Bulgaria has emerged as a compelling destination for high-net-worth individuals (HNWIs) and expatriates seeking favorable tax conditions within the European Union. The nation’s commitment to a stable and competitive fiscal environment, underscored by its consistent application of low flat tax rates for both personal and corporate income, positions it as a jurisdiction warranting serious consideration. Coupled with its membership in the EU and strategic geographical location, Bulgaria offers a unique blend of tax efficiency and access to a reputable economic zone. This report delves into the intricacies of Bulgaria’s tax system, specifically examining its appeal to HNWIs and expatriates, encompassing personal and corporate tax obligations, residency considerations, benefits for expatriates, wealth-related taxes, strategic optimization opportunities, and recent legislative updates. It is also crucial to understand the annual tax return obligations for individuals regarding their tax status and income in Bulgaria.

Understanding Tax Residency in Bulgaria for Individuals and Entities

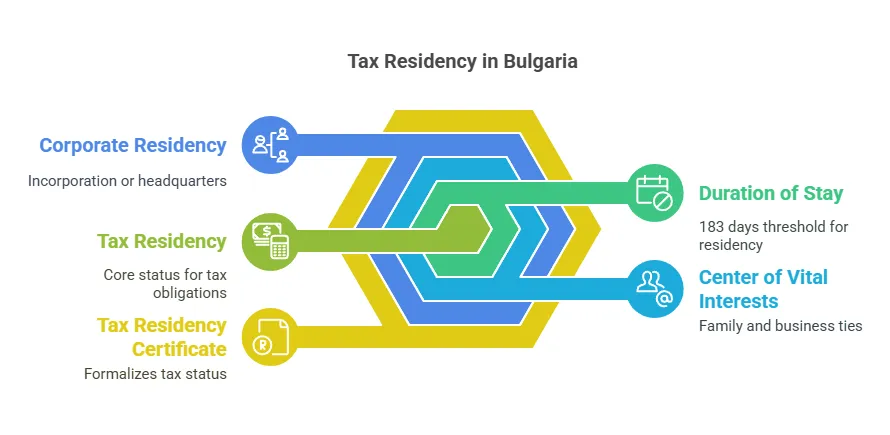

Tax residency serves as the cornerstone for determining an individual’s or a company’s tax obligations within a specific jurisdiction. In Bulgaria, the criteria for establishing tax residency are clearly defined for both individuals and entities. For individuals, several factors are considered. One primary criterion is physical presence, with an individual being deemed a tax resident if they stay in Bulgaria for more than 183 days within any 12-month period. However, physical presence alone is not always the sole determinant. Bulgaria also considers the “center of vital interests,” which encompasses an individual’s strongest economic and personal ties to the country. This includes factors such as owning property, having family in Bulgaria, the location of business operations, and the management of bank accounts. Even if the 183-day threshold is not met, an individual may still be considered Bulgarian tax residents if their permanent address is in Bulgaria and their center of vital interests is demonstrably within the country. Individuals who are considered Bulgarian tax residents are liable for tax on their worldwide income, while non-residents only pay taxes on income sourced from Bulgaria. Additionally, Bulgarian citizens sent abroad by the state are also considered tax residents.

For corporate tax residency, the criteria are more straightforward. A company is generally considered a tax resident of Bulgaria if it is incorporated under Bulgarian law or if its registered office is located in Bulgaria. It is important to distinguish between a Residency Card, which grants permission to reside in Bulgaria for specific purposes like work or study, and a Tax Residency Certificate, which formally confirms an individual’s tax obligations within the country. While a Residency Card might be a prerequisite for obtaining tax residency, it does not automatically confer that status. Tax residency in Bulgaria is determined on an annual basis and typically requires a formal application to the Bulgarian National Revenue Agency (NRA). The processing of a Tax Residency Certificate can take approximately one month from the submission of the application.

The emphasis on the “center of vital interests” provides a nuanced approach to determining tax residency, extending beyond mere physical presence. This acknowledges that an individual’s connections to a country can be multifaceted and allows for consideration of their economic and personal ties, which is particularly relevant for HNWIs with diverse international activities. Furthermore, the separation between a Residency Card and a Tax Residency Certificate underscores the need for expatriates to actively engage with the Bulgarian tax authorities to formally establish their tax residency and benefit from the advantageous tax regime.

The Attractive Bulgarian Tax System: A Deep Dive into Key Rates and Provisions

Bulgaria’s tax system is characterized by its simplicity and competitive rates, making it an appealing destination for both individuals and corporations.

Personal Income Tax: The Flat 10% Rate and its Implications

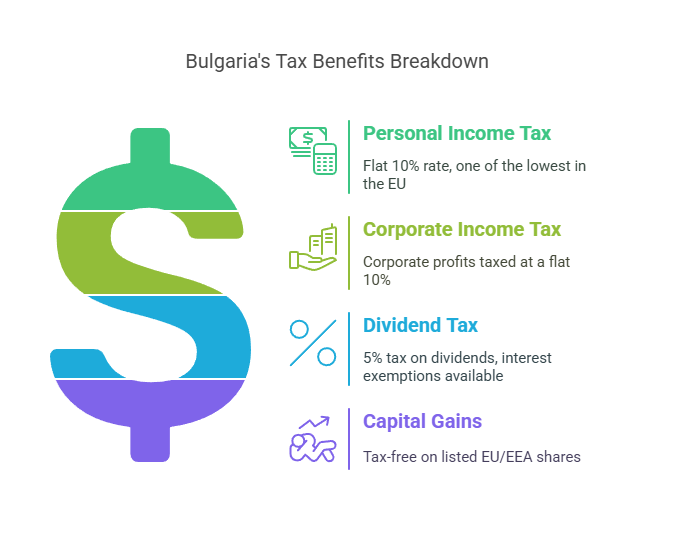

A cornerstone of Bulgaria’s attractiveness is its flat personal income tax rate of 10%. Employment income, derived from work under an employment contract, is also taxed at this flat rate of 10%. This rate is one of the lowest within the European Union, applying uniformly across various income levels. While the standard rate is 10%, there are specific exceptions and variations for certain types of income. For instance, dividends are taxed at a reduced rate of 5%, and interest income from bank accounts within the EU/EEA is generally tax-free. Interest from non-EU/EEA bank accounts is taxed at the standard 10% rate. Notably, income earned by seafarers may be subject to a rate as low as 1%. Income for sole traders might be taxed at 15% on their net income, while freelancers can benefit from an effective tax rate of 7.5% due to a provision allowing a 25% deduction for operational expenses. It is worth noting that the Bulgarian tax regime offers a limited personal allowance, primarily for disabled individuals.

The lower tax rate on dividends compared to the standard income tax rate serves as an incentive for investment income. This differential treatment can be particularly advantageous for HNWIs who often have significant income derived from investments, potentially leading to a reduced overall tax liability on their investment returns. Furthermore, the tax exemption for interest income from bank accounts within the EU/EEA can be beneficial for expatriates who maintain financial ties within the European economic zone, encouraging savings within the EU banking system.

Corporate Income Tax: Competitiveness and Recent Developments

Bulgaria’s corporate income tax rate is also set at a flat 10% , making it one of the most competitive corporate tax rates in the European Union . This low rate can significantly reduce the tax burden on company profits, encouraging reinvestment and business growth within Bulgaria. However, recent developments in international tax law have introduced a global minimum tax. As of January 1, 2024, Bulgaria has implemented a 15% global minimum tax for large multinational enterprise groups and large-scale domestic groups within the EU with annual consolidated revenue of at least EUR 750 million . This implementation includes the Income Inclusion Rule (IIR), applicable for fiscal years beginning on or after January 1, 2024, and the Undertaxed Profit Rule (UTPR), applicable for accounting periods beginning on or after January 1, 2025 . Bulgaria also intends to adopt a Qualified Domestic Top-Up Tax (QDMTT), applicable for fiscal years beginning on or after January 1, 2024 . Notably, there are potential corporate tax exemptions available for companies that incorporate in Bulgarian municipalities with high rates of unemployment , aiming to stimulate economic activity in these regions.

While Bulgaria retains its appealing 10% corporate tax rate, the introduction of the 15% global minimum tax signifies an alignment with international efforts to prevent base erosion and profit shifting . This new rule primarily targets very large multinational entities, suggesting that the standard 10% corporate tax rate will continue to be a significant advantage for smaller businesses and many HNWIs operating through their own companies in Bulgaria. The potential for corporate tax exemptions in high-unemployment areas further enhances Bulgaria’s attractiveness as a business location for those willing to invest in these regions .

Taxation of Dividends, Interest, and Capital Gains

The tax treatment of dividends, interest, and capital gains is crucial for HNWIs. In Bulgaria, dividends paid to non-resident companies and individuals are subject to a 5% withholding tax, unless a double tax treaty specifies a lower rate . Dividends paid by a Bulgarian resident company to an entity tax resident in an EU/EEA member state are exempt from withholding tax , as are dividends paid to resident companies . Dividends paid to resident individuals are subject to a 5% withholding tax . Interest paid to non-residents is generally subject to a 10% withholding tax, again potentially reduced by tax treaties , while interest paid to resident companies is exempt from withholding tax , and interest paid to resident individuals is taxed at 10% . Capital gains are generally taxed at the standard income tax rate of 10% for both individuals and corporations . A significant exemption exists for capital gains derived from the sale of shares listed on the Bulgarian and EU/EEA stock exchanges . However, capital gains from the sale of real estate may be subject to a tax rate ranging between 0.1% and 3%, determined by the specific municipality .

The withholding tax regime on dividends and interest is a key consideration for HNWIs with international income streams . The exemption from dividend withholding tax for EU/EEA resident legal entities can be particularly advantageous for those structuring their investments within the European Union. Furthermore, the exemption of capital gains from the sale of listed shares incentivizes investment in the Bulgarian and broader EU stock markets , potentially attracting HNWIs seeking to grow their capital through equity investments.

Value-Added Tax (VAT) and Other Local Taxes

Bulgaria’s Value-Added Tax (VAT) system is designed to be competitive and aligned with European Union regulations. The standard VAT rate in Bulgaria is 20%, which is applied to most goods and services. However, there are reduced rates of 9% for hotel accommodations and 0% for certain exports and intra-EU supplies.

In addition to VAT, Bulgaria has other local taxes that apply to specific situations. For example, property tax is levied on real estate owned by individuals and companies, with rates varying depending on the municipality and type of property. Vehicle tax is also applicable to owners of vehicles, with rates based on the vehicle’s engine capacity and age.

Inheritance tax is another important consideration in Bulgaria. The country has a relatively low inheritance tax rate, with a maximum rate of 10% applicable to certain types of property. However, there are exemptions and deductions available, and the tax is only levied on property situated in Bulgaria or abroad that is inherited by Bulgarian citizens.

It’s worth noting that Bulgaria has a territorial tax system, which means that foreign-sourced income is generally not taxed in Bulgaria unless it’s remitted into the country. This can be beneficial for Bulgarian tax residents who have income from foreign sources.

Overall, Bulgaria’s VAT and local tax system is designed to be competitive and attractive to businesses and individuals. However, it’s essential to understand the specific tax obligations and regulations that apply to your situation to ensure compliance and minimize tax liabilities.

Tax Rates:

Standard VAT rate: 20%

Reduced VAT rate for hotel accommodations: 9%

Zero-rated VAT for certain exports and intra-EU supplies: 0%

Inheritance tax rate: up to 10%

Property tax rates: vary depending on municipality and type of property

Vehicle tax rates: based on engine capacity and age

Tax Obligations:

VAT registration is required for businesses with an annual turnover exceeding BGN 50,000 (approximately €25,600)

Property tax is levied on real estate owned by individuals and companies

Inheritance tax is levied on property situated in Bulgaria or abroad that is inherited by Bulgarian citizens

Vehicle tax is applicable to owners of vehicles

Tax Residency:

Bulgarian tax residents are subject to taxation on their worldwide income

Foreign-sourced income is generally not taxed in Bulgaria unless it’s remitted into the country

Bulgaria has a territorial tax system

Double Taxation Treaties:

Bulgaria has signed double taxation treaties with numerous countries to prevent double taxation of income

These treaties can affect tax obligations in Bulgaria and provide relief from double taxation

Tax Benefits and Incentives for Expatriates in Bulgaria

Beyond the general advantages of a low flat tax rate , Bulgaria offers specific tax benefits and incentives that are particularly attractive to expatriates.

Special Considerations for Digital Nomads and Freelancers

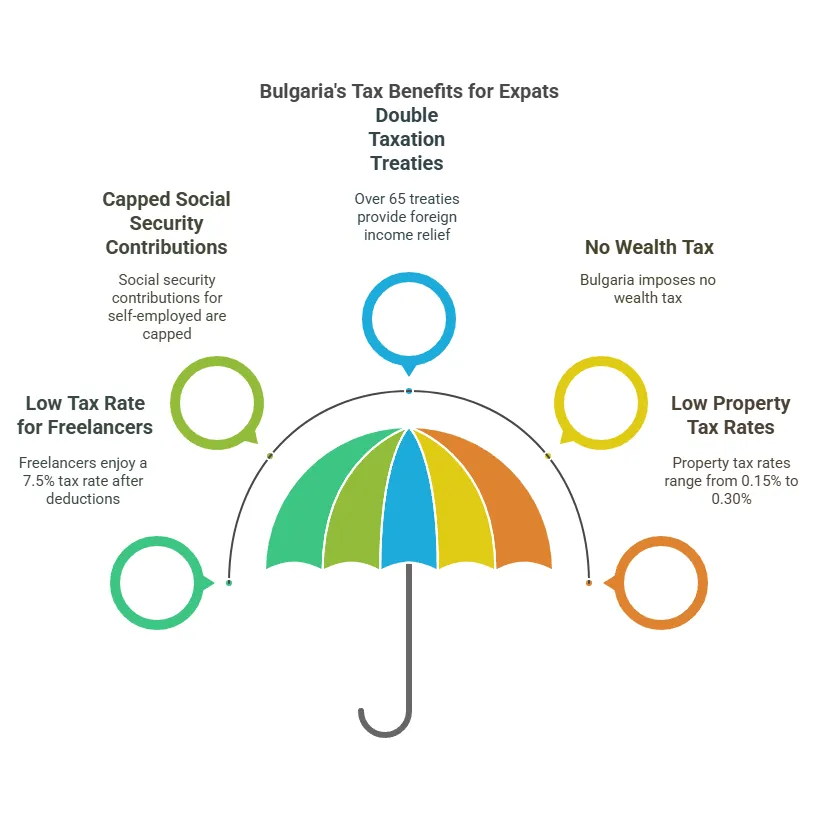

Bulgaria has gained significant popularity among digital nomads and freelancers due to its favorable tax regime. Freelancers benefit from an effective income tax rate of just 7.5% due to a provision allowing a 25% deduction for operational expenses without the need for detailed justification . Additionally, social security contributions for freelancers are capped at a certain income level, approximately EUR 1,900 per month , limiting the social security burden for higher earners. The combination of low taxes and a relatively low cost of living makes Bulgaria an appealing choice for location-independent professionals .

The specific tax treatment afforded to freelancers, with the simplified 25% expense deduction, positions Bulgaria as a highly competitive destination for digital nomads and self-employed expatriates . This significantly reduces their taxable income and simplifies tax compliance compared to many other European countries.

Taxation of Foreign Income and Double Taxation Relief

Bulgarian tax residents are subject to tax on their worldwide income, meaning they are liable to pay taxes on all income earned globally, while non-residents are taxed only on income derived from Bulgarian sources. To mitigate the issue of double taxation, Bulgaria offers tax credits for taxes paid overseas. Furthermore, Bulgaria has entered into double taxation treaties with over 65 countries, providing relief from double taxation in accordance with the terms of these agreements. Even in the absence of a tax treaty, Bulgaria grants unilateral tax relief for foreign taxes paid on income also taxable in Bulgaria.

Given that Bulgaria taxes residents on their global income, the availability of double taxation relief mechanisms is crucial. The extensive network of double taxation treaties and the provision of unilateral tax credits ensure that expatriates are not subjected to excessive taxation on income earned outside of Bulgaria, making it a more appealing and compliant destination for international residents.

Strategic Tax Planning and Optimization for High-Net-Worth Individuals

Bulgaria’s overall low tax burden presents numerous opportunities for strategic tax planning and wealth preservation for HNWIs.

Leveraging Bulgaria’s Tax Laws for Wealth Preservation

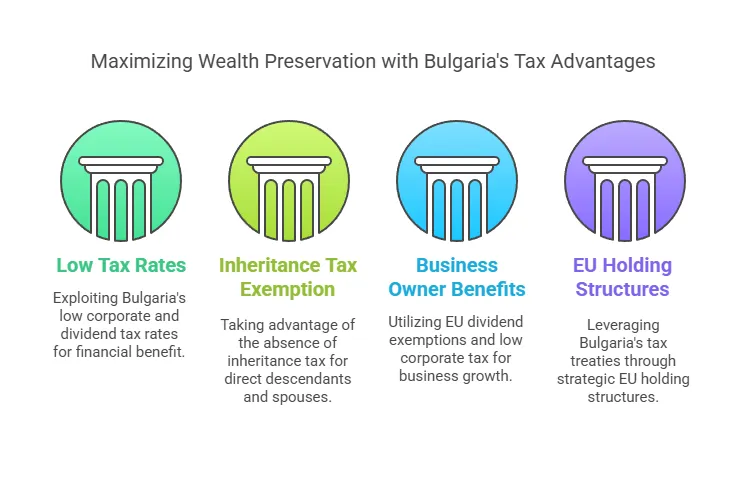

HNWIs can potentially benefit from the 7.5% effective tax rate on freelance income if their income sources align with this category. The 5% tax rate on dividend income is also advantageous for those with substantial investment portfolios. The exemption from capital gains tax on listed shares further enhances Bulgaria’s appeal for equity investors. Notably, Bulgaria does not impose a wealth tax , which is a significant benefit for preserving accumulated assets. Property tax rates are relatively low, ranging from 0.15% to 0.30% of the property’s tax value . Furthermore, there is no general inheritance tax for close family members .

The absence of a wealth tax is a significant advantage for HNWIs, as it allows for the preservation of their net worth without annual taxation based on its value . This can lead to substantial long-term savings compared to jurisdictions that levy wealth taxes. The relatively low property tax rates also make owning real estate in Bulgaria more tax-efficient , and the exemption from inheritance tax for spouses and direct descendants facilitates smoother wealth transfer planning .

Potential Use of Holding Structures

While Bulgaria does not have a specific holding company regime , its low corporate tax rate of 10% and a 5% withholding tax on dividends distributed to shareholders can still make it an attractive jurisdiction for establishing holding structures. The exemption from withholding tax on dividends paid to EU/EEA entities is particularly beneficial for those with business interests within the European Union. Bulgaria’s extensive network of double tax treaties can further enhance the attractiveness of using Bulgarian holding structures for managing international investments.

Despite the absence of a dedicated holding company regime, the combination of a low corporate tax rate and a relatively low dividend withholding tax, coupled with the EU dividend exemption, can position Bulgaria as a favorable location for holding companies, especially for those managing subsidiaries within the European Union .

Navigating Wealth, Inheritance, and Property Taxes in Bulgaria

Understanding the nuances of wealth, inheritance, and property taxes is essential for HNWIs considering Bulgaria.

Wealth Tax

As previously mentioned, Bulgaria does not impose a net wealth tax .

Inheritance Tax

Inheritance tax in Bulgaria has specific rules and exemptions. Spouses and direct descendants are exempt from inheritance tax . For siblings and their children, the tax rate ranges from 0.4% to 0.8% on the inherited portion exceeding BGN 250,000 (USD 140k) . Other heirs are subject to rates between 3.3% and 6.6% on the inherited portion exceeding a certain threshold, which appears to be either BGN 25,000 or BGN 250,000 depending on the source . The tax is levied on the value of the inherited assets .

Property Tax

Owners of real estate in Bulgaria are liable for an annual property tax based on the tax value of the property . The tax rate is determined by local authorities and ranges from 0.15% to 0.30% . Payment is typically due in installments . Additionally, there is a transfer tax on the acquisition of property, which is generally around 2% of the property price, along with registration and notary fees

Summary of Wealth, Inheritance, and Property Taxes in Bulgaria

| Tax Type | Rate/Threshold | Exemptions/Notes |

|---|---|---|

| Wealth Tax | None | |

| Inheritance Tax | 0% for spouses and direct descendants; 0.4-0.8% / 3.3-6.6% for others (over thresholds) | Thresholds apply (BGN 25,000 or 250,000 depending on relationship); rates vary based on relationship and inherited amount; tax on assets above threshold. |

| Property Tax | 0.15% – 0.30% of tax value (municipality dependent) | Paid annually, often in installments; rates vary based on location and property type. |

| Property Transfer Tax | ~2% of property price | Typically paid by the buyer; plus registration fee (0.1%) and notary fee (up to BGN 3,000). |

Key Updates in Bulgarian Tax Legislation for 2024 and 2025

Several key updates in Bulgarian tax legislation are relevant for 2024 and 2025. As mentioned earlier, the 15% global minimum tax came into effect on January 1, 2024, with the IIR applicable from that date and the UTPR from accounting periods beginning on or after January 1, 2025 . Bulgaria also intends to implement the QDMTT from January 1, 2024 . Draft legislation for a Standard Audit File for Taxes (SAF-T) is expected to be implemented in early 2025, with mandatory adoption phased in starting in 2026 . Public Country-by-Country (CbC) reporting was adopted from January 1, 2025, for multinational enterprises meeting certain revenue thresholds . The VAT registration threshold will increase to BGN 166,000 from January 1, 2025 . Adjustments have also been made to the input VAT credit for scrapped or lost goods . Additionally, the tax periods for the global minimum tax calculation have been revised based on the applicable accounting standards .

The upcoming implementation of SAF-T reporting signifies a move towards enhanced transparency and digitalization of tax administration in Bulgaria . Businesses operating in Bulgaria, including those owned by HNWIs, will need to prepare for these new reporting requirements, which will necessitate the submission of detailed accounting information to the tax authorities on a monthly basis in a standardized electronic format. The increase in the VAT registration threshold will likely benefit smaller businesses and startups by reducing their compliance burden , potentially making Bulgaria an even more attractive location for new ventures.

Illustrative Examples and Case Studies

To illustrate the practical application of Bulgaria’s tax system, consider the following examples:

Example 1: Digital Nomad. A software developer from the US resides in Bulgaria for more than 183 days and earns EUR 80,000 annually as a freelancer. Their taxable income in Bulgaria would be EUR 80,000 minus a 25% expense deduction (EUR 20,000), resulting in a taxable base of EUR 60,000. The income tax payable would be EUR 60,000 * 10% = EUR 6,000, representing an effective tax rate of 7.5%. This is notably lower than potential tax liabilities in many other developed countries.

Example 2: HNWI Investor. A German resident invests in shares of a company listed on the Bulgarian Stock Exchange and realizes a capital gain of EUR 50,000. This gain would be exempt from capital gains tax in Bulgaria. If they also receive EUR 20,000 in dividends from a Bulgarian company, the tax liability on these dividends would be EUR 20,000 * 5% = EUR 1,000.

Example 3: Business Owner. A French entrepreneur establishes a company in Bulgaria with a taxable profit of EUR 200,000. The corporate income tax payable would be EUR 200,000 * 10% = EUR 20,000. If the company then distributes EUR 50,000 in dividends to his French holding company, there would be no withholding tax in Bulgaria due to the exemption for EU resident legal entities.

These examples, while simplified, illustrate the tangible benefits of Bulgaria’s tax regime for different profiles of individuals and businesses, highlighting the potential for significant tax savings.

Conclusion: Why Bulgaria Presents a Compelling Tax Landscape for HNWIs and Expats

Bulgaria offers a compelling tax landscape for high-net-worth individuals and expatriates seeking a stable, low-tax environment within the European Union. The consistent application of low flat tax rates for both personal and corporate income, coupled with the absence of wealth tax and favorable treatment of dividends and capital gains, makes it an attractive destination for wealth preservation and business operations. The specific tax benefits for freelancers further enhance its appeal to digital nomads and self-employed professionals. While the implementation of the global minimum tax will impact very large multinational corporations, the core tax advantages for individuals and smaller businesses remain robust. The stability of Bulgaria’s tax policy, particularly the long-standing flat tax rate, provides a degree of predictability that is valuable for long-term financial planning. Bulgaria’s unique combination of tax efficiency and EU membership positions it as an increasingly attractive option for those looking to optimize their tax liabilities within a reputable international framework.