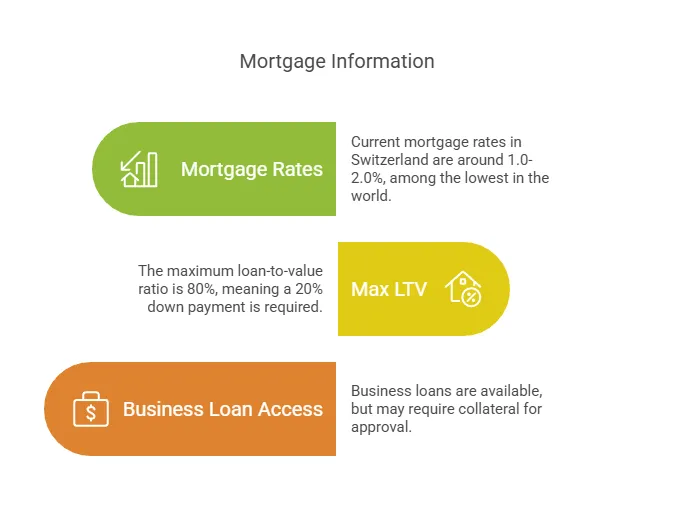

Switzerland – Stable Banks, Offshore Banking, and Low Rates for Residents

Expat Loan Access: Switzerland consistently ranks as a top expat destination for finance, known for banking stability and ultra-low interest rates. Foreign residents (with a B or C residence permit) can access Swiss mortgages, which feature some of the lowest interest rates globally. Even after recent rate adjustments, 10-year fixed mortgage rates average only ~1.13% in late 2024, and variable rates ~1.6–2.3%. These cheap loans make home financing very attractive if you live and work in Switzerland. Banks generally require at least 20% down payment (80% LTV max) from anyone – citizen or expat – ensuring borrowers have skin in the game. Expats may face property purchase restrictions if not from the EU (the Lex Koller law limits non-resident foreigners to certain properties), but as a legal resident you can buy a primary residence relatively easily. Business loans and credit lines are available to expat entrepreneurs who establish a Swiss company, though conservative Swiss lending means you often need solid collateral or finances. That said, Switzerland’s pro-business environment and wealth management expertise provide financing avenues for expats with means.

Insurance and Banking Stability: All Swiss residents must obtain health insurance from private insurers within 3 months of arrival – there’s no free national healthcare, but the system ensures everyone is covered by a basic plan. The average basic premium is about CHF 300–500 per month (≈$4,000–$6,000 annually), depending on age and canton. This guarantees access to Switzerland’s high-quality healthcare. Many expats supplement with private add-ons for wider coverage, but overall medical care is comprehensive. Notably, international health insurance costs for expats in Switzerland are lower than in many hubs – Switzerland didn’t even appear in the top 5 most expensive countries in a 2023 survey (Hong Kong and Singapore were much higher). Beyond health, insurance for life, property, and vehicles is readily available; Switzerland even has mandatory liability insurance for certain cases, reflecting its risk-averse culture. The banking system here is legendary for its stability and security – Swiss banks are heavily regulated and well-capitalized. Deposit protection covers up to CHF 100,000 (~$110k) per depositor. Expats often praise the peace of mind of keeping money in Swiss banks (which famously prioritize confidentiality and prudence). For those interested in investments, opening a brokerage account in Switzerland can provide access to a wide range of financial products and services. There are no currency controls, making it easy to move funds. Overall, Switzerland offers a secure financial environment for expats. And importantly, it permits dual citizenship without restriction since 1992, so if you naturalize as Swiss you can keep your original nationality.

Residency & Citizenship Options:

Work Permit (B Permit): Non-EU nationals need an employer-sponsored permit (quotas apply). EU/EFTA nationals have easier access via free movement. After 5–10 years of continuous residence (depending on nationality and integration level), one can obtain a C Permit (permanent residency).

Investor and Retiree Residency: Switzerland has no official “golden visa,” but wealthy individuals may negotiate cantonal residency by paying an annual lump-sum tax (often CHF 150k+). Retirees over 55 with sufficient assets can sometimes qualify for residence under this scheme as well.

Entrepreneur Visa: If you start a company that creates local jobs, authorities may grant a residence permit (case-by-case for non-EU investors). Typically, proving significant economic benefit or investing substantial capital is required.

Citizenship: Eligible after 10 years of residency (time on certain permits counts, and years between ages 8–18 count double). Must demonstrate integration (including language proficiency in a national language and community involvement). Switzerland allows dual citizenship, so expats can naturalize without losing their original passport. The citizenship process is federal + cantonal + communal, meaning you’ll need approval at all three levels, which underscores the importance of local integration.

Singapore – Asia’s Expat Finance Powerhouse (Residency Key, Foreign Transaction Fees)

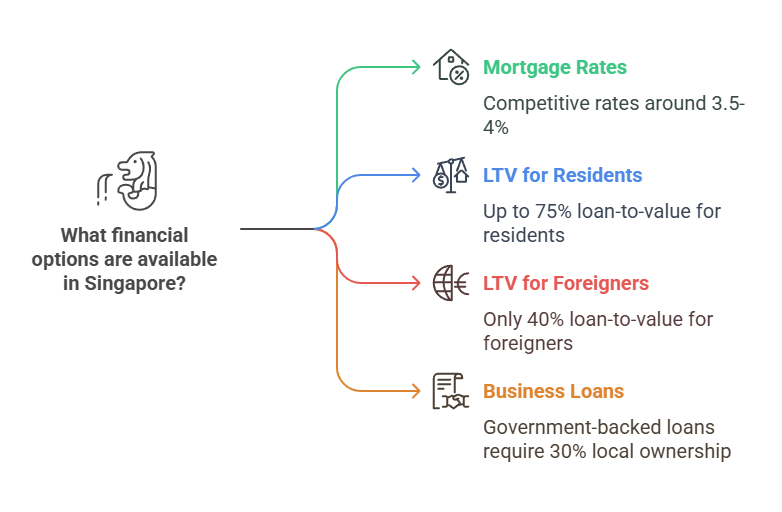

Expat Loan Access: Singapore is a top financial hub with modern banks and a credit-friendly environment – if you’re a resident. Expats can get mortgages for private property, but Singapore differentiates heavily between citizens, permanent residents (PRs), and foreign buyers. Permanent Residents have a big advantage: PRs enjoy up to ~75% LTV on home loans and pay only 5% Additional Buyer’s Stamp Duty on a first property. In contrast, foreigners without PR status face steep barriers – notably a massive 60% stamp duty on any residential purchase (raised in 2023 to cool the market). That means a foreigner buying a $1M condo would pay an extra $600k in tax, which is prohibitive. This policy drives many expats to seek PR before buying property. Interest rates in Singapore have risen from the ultra-low < 2% levels of a few years ago: as of mid-2023, local mortgage rates hover ~3.65–3.75% for 2-year fixed packages. These rates are still moderate and competitive. Expats with valid work passes can apply for loans, but banks will look at your employment stability and may be slightly more conservative if you’re on a shorter-term visa. On the business side, Singapore aggressively supports SMEs – but government-backed SME loans require local participation. The Enterprise Financing Scheme, for example, mandates at least 30% local (Singaporean/PR) shareholding for a company to qualify. This means expat entrepreneurs are wise to either take up PR or partner with a local to access low-interest SME loans and grants. Private financing and venture funding are also plentiful in Singapore’s startup ecosystem, so expats do have funding avenues. Overall, attaining PR unlocks the full suite of Singapore’s affordable financing (from home loans to business capital).

Insurance and Banking Stability: Singapore boasts an advanced insurance industry and world-class healthcare, but expats should budget for private coverage. Locals enjoy Medisave and other subsidies, but foreign residents do not get automatic free healthcare. Most expats are covered via employer-provided health insurance or purchase international plans. Costs can be high – Singapore was ranked the 3rd most expensive country for expat health insurance in 2023, with an average annual premium around $7,028. (Routine local plans can be cheaper; this figure reflects comprehensive international coverage.) Despite the cost, the quality of medical care is excellent. Other insurance: car insurance, renters insurance, etc., are easily available and priced competitively, though owning a car is famously expensive for other reasons (COE taxes). The banking sector in Singapore is extremely robust and tightly regulated by the Monetary Authority of Singapore (MAS). Singapore’s banks are among the safest in Asia; there is deposit insurance up to S$75,000–100,000 per depositor (about US$55k–$74k). Financial stability is a hallmark – Singapore often scores top in political stability and low corruption, giving expats confidence in keeping assets here. No capital controls exist, so you can freely remit money in and out. Many banks in Singapore offer benefits for accounts with direct deposit, such as waived fees and early access to funds. Financial inclusion is high: as a work pass holder or PR, you can open accounts, get credit cards, and even invest through local brokerage platforms. One caveat: citizenship in Singapore is restrictive – it’s difficult to obtain and dual citizenship is not allowed. Most expats aim for long-term residency (PR) rather than citizenship, thereby keeping their original passport while still accessing Singapore’s financial benefits.

Residency & Citizenship Options:

Employment Pass (EP): Singapore’s primary work visa for professionals (requires a job offer and minimum salary of S$5,000+ for new applicants, higher for older candidates). Valid 1–2 years and renewable. Similar visas include the S Pass (mid-skilled workers) and EntrePass (for entrepreneurs with innovative startups).

Permanent Residence (PR): After working in Singapore for 6–12 months on an EP, many expats apply for PR. Approval is competitive, considering salary, education, and ties to Singapore. PR is highly sought as it confers benefits (like easier loan access and lower property duties). Note: male PRs are subject to Singapore’s military service if obtained at a young age.

Global Investor Programme (GIP): A residency by investment scheme. Investing S$2.5 million in a new or existing Singapore business, or an approved fund, can qualify an individual (and family) for PR. This is aimed at high-net-worth investors who want to “buy” PR status by driving economic growth.

Citizenship: Eligible after 2 years as a PR, but approval is stringent. One must show deep integration and commitment. Importantly, Singapore requires new citizens to renounce all other citizenships – no dual citizenship allowed. Thus, many expats remain PRs indefinitely rather than give up their original nationality. Those who do naturalize enjoy a powerful passport and full rights (e.g. ability to buy subsidized public housing), but it’s a profound decision due to the exclusivity of Singaporean citizenship.

United Arab Emirates – Opportunity Hub with Evolving Residency and Minimum Balance Requirements

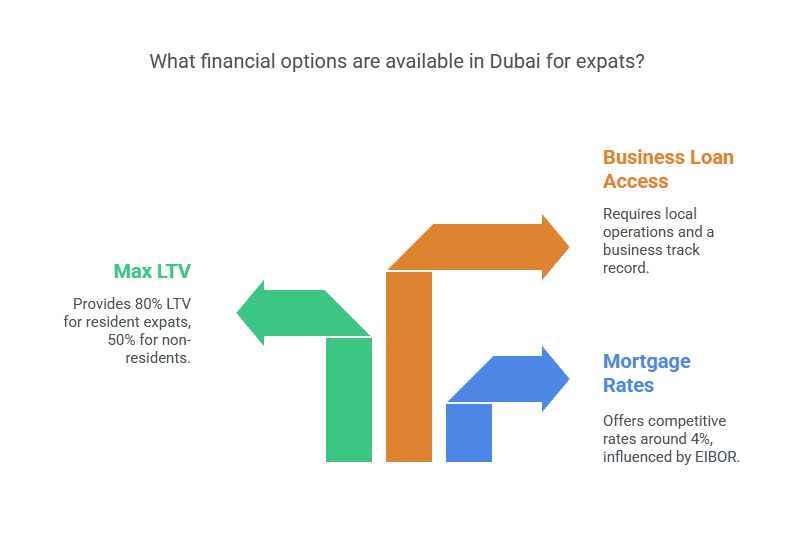

Expat Loan Access: The UAE (notably Dubai and Abu Dhabi) has emerged as a magnet for expat investors and entrepreneurs, with a rapidly maturing financial sector. Traditionally, expatriates in the UAE faced limitations on financing – but recent reforms have improved access. Expats who are UAE residents (holding a residence visa and Emirates ID) can obtain local mortgages for property in designated freehold areas. Banks typically offer up to 80% LTV for expat residents, compared to 85% for UAE nationals. Non-resident foreign buyers can also get mortgages, but usually only up to 50% LTV and often at slightly higher interest rates or with more conditions. As a result, becoming a resident (via work or an investor visa) significantly boosts your borrowing capacity for real estate. Mortgage interest rates in the UAE are competitive; many banks offer fixed rates around ~4% in the current climate. For example, one large bank advertises 3-year fixed home loans at 3.99%–4.24%. Rates are often pegged to the Emirates Interbank Offered Rate (EIBOR) plus a margin. Because the UAE dirham is pegged to the US dollar, rate trends follow the U.S. – in 2023 rates rose to ~5%+ at times as the Fed tightened, but they remain moderate. Expats will need proof of income in the UAE and typically salary transfer to the lending bank to get the best rates (many banks offer rate discounts if you credit your monthly salary to an account with them). On the business financing side, the UAE has historically required local sponsorship for companies, but as of recent years 100% foreign ownership is allowed in many sectors. Banks do provide business loans to expat-owned companies, though they may require a few years of financial statements or personal guarantees. Government programs for SMEs (like the Khalifa Fund) exist but are largely aimed at Emirati-owned businesses. Still, free zones and new startup ecosystems in Dubai offer alternative funding (venture capital, etc.). Overall, the UAE is making strides in expat credit inclusion – once you’ve established residency and local banking history, loan access is quite feasible.

Insurance and Banking Stability: The UAE offers a mixed insurance environment. There is no universal healthcare for expatriates – instead, health insurance is mandatory for residents (employers are required to provide it in Dubai and Abu Dhabi). This means most expats have private health coverage partially or fully paid by their employer. The cost of health insurance in the UAE is high by global standards (ranked 4th most expensive country): an average expat premium runs about $5,687 per year for a comprehensive plan. However, many basic employer plans are less expensive with limited coverage. It’s important for expats to have insurance, as healthcare is mostly private (except emergency stabilization and some public hospitals in Abu Dhabi). Aside from health, other insurance products – car, property, life – are widely available from both local and international insurers. Premiums can vary; car insurance, for instance, is often around 1.5–2% of the car’s value annually for full coverage, and property insurance is relatively affordable (the UAE has no income or property tax, which helps offset such costs). Banking stability in the UAE is generally strong: the major banks (e.g. Emirates NBD, First Abu Dhabi Bank) are well-capitalized, and the government has a record of backstopping banks (as seen during the 2009 crisis). One caveat: the UAE does not yet have an official deposit insurance scheme guaranteeing customer deposits. In practice, the government has intervened to protect depositors in times of crisis, and plans for a formal deposit guarantee framework have been discussed. Despite the lack of a formal FDIC-style guarantee, expats usually trust the system given the UAE’s wealth and support of its banking sector. The dirham’s USD peg also provides currency stability. Moreover, the UAE is a dollarized environment (many expats hold accounts in USD and AED interchangeably), and free flow of capital is allowed (no exchange controls). Overall, the UAE’s financial infrastructure is modern – expats can quickly open bank accounts and use advanced digital banking services. Just be mindful that dual citizenship is generally not available – the UAE only grants citizenship in very rare cases, and while it has started allowing dual nationality for those select cases, for most expats the realistic goal is long-term residency, not Emirati citizenship.

Residency & Citizenship Options:

Work Visa (Residence Visa): Secured via employment in the UAE. This is the most common route – your employer sponsors your residence visa (usually 2–3 years, renewable). It also allows you to sponsor family dependents. Holding a work residence visa is sufficient to access local financing and insurance as described.

Investor & Property Visas: The UAE offers Golden Visas for long-term residency. For example, a 10-year Golden Visa can be obtained by purchasing property worth at least AED 2 million (~$540k), or by investing in/startup a business meeting certain criteria (e.g. a startup generating AED 1M revenue, or being a recognized exceptional talent). There’s also a 5-year property investor visa (usually for a ~AED 5 million investment). These visas are not citizenship but grant stability – crucially, they are renewable long-term residencies that make expats feel secure in planting financial roots.

Freelancer/Remote Work Visas: The UAE introduced a remote work visa (1-year permit) and Green Visa (5-year residency for freelancers or self-sponsored professionals) to attract digital nomads and entrepreneurs. While these confer residency status (and thus access to local banks and insurance), they require proof of sufficient income (e.g. ~$3,500/month for the remote work visa).

Citizenship: Naturalization is extremely uncommon. The UAE only grants citizenship by invitation – recently, laws changed to allow selected investors, scientists, and talented individuals to be nominated for UAE citizenship. In such cases, the UAE may allow dual citizenship (a new development). However, for the vast majority, UAE citizenship is not attainable and not necessary for enjoying financial benefits. A long-term residence (via work or Golden Visa) is the practical end-goal for expats, providing many of the advantages of citizenship (except voting rights) without needing to renounce original citizenship.

United States – Immense Financing Opportunities (for Green Card Holders)

Expat Loan Access: The United States is the world’s largest economy and financial system – expats who establish legal residency find nearly unlimited financing options. U.S. banks and lenders are open to granting mortgages to foreign nationals, but residency status makes a big difference. If you become a U.S. permanent resident (Green Card holder) or even hold a long-term work visa (like H-1B), you can usually access home loans on similar terms as U.S. citizens. Down payments can be as low as 5–10% for residents with good credit (some federal programs like FHA loans allow 3.5% down for permanent residents). Non-resident foreigners can still buy U.S. property, but often need around 30% down and may face higher rates or extra documentation. Interest rates in the U.S. depend on credit scores and market conditions – as of early 2025, mortgage rates are around 5–7% for 30-year fixed loans (having risen with Federal Reserve rate hikes). Expats will need to build a U.S. credit history to get prime rates; this can be done in a year or two by using credit cards and paying on time. The scale of U.S. credit markets means expats with status can also access auto loans, personal loans, and credit lines readily. For entrepreneurs, the U.S. has a plethora of financing: venture capital, private lenders, and bank small-business loans. The key is often immigration status – notably, SBA loans (Small Business Administration) require that at least 51% of the business is owned by U.S. citizens or permanent residents. In other words, an expat entrepreneur really benefits from having a Green Card or citizen partner to tap low-interest SBA financing. Absent that, plenty of private funding is still available, though possibly at higher interest. Overall, the U.S. offers expats the chance to leverage an incredibly dynamic credit market – once you’ve navigated the initial hurdle of establishing U.S. residency and creditworthiness, financing for homes or business ventures is among the most accessible in the world.

Insurance and Banking Stability: The U.S. is a bit of a paradox for expats on insurance. On one hand, it has arguably the best-developed insurance industry with abundant choices; on the other, health insurance in the U.S. is notoriously expensive and complicated. Unlike many countries, there is no universal healthcare for residents. Expats with jobs will typically get employer-sponsored health insurance, which is vital given that the USA has the highest average expat health insurance premiums globally at about $9,817 per year. If you’re not covered by an employer, private individual plans can be costly, though the Affordable Care Act exchanges do offer plans (pricing varies by state and income). Despite the cost, high-quality care is available – many expats budget for a global health plan that includes U.S. coverage due to the steep medical fees. Other types of insurance – auto, home, liability – are widely available and usually reasonably priced due to the competitive market. For instance, auto insurance might be a few hundred dollars per half-year depending on state and driving record. Life insurance is also easy to obtain as a resident. The banking system is very secure (even with recent high-profile bank mergers, depositors have been protected). Deposits are insured up to $250,000 per depositor at FDIC-insured banks – one of the highest guarantees in the world. Many U.S. banks charge monthly service fees, but these can often be waived with direct deposits or maintaining a minimum balance. Large U.S. banks and credit unions offer full-service banking to expats; opening accounts may require a Social Security Number or ITIN, but even non-residents can open certain accounts (with more effort). Once you have a Green Card or SSN, you can fully participate in the U.S. credit system. Another perk: the U.S. dollar is a global reserve currency, eliminating currency risk for your USD assets. There are no capital controls – you can move money in and out freely, though tax compliance (FATCA, etc.) is important for U.S. persons abroad. In summary, the U.S. offers robust financial stability and insurance options, albeit with a warning that health coverage is a critical consideration (and dual citizenship is allowed, which helps if you plan to keep ties abroad).

Residency & Citizenship Options:

Employment-Based Visas → Green Card: Many expats come to the U.S. on work visas (H-1B specialty worker, L-1 transferee, O-1 extraordinary ability, etc.). These are temporary but can often lead to employer-sponsored permanent residency. For instance, an H-1B worker can have their employer file for a Green Card (PERM process). Having a Green Card (permanent resident status) is key to long-term financial access and is usually attainable in 5–10 years depending on the visa and country of origin (backlogs vary).

Investment Visa (EB-5): The EB-5 Immigrant Investor Program grants a Green Card for a qualifying investment of $1,050,000 (or $800,000 in a high-unemployment or rural area) in a U.S. business that creates 10 jobs. Processing can take a couple of years. It’s a direct path to permanent residency for those who have the capital.

Family Sponsorship: Many expats also obtain residency by marrying a U.S. citizen or through other immediate family relations. Spouse visas (CR1/IR1) or fiancé visas can lead to a Green Card within roughly a year of application.

Citizenship: A Green Card holder can apply for U.S. citizenship after 5 years of residency (3 years if married to a U.S. citizen). The naturalization process requires passing an English and civics test and taking an oath. The U.S. allows dual nationality – it “allows for dual (or multiple) nationality” without requiring renunciation, so you can keep your original citizenship. Becoming a U.S. citizen gives you full rights (voting, federal jobs, etc.) and frees you from immigration constraints. However, it also carries the responsibility of worldwide income tax reporting (the U.S. taxes citizens globally, which is a financial consideration for those who may move around). Many expats find the benefits (a powerful passport, security of status) outweigh the tax compliance burden, but it’s something to be aware of.

Portugal – Affordable Loans, Low Insurance Costs, Tax Free Savings Accounts, and a Fast Track to EU Citizenship

Expat Loan Access: Foreigners face few legal barriers to obtaining loans in Portugal. Expats can qualify for home mortgages much like locals, though non-residents are typically asked to provide a larger down payment – around 30% of the property price (≈70% loan-to-value). By contrast, expats with Portuguese residency may access higher LTV mortgages (up to ~80%) and a wider choice of lenders. Portuguese banks require a Número de Identificação Fiscal (NIF), proof of stable income, and a solid credit history to approve loans. Business loans are available if the expat establishes a local business presence, but banks will scrutinize the business plan and may require collateral or personal guarantees given the higher risk. Opening a savings account in Portugal can help expats manage their finances and save for future investments.

Interest Rates & Credit Accessibility: Mortgage interest rates in Portugal are moderate by EU standards, averaging around 4% for new home loans. Many banks offer expat borrowers rates comparable to those for local residents, provided the applicant’s finances are sound. Credit in Portugal is granted based on income and creditworthiness rather than an international credit score – lenders will closely review your financial stability and history before lending. To build credit as an expat, it helps to open a Portuguese bank account and possibly acquire a local credit card or small loan, using them responsibly. Over time, consistent repayment behavior and maintaining Portuguese accounts will establish a positive credit record, making it easier to access larger financing (for example, a car loan or business credit line) at favorable terms.

Insurance Policies and Premiums: Expats in Portugal enjoy relatively affordable insurance options. Key insurance considerations include:

Health Insurance: While public healthcare is accessible to legal residents, many expats opt for private health insurance for extra coverage. Private plans are generally inexpensive, with basic premiums ranging roughly from €20–50 per month (about $22–55) for a healthy adult – though costs rise with age and comprehensive benefits. International health insurance or travel insurance is required for certain visas (like D7 or D8), but once resident, you can also use the national health service with minimal co-pays.

Home/Property Insurance: Home insurance is mandatory for homeowners in Portugal. A basic homeowner’s policy costs around €80–100 per year, typically covering structural damage from hazards (fire, flood, etc.). Expanded coverage (for valuable contents, liability, or holiday homes) can increase premiums modestly (often starting from €100+ annually). These insurance costs are low compared to many countries, which is a benefit for expats buying property.

Life Insurance: Life insurance is optional but often recommended, especially if you have a Portuguese mortgage (lenders may ask for a policy assignment to cover the loan). Premiums are quite reasonable – averaging €50–100 per year for a basic term policy, depending on age and coverage. This provides financial protection for your family or loan obligations, and expats can obtain coverage similar to locals as long as health requirements are met.

Financial Regulations and Banking Stability: Headquarters of the Banco de Portugal in Lisbon, symbolizing the country’s stable, well-regulated banking sector. Portugal’s banking system is considered stable and is closely regulated by the Banco de Portugal (the central bank) under EU oversight. All banks in Portugal participate in a national deposit insurance scheme that protects depositor funds up to €100,000 per bank (approximately $105,000, offering peace of mind to those holding savings). Expats can open accounts even as non-residents, and Portuguese banks generally do not impose negative interest rates on deposits. The country has strengthened financial supervision in recent years, and major banks are well-capitalized and subject to European Central Bank regulations. This robust regulatory framework ensures a high level of banking security for expats, with low incidences of fraud and strong consumer protections.

Residency and Citizenship Options:

Portugal offers several residency visa pathways for expats, each with its own financial requirements and benefits:

Golden Visa (Investment Residency): A fast-track residency program for non-EU investors. It requires a qualifying investment in Portugal, starting from around €250,000 (for cultural heritage projects) up to €500,000+ in real estate or investment funds. (Note: direct residential real estate investment in high-demand areas has recently been restricted under the Golden Visa.) In return, investors and their immediate family members receive renewable residency permits with minimal stay requirements (about 7 days per year in Portugal) and become eligible for permanent residency or citizenship after five years.

Digital Nomad Visa (D8): A visa tailored for remote workers and freelancers introduced in 2022. Applicants must demonstrate remote employment or business activity outside Portugal and a high monthly income (around four times the Portuguese minimum wage, roughly €3,300–3,500 per month). Proof of income for the past year and savings of at least €10,000 are required as financial security. The D8 visa grants a one-year residency (extendable) or a two-year residence permit, allowing expats to live and work from Portugal tax-resident if they stay >183 days. It can be renewed and can lead to permanent residency and citizenship after five years, similar to other visas.

D7 Visa (Passive Income Visa): A popular route for retirees and entrepreneurs with passive income. Applicants need to show a reliable passive income stream of about €870 per month (indexed to the minimum wage)from sources like pensions, rentals, dividends, or remote work, plus sufficient savings (around €10,000 in funds). The D7 visa leads to a residence permit (initially valid for 2 years, then renewable for 3 years) without any investment requirement. D7 residents must spend the majority of the year in Portugal, and after five years of continuous residency they can apply for permanent residency or citizenship.

Work Permit (Employment Visa): For expats with a job offer in Portugal. A Portuguese employer must sponsor the work visa, and the position may need to be advertised to EU citizens first (labor market test) unless the applicant qualifies as a highly skilled worker. Once approved, the work visa grants a residence permit tied to the employment. No specific investment is required aside from gainful employment, but the expat should earn at least the Portuguese minimum wage (often higher for specialized roles or the EU Blue Card scheme). After 5 years of working and legally residing in Portugal, expats can typically apply for permanent residence and eventually citizenship, just as with the other visa categories.

Citizenship: Portugal’s citizenship laws are very favorable for expats. The country allows dual citizenship, so you can retain your original nationality while holding a Portuguese passport. Foreign residents become eligible to apply for naturalization after 5 years of legal residency (one of the fastest pathways in the EU). This means that expats who maintain residency through visas like the D7, D8, Golden Visa, or work permits can seek citizenship relatively quickly. The naturalization process requires passing a basic Portuguese language exam (A2 level) and showing integration into Portuguese society, as well as a clean criminal record. Once granted, Portuguese citizenship gives you the full rights of an EU citizen – including the ability to live and work anywhere in the EU – which is a significant financial and personal benefit for expats planning long-term life in Europe.

Below, we present comparative tables summarizing Financial Accessibility, Insurance Benefits, and Residency/Citizenship options across these expat-friendly hubs for quick reference.

Comparative Table: Residency & Citizenship Pathways

| Country | Notable Residency Programs | Investment (if any) | Time to Permanent Residency | Time to Citizenship | Dual Citizenship? |

|---|---|---|---|---|---|

| United Kingdom | – Skilled Worker Visa: job offer required (no direct investment). \ – Innovator Visa: start-up endorsed (no minimum investment, but needs viable business idea). \ – Ancestry Visa: for Commonwealth citizens with UK-born grandparent. | £0 direct (Skilled Worker); £50k recommended for Innovator startup. | 5 years (ILR) on work visas (sooner if a now-closed Investor visa had been used). | 6 years total (5+1 after ILR). | Yes |

| Switzerland | – Work Permit (B): via employment (quota for non-EU). \ – Independent Means/Retiree: negotiate lump-sum tax with canton (for wealthy individuals). | Varies – lump-sum taxation ~CHF 250k/yr in taxes for fast-track residency. | 5–10 years for C Permit (EU nationals 5; most others 10, can be 5 if highly integrated). | 10 years (with C Permit, plus integration criteria). | Yes |

| Singapore | – Employment Pass: need job (min salary ~$4–5k/month). \ – Global Investor Program: invest S$2.5M in business/fund for PR. \ – EntrePass: for entrepreneurs with innovative startups (no minimum investment but stringent approval). | S$2.5M (~$1.8M) for investor PR route Other work visas: no direct investment required. | Eligible for PR after typically 1–2 years on work visa (approval not guaranteed). PR is effectively permanent. | 2+ years as PR to apply, but granting is tough. | No |

| UAE (Dubai) | – Property Investor Visa: 2-year residency for AED 750k property; 10-year Golden Visa for AED 2M property \ – Work Visa: employer-sponsored (common route). \ – Green Visa: 5-year self-sponsored for freelancers/business owners (income proof required). | AED 2,000,000 ($545k) property for 10-year visa No investment needed for work visas (just a job). | No formal PR – residency is maintained by visa renewal. Golden Visas (5 or 10 year) are long-term renewable residencies. | N/A – No routine citizenship process for expats. (Exceptional cases only.) | No (with rare exceptions). |

| United States | – Employment Green Card: employer-sponsored (EB-2/EB-3 categories). \ – EB-5 Investor Green Card: invest $1.05M (or $800k in target area) + create 10 jobs\ – Family Sponsorship: immediate relatives of U.S. citizens (spouse, etc.). \ – Diversity Lottery: 55k visas annually (random draw for eligible countries). | $800k–1M for EB-5 investment other paths cost mainly fees, not investment. | NA (Direct to PR) – e.g. marriage to a U.S. citizen or EB-5 leads directly to a Green Card. Work visas H-1B/L-1 don’t themselves give PR, but allow transition to PR in ~5–10 years. | 5 years after obtaining Green Card (3 years if married to a U.S. citizen). | Yes |

| Portugal | – Golden Visa (ARI): €280k–€500k investment in property/fund (program under revision in 2025). \ – D7 “Passive Income” Visa: for retirees or remote workers with ~€8k/yr income + accommodation. \ – Digital Nomad Visa: 1-year remote work residency (income ~€2,800/mo required). \ – Job or Study Visas: standard routes for workers and students. | €280k (rehab property in low-density area) to €500k (prime property) for Golden Visa. €0 for D7 (just proof of income). | 5 years temporary residency then eligible for permanent residency (or citizenship directly). Golden Visa holders meet this by maintaining investment & minimal stay (7 days/year) | 5 years (Portugal offers naturalization after 5 years legal residency, with A2 language test). | Yes |

Note: Expats may also consider opening an offshore bank account to manage their wealth and investments more effectively while living abroad.

Essential Features in Expat-Friendly Checking Accounts

When it comes to choosing a checking account as an expat, there are several essential features to look for. These include:

Low or No Foreign Transaction Fees: Many banks charge foreign transaction fees for transactions made abroad, typically between 1-3% of each purchase. For expats, these fees can quickly add up, making low or waived foreign transaction fees essential. Look for banks that do not charge foreign transaction fees on debit card purchases or have minimal fees.

Global ATM Access and Fee Reimbursements: Cash access is essential for expats, but using foreign ATMs can bring on heavy fees. Many expat-friendly accounts offer worldwide ATM reimbursements, refunding fees incurred at ATMs outside the U.S. This feature can save you a significant amount of money in ATM fees.

Multi-Currency and International Wire Transfer Options: An expat-friendly account should support multiple currencies, allowing for easy exchange or management of funds. Some banks make international wire transfers cheaper and more accessible, which is crucial for expats who need to send money across borders frequently.

Robust Online and Mobile Banking: 24/7 digital access is crucial for expats, allowing for real-time balance checks, payments, and transaction monitoring. Look for banks with high-rated mobile apps or online banking platforms that offer comprehensive services, including bill payments, direct deposits, and account management.

Reliable Customer Support: Expats face unique banking needs, requiring helpful customer service. Choose a bank with support that understands expat-related issues, such as verifying identity from abroad. Having access to knowledgeable and responsive customer support can make a significant difference in managing your finances smoothly.

By prioritizing these features, expats can find checking accounts that cater to their specific needs, ensuring a hassle-free banking experience while living abroad.

Conclusion

Each of these expat-friendly hubs offers a unique mix of financial advantages. For example, Switzerland’s ultra-low interest rates, Singapore’s robust credit access, and the UK’s public healthcare can significantly improve an expat’s financial outlook. However, unlocking these benefits often hinges on obtaining the right residency status – whether that’s Permanent Residence in Singapore to avoid hefty property levies, a Green Card in the US to access SBA business loans, or a long-term visa in the UAE for higher LTV on mortgages. Stability and regulation matter too: countries like Switzerland, the UK, and Singapore boast very secure banking environments with strong depositor protections, whereas hubs like the UAE are high-opportunity but still formalizing safeguards (notably deposit insurance).

For globally-minded professionals and investors, dual citizenship flexibility is also key – jurisdictions that allow dual nationality (UK, Switzerland, Portugal, USA, etc.) make it easier to naturalize without sacrificing your original citizenship. In contrast, Singapore or the UAE may be best utilized as long-term residencies rather than passport switches.

If you’re searching for “best country for expat mortgage” or “where can expats get cheap loans”, the above comparisons show there is no one-size-fits-all answer. Your choice should align with your career, investment goals, and tolerance for integration. For instance, a tech entrepreneur might leverage Singapore’s startup ecosystem and eventually attain PR for financial perks, whereas a retiree with passive income might opt for Portugal’s residency to enjoy Europe’s banking and insurance stability.

In sum, these financial hubs reward those expats who commit to residency or citizenship: by doing so, you gain insider access to credit markets, better insurance rates, and the full trust of the local financial system. Use the data and tables above to weigh your options, and you’ll be well on your way to making an informed decision about your next expat destination – one that secures both your lifestyle and your financial future.